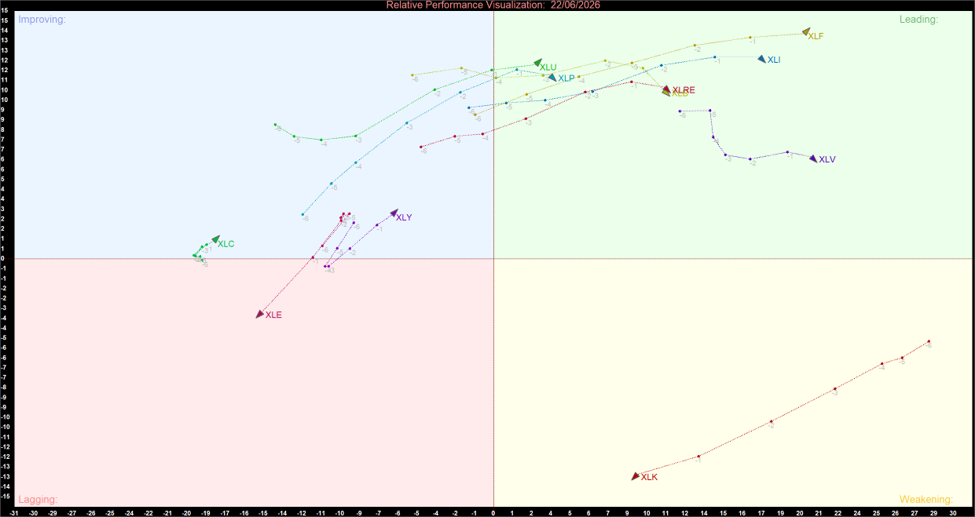

Key Highlights

- Financials Strengthen Leadership: Financials (XLF) occupy the strongest position within the Leading quadrant and continue to demonstrate both superior relative strength and improving momentum.

- Industrials Maintain Positive Rotation: Industrials (XLI) remain firmly positioned in the Leading quadrant, reinforcing confidence in economically sensitive sectors.

- Technology Remains in Weakening: Information Technology (XLK) remains the sole sector within the Weakening quadrant, indicating strong relative strength but deteriorating momentum.

- Consumer Sectors Continue Improving: Consumer Discretionary (XLY) and Communication Services (XLC) remain in the Improving quadrant, suggesting that relative momentum continues to recover.

- Energy Remains the Sole Laggard: Energy (XLE) continues to occupy the Lagging quadrant, highlighting persistent relative weakness despite signs of stabilization.

The US sector rotation profile remained constructive on June 22, 2026, although notable leadership changes continue to emerge beneath the surface. The latest Relative Rotation Graph (RRG) shows Financials and Industrials strengthening their leadership positions, while Technology continues to lose momentum after an extended period of market dominance.

At the same time, several defensive sectors remain comfortably positioned within the Leading quadrant, indicating that institutional investors continue to maintain balanced exposure across both cyclical and defensive areas of the market. The overall structure suggests broad participation remains intact despite ongoing sector rotation.

US Sector Momentum Summary

US Sector Relative Momentum Chart (at the closing price of 22/06/2026). Powered by: amibroker.com

Key Market Theme

Financials Emerge as the Dominant Market Leader

The most significant development on the chart is the continued strength of Financials (XLF). The sector occupies one of the strongest positions within the Leading quadrant and continues to move northeast, indicating simultaneous improvement in both relative strength and momentum. This sustained leadership suggests investors remain optimistic regarding economic activity, lending conditions, and earnings prospects for financial institutions.

Industrials Continue Supporting the Broader Advance

Industrials (XLI) remain firmly established within the Leading quadrant and continue to display healthy momentum characteristics. The sector's strong position reflects continued confidence in infrastructure spending, manufacturing activity, and broader economic growth. As one of the market's key cyclical sectors, Industrials continue to provide important support for the broader equity advance.

Defensive Sectors Maintain Leadership

Utilities (XLU), Consumer Staples (XLP), Real Estate (XLRE), Materials (XLB), and Health Care (XLV) all remain within the Leading quadrant. The presence of both defensive and cyclical sectors among market leaders reflects a balanced and healthy market environment. Investors appear comfortable maintaining exposure to sectors offering stable earnings and defensive characteristics while still participating in economic growth opportunities.

Technology Continues to Lose Momentum

Information Technology (XLK) remains the only sector positioned within the Weakening quadrant. Although relative strength remains exceptionally strong compared with many other sectors, momentum has deteriorated considerably over recent periods. This suggests investors are gradually diversifying away from Technology and allocating capital toward sectors exhibiting stronger relative momentum. While Technology remains an important contributor to overall market performance, its leadership role has become less dominant.

Consumer Discretionary and Communication Services Continue Improving

Consumer Discretionary (XLY) and Communication Services (XLC) remain within the Improving quadrant and continue to exhibit strengthening momentum profiles. Although both sectors still trail the broader market in terms of relative strength, their current trajectories suggest improving investor sentiment. Continued momentum gains could eventually support a transition into the Leading quadrant if current trends persist.

Energy Remains the Weakest Area of the Market

Energy (XLE) remains the sole occupant of the Lagging quadrant. While the sector has shown some stabilization compared with previous periods, both relative strength and momentum remain below broader market levels. Until a more decisive improvement in relative performance emerges, Energy is likely to continue lagging the market's leading sectors.

Bottom Line

The June 22 RRG continues to present a constructive market environment characterized by broad sector participation and diversified leadership. Financials and Industrials remain among the strongest sectors, while Utilities, Consumer Staples, Real Estate, Materials, and Health Care continue to support market breadth from within the Leading quadrant.

Meanwhile, Consumer Discretionary and Communication Services continue to improve their momentum profiles and may be positioning for future leadership roles. Technology remains a weakening leader, while Energy continues to be the market's sole laggard.

Overall, the current sector rotation profile suggests that market leadership remains broad-based and healthy, with investors maintaining exposure across both cyclical and defensive sectors rather than concentrating capital within a narrow group of industries.

Please wait processing your request...

Please wait processing your request...