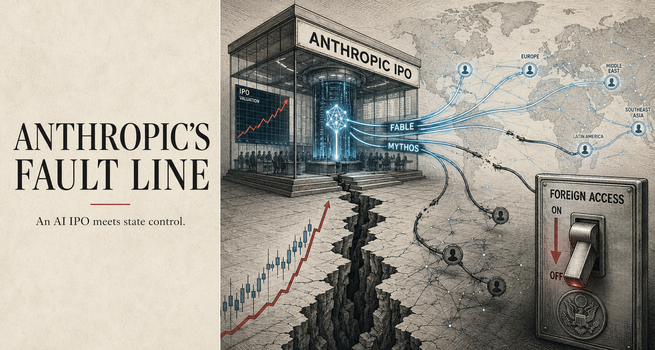

As Anthropic moves toward a 2026 IPO, a US government access restriction on its frontier models exposes structural risks that public market investors cannot afford to ignore.

Key Highlights

- Anthropic's IPO is expected as early as October 2026, entering public markets alongside OpenAI and SpaceX.

- 80% of Anthropic's consumer usage base is international, making foreign access restrictions a direct revenue risk.

- The US government's June 12th order blocking foreign access to Fable and Mythos establishes a precedent of state intervention in product distribution.

- Anthropic's March designation as a "supply-chain risk" suggests a pattern of regulatory exposure, not a one-off event.

- Public market investors will demand a valuation framework that accounts for geopolitical binary risk sitting directly on the revenue line.

The Timing Problem

Anthropic is heading toward one of the most anticipated technology IPOs of the decade at precisely the moment its relationship with the US government has become its most consequential and least predictable variable. The company that built Claude Fable 5 and the restricted Mythos 5 is not simply a frontier AI firm seeking public capital. It is now visibly a policy instrument of the American state, and that distinction will matter enormously when institutional investors begin stress-testing its S-1.

The expected October 2026 timeline places Anthropic in a three-way IPO race alongside OpenAI and SpaceX. Each carries its own complexity. But Anthropic's situation is structurally distinct. Its core product, the most capable AI model available to the public, was subject to a government-imposed foreign access restriction three days after its broadest commercial launch. That sequence is not incidental. It is the central fact any prospective investor must price.

The Revenue Geography Problem

Anthropic has disclosed that approximately 80% of its consumer usage originates outside the United States. That figure, intended to demonstrate global product-market fit, now reads differently. It quantifies the portion of the company's revenue base that the US government demonstrated it can switch off with a single executive order.

For a private company operating in a high-growth phase, international reach is an asset. For a company filing for public markets, international reach concentrated in a product category that the government has already restricted once is a liability that requires explicit disclosure and a credible mitigation framework. Neither currently exists in the public domain.

Institutional investors modelling discounted cash flows will apply a probability-weighted haircut to international revenue projections. The size of that haircut depends on how they assess the likelihood of future interventions. Given that June 12th was itself preceded by the March designation of Anthropic as a supply-chain risk, the probability is not negligible.

A Pattern, Not an Incident

The March supply-chain risk designation and the June access restriction are not independent events. They form a pattern of escalating government willingness to treat Anthropic as a regulated utility rather than a private technology company. That pattern has direct implications for how public markets will assign a governance premium or discount to the stock.

Private market valuations are negotiated between sophisticated parties who can structure protections, information rights, and exit mechanisms into their agreements. Public market valuations are set by the aggregate judgment of investors who hold no such protections. When the underlying company cannot guarantee the continuity of its own product distribution, that asymmetry of information and control becomes a valuation problem.

The government's relationship with Anthropic through Project Glasswing further complicates the picture. Glasswing embeds Anthropic's most capable models, specifically Mythos 5, into a national security adjacent framework involving vetted organisations across critical infrastructure sectors. That relationship generates revenue and confers a degree of institutional legitimacy. It also means Anthropic's most advanced product line operates under a governance structure that is not fully visible to public shareholders.

The Double-Edged Moat

There is a bullish reading of Anthropic's government proximity. A company whose technology is sufficiently critical to national security that the state intervenes to control its distribution is a company with a genuine moat. The Glasswing relationship, the vetted access structure for Mythos 5, and the evident White House awareness of Anthropic's capability trajectory all suggest a company that is deeply embedded in the infrastructure of American power.

But moats built on government proximity are contingent moats. They persist as long as the relationship remains mutually beneficial and politically stable. The same administration that restricted foreign access to Fable and Mythos on June 12th designated Anthropic a supply-chain risk in March. The strategic value of the relationship is real. Its stability as a foundation for a public company's long-term revenue model is an open question.

What the Market Will Demand

Public markets will not reject Anthropic's IPO on the basis of geopolitical risk alone. The company's technical lead, its revenue trajectory, and the structural tailwinds behind enterprise AI adoption are genuine. But investors will demand a valuation that reflects the full risk structure, including the probability that a government intervention recurs, the revenue exposure that such an intervention would affect, and the absence of any contractual or legal mechanism Anthropic can deploy to prevent it.

That is not a reason to avoid the IPO. It is a reason to price it carefully.

Please wait processing your request...

Please wait processing your request...