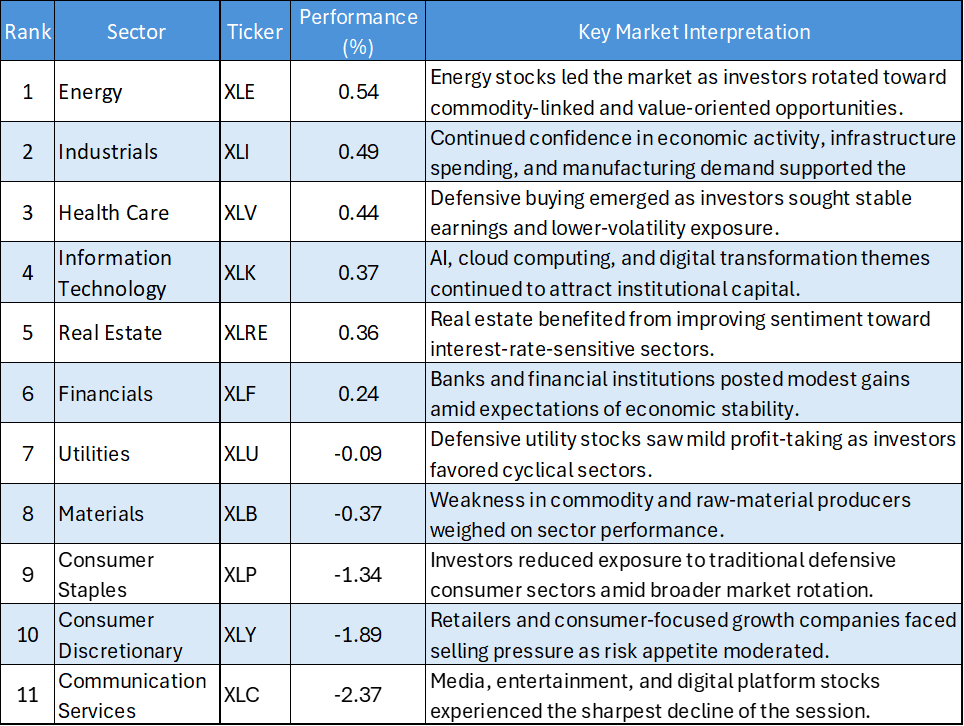

Key Highlights

- Energy Takes the Lead: Energy (XLE) advanced 0.54%, emerging as the strongest-performing sector as investors rotated toward commodity-linked and value-oriented opportunities.

- Industrials and Health Care Show Resilience: Industrials (XLI) gained 0.49% while Health Care (XLV) rose 0.44%, reflecting continued demand for economically sensitive and defensive sectors.

- Technology Maintains Positive Momentum: Information Technology (XLK) added 0.37%, extending its recent strength despite a broader pullback in growth-oriented sectors.

- Communication Services and Consumer Stocks Lag: Communication Services (XLC) fell 2.37%, while Consumer Discretionary (XLY) declined 1.89% and Consumer Staples (XLP) lost 1.34%, making them the weakest performers of the session.

The US equity market delivered a mixed session on June 22, 2026, characterized by a notable shift away from consumer-oriented growth sectors and toward Energy, Industrials, and Health Care. While several sectors remained in positive territory, market leadership broadened beyond Technology as investors adopted a more balanced and selective approach to risk exposure.

The divergence between cyclical leaders and consumer-related laggards suggests investors are reassessing growth expectations while maintaining confidence in sectors supported by economic activity, infrastructure spending, and defensive earnings profiles.

Daily US Sector Performance Summary

Key Market Themes

Energy Emerges as Market Leader

Energy (XLE) led all sectors with a gain of 0.54%, reflecting improving sentiment toward commodity-linked businesses and value-oriented opportunities. The sector's outperformance suggests investors increasingly sought exposure to areas benefiting from stable energy prices and attractive valuations. The move also highlights a degree of rotation away from the high-growth sectors that had dominated recent market leadership.

Industrials Continue to Attract Capital

Industrials (XLI) advanced 0.49%, making it one of the strongest-performing sectors of the session. Continued strength across industrial companies suggests investors remain optimistic about economic activity, infrastructure investment, and manufacturing demand. The sector's ability to generate gains alongside Energy reinforces the view that market participation is broadening beyond traditional growth-oriented industries.

Health Care Demonstrates Defensive Strength

Health Care (XLV) gained 0.44%, outperforming many sectors that have recently benefited from strong growth momentum. The advance highlights growing investor demand for companies with stable earnings profiles and defensive characteristics. Such resilience often emerges when market participants seek a balance between capital preservation and continued equity exposure.

Technology Holds Firm

Information Technology (XLK) rose 0.37%, extending its positive momentum despite a broader rotation occurring elsewhere in the market. Although Technology no longer dominated sector leadership during the session, investors continued to support long-term themes such as artificial intelligence, cloud computing, and digital transformation. The sector's ability to remain in positive territory suggests institutional confidence in its earnings outlook remains intact.

Financials and Real Estate Deliver Moderate Gains

Financials (XLF) and Real Estate (XLRE) posted gains of 0.24% and 0.36%, respectively. While their advances were relatively modest compared with the session's leaders, both sectors contributed positively to overall market breadth. Their performance suggests investors remain comfortable maintaining exposure to sectors linked to economic stability, credit conditions, and interest-rate expectations.

Consumer and Communication Sectors Under Pressure

Communication Services (XLC) suffered the steepest decline of the session, falling 2.37%, while Consumer Discretionary (XLY) and Consumer Staples (XLP) dropped 1.89% and 1.34%, respectively. The broad weakness across consumer-related sectors suggests investors reduced exposure to areas heavily dependent on household spending and growth expectations. This selling pressure stood in stark contrast to the strength observed in Energy, Industrials, and Health Care.

Market Rotation Becomes More Evident

The June 22 session highlighted a clear rotation away from consumer and communication stocks toward sectors offering either defensive qualities or exposure to underlying economic fundamentals. Unlike previous growth-led rallies, leadership was more balanced and diversified across multiple industries. Such shifts often occur when investors seek greater portfolio stability while remaining constructive on the broader market outlook, indicating a more measured approach to risk-taking.

Bottom Line

The June 22 session reflected a meaningful shift in sector leadership. Energy (XLE) led the market with a gain of 0.54%, while Industrials (XLI), Health Care (XLV), Technology (XLK), and Real Estate (XLRE) also posted positive returns.

In contrast, Communication Services (XLC), Consumer Discretionary (XLY), and Consumer Staples (XLP) experienced significant weakness, highlighting investor preference for sectors tied to economic resilience and defensive earnings.

Going forward, market participants will closely monitor whether this rotation continues or whether growth-oriented sectors can regain leadership. For now, the sector landscape suggests a more balanced market environment with investors increasingly favoring diversification over concentrated growth exposure.

Please wait processing your request...

Please wait processing your request...