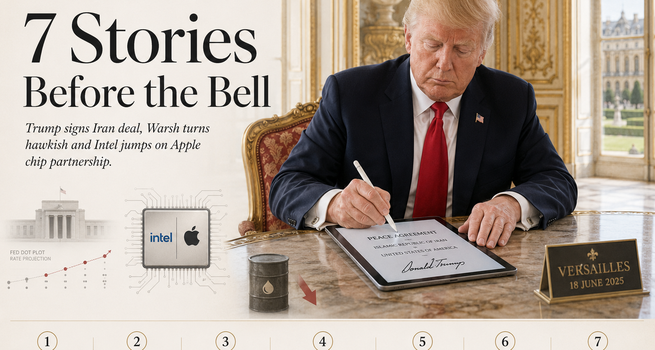

1. IRAN/GEOPOLITICS: MOU Signed at Versailles: Hormuz Reopens Toll-Free, $300B Reconstruction Fund, 60-Day Nuclear Clock Starts

Trump and Iranian President Masoud Pezeshkian digitally signed the memorandum of understanding during a dinner with G7 leaders at the Palace of Versailles on Wednesday night. Pakistan's Prime Minister Shehbaz Sharif confirmed Iran also signed. The agreement calls for the immediate reopening of the Strait of Hormuz with toll-free transit for 60 days while parties negotiate a final deal, the creation of a $300 billion fund for Iran's reconstruction and economic development, a ban on Iran producing nuclear weapons, and the immediate waiver of heavy U.S. sanctions on Iranian oil exports. The deal also ends fighting in Lebanon. Trump warned he would "bomb the hell" out of Iran if it violated the agreement, and separately said he would resume military operations if the final deal terms are unsatisfactory. WTI crude fell to a three-month intraday low of $73.36 overnight before steadying at $75.53 pre-market, on track for a weekly decline exceeding 10%. Brent trades at $78.67, down 1.11%.

- The immediate sanctions waiver on Iranian oil exports is the most consequential near-term supply variable; it restores a significant volume of barrels to global markets before Hormuz physically reopens.

- Airline and cruise operator stocks are pre-market beneficiaries: United Airlines (NASDAQ: UAL), Delta Air Lines (NYSE: DAL) and American Airlines (NASDAQ: AAL) each rose about 2%; Carnival (NYSE: CCL) advanced 3% while Royal Caribbean (NYSE: RCL) and Norwegian Cruise Line (NASDAQ: NCLH) added roughly 2%.

- Risk note: the agreement reserves the hardest issues, including Iran's enriched uranium stockpile, for the 60-day negotiation window; if those talks break down before the August deadline, oil markets reprice rapidly and the military option returns.

2. FED/MACRO: Warsh's Hawkish Debut: No Dot, No Forward Guidance, Nine Officials Back a Hike; S&P Closes -1.21%

The Federal Reserve held the federal funds rate at 3.50%-3.75% on Wednesday in a unanimous vote, marking Warsh's first policy meeting as chair and the fourth consecutive hold. The substantive shift was in everything around the decision. Warsh scrapped forward guidance entirely, noting it is "not well suited to this juncture," and cut the FOMC statement to roughly half the length of Powell-era releases. He did not submit his own dot-plot forecast. Of the 18 participants who did submit projections, nine see at least one rate hike before year-end and one sees a cut; the median 2026 rate path rose from 3.4% in March to 3.8%.

The Fed dropped its easing bias and described inflation as "elevated" relative to the 2% target, citing the global energy shock. Warsh also announced five internal reform task forces on communications, balance sheet, data sources, productivity and inflation frameworks, with most concluding by year-end. The S&P 500 closed -1.21% at 7,420.10 and the Nasdaq fell -1.34% on Wednesday. The 2-year Treasury yield rose; pre-market it sits at 4.19%-4.20%.

- CME FedWatch now prices an 85% probability of a 25-basis-point hike by December, a sharp recalibration from a week ago when four consecutive holds were the base case.

- Warsh's refusal to submit a dot removes the single most-watched anchor for rate expectations, forcing markets to read incoming data directly rather than through the Fed's own signalling, which structurally increases volatility around every data print.

- Risk note: if May jobless claims due this morning (8:30 AM ET) come in materially below consensus, the hike probability rises further and the bond market extension of Wednesday's selloff resumes, compounding pressure on rate-sensitive equities.

3. SEMICONDUCTORS: Trump Confirms Apple-Intel Chip Deal: INTC +9%, Marvell +7%, Lam +5%; Broad Chip Rally

Trump posted on Truth Social early Thursday confirming that Apple (NASDAQ: AAPL) has "agreed to work with Intel to design and build its Chips in America," completing what the president called a domestic semiconductor alliance alongside Nvidia (NASDAQ: NVDA) and Tesla (NASDAQ: TSLA), both previously confirmed Intel manufacturing partners. Intel (NASDAQ: INTC) surged approximately 9% pre-market. The government acquired a 9.9% passive stake in Intel last year at $20.47 per share through an $8.9 billion CHIPS Act investment; at Intel's current price near $120, that stake is worth approximately $52 billion, a roughly 5.8x return. Intel's 18A-P semiconductor node entered risk production earlier this week, a significant milestone in its foundry recovery.

The announcement triggered a broad chip rally: Marvell Technology (NASDAQ: MRVL) rose nearly 7%, Lam Research (NASDAQ: LRCX) and Applied Materials (NASDAQ: AMAT) both gained about 5%, Western Digital (NASDAQ: WDC) rose 5.6%, and Micron Technology (NASDAQ: MU) and Sandisk each climbed about 4%. Apple separately warned that it will raise prices on several products due to the surging cost of memory chips, which Tim Cook described as a "100-year flood" in input costs.

- Apple currently relies almost entirely on Taiwan Semiconductor Manufacturing (NYSE: TSM) for chip production; a shift to Intel for even a portion of its silicon would represent the most consequential customer win in Intel's foundry history and the first crack in TSMC's grip on leading-edge Apple silicon.

- The memory price warning from Apple is analytically distinct from the chip partnership story: it signals that the AI infrastructure buildout has created genuine component scarcity that is now passing through to consumer hardware pricing.

- Risk note: Trump's post did not disclose terms, timeline, or which Apple products would use Intel-made chips; if Apple or Intel formally clarify the arrangement as exploratory rather than contractual, the pre-market gains reverse sharply.

4. EARNINGS: Accenture -13% on Revenue Miss and FY26 Guidance Cut vs. Smith & Wesson +14% on Handgun Beat

Accenture (NYSE: ACN) fell 13% pre-market after reporting fiscal Q3 revenue of $18.72 billion, narrowly missing the $18.75 billion estimate, while cutting full-year local currency revenue growth guidance to 3%-4% from the prior 3%-5%. EPS of $3.80 beat the $3.71 estimate, but the guidance cut overshadowed the earnings beat. New bookings fell 2% to $19.3 billion, and Accenture cited its U.S. federal business as a 1% headwind to growth. The stock was already down approximately 42% year-to-date heading into results. Accenture also announced $4.18 billion in cybersecurity acquisitions, buying majority stakes in Dragos, runZero, and NetRise, a move markets read as defensive in a soft demand environment.

Smith & Wesson Brands (NASDAQ: SWBI) delivered the session's sharpest earnings beat: Q4 EPS of $0.36 versus the $0.23 estimate, revenue of $178.39 million versus $155.27 million expected. Handgun sales to sporting goods retailers jumped 23% year over year, with handguns representing 80% of units shipped. Shares rose 14-17% pre-market.

- Accenture's guidance cut is a direct signal on enterprise IT and consulting demand: the U.S. federal headwind reflects the government spending pullback, while the broader miss suggests corporate clients are deferring large-scale transformation programs.

- Smith & Wesson's channel jump illustrates the persistence of consumer discretionary demand in specific categories despite macro pressure, with the sporting goods retail channel absorbing a meaningful volume increase.

- Risk note: if Accenture's bookings trajectory continues declining into Q4, the read-across for other large IT services names broadens the de-rating across the sector.

5. COMMODITIES: Gold -2.74%, Silver -5.44%: Iran Deal and Hawkish Fed Deliver a Simultaneous Double Squeeze

Gold trades at $4,261.50 pre-market, down $119.90 or 2.74% on the session. Silver sits at $66.915, down 5.44%. The two forces are distinct and simultaneously pressing in the same direction: the Iran MOU removes the geopolitical risk premium that has supported precious metals since the war began in February, while Warsh's hawkish debut raises real yield expectations and strengthens the dollar, both structural headwinds to non-yielding assets. Copper fell 1.9%; oil is falling on supply expectations while gold is falling on rate and risk-premium dynamics, a decoupling that marks a regime shift in commodity markets.

- The simultaneous removal of the geopolitical premium and the addition of a rate-hike premium represents the sharpest two-day headwind gold has faced since the war began; the prior gold floor was partially underwritten by the assumption that Warsh would be dovish and that the Iran conflict would persist.

- Silver's larger percentage decline reflects its dual industrial-precious character: the same Iran deal that pressures the geopolitical premium also softens the industrial demand outlook for energy-adjacent metals in the near term.

- Risk note: if the 60-day nuclear talks break down and the ceasefire collapses, the geopolitical premium reasserts quickly; gold's downside from here is bounded by that optionality.

6. MOVERS: SpaceX -1.2% Extends Pullback; Pfizer -1% on CFO Exit; Robinhood +2.1% Extends Wednesday's 8.8% Surge; Meta Rebounds

SpaceX (NASDAQ: SPCX) shed 1.2% pre-market following a 5% loss on Wednesday, continuing to unwind a portion of the more than 40% gain it posted in the week following its historic IPO debut. The stock remains well above its IPO price. Pfizer (NYSE: PFE) fell 1% after announcing that CFO Dave Denton will step down on August 15; senior vice president of finance Cecile Guegan was named interim finance chief. Robinhood Markets (NASDAQ: HOOD) gained 2.1% pre-market, extending the prior session's 8.8% jump on no specific new catalyst, suggesting momentum continuation from Wednesday's move. Meta Platforms (NASDAQ: META) rebounded 1.6% pre-market after falling 5.4% on Wednesday following the Fed decision.

- SpaceX's two-session pullback is technically orderly given the scale of the prior week's move; the stock is consolidating rather than reversing, and the broader space sector remains supported by the oil-fall tailwind reducing launch cost assumptions.

- Pfizer's CFO transition at a time of ongoing pipeline uncertainty and GLP-1 competitive pressure adds a leadership risk layer to an already complex investment narrative.

- Risk note: if Robinhood's Wednesday move was driven by options flow or short covering rather than fundamental news, the pre-market extension may not hold through the regular session.

7. PRE-MARKET SETUP: Futures Rebound From Fed Selloff: Dow +0.16%, S&P +0.56%, Nasdaq +1.25%; Jobless Claims at 8:30 AM; Last Session Before Juneteenth

U.S. equity futures are recovering after Wednesday's broad selloff driven by Warsh's hawkish debut. Pre-market at 7:40 AM EDT: Dow futures at 52,029 (+85, +0.16%), S&P futures at 7,535 (+42.25, +0.56%), Nasdaq futures at 30,373.75 (+375, +1.25%). The recovery is tech-led, driven primarily by the Intel-Apple chip partnership announcement. Oil at $75.45 pre-market, continuing its decline. The 10-year Treasury yield eases slightly to 4.45-4.49% from Wednesday's close.

The weekly jobless claims report prints at 8:30 AM ET alongside the Philadelphia Fed manufacturing index for June. May Leading Economic Indicators follow at 10 AM. The Baker Hughes weekly oil and gas rig count posts at 1 PM. Today is the final session of the week; U.S. markets close Friday for the Juneteenth National Independence Day holiday.

- The Nasdaq futures outperformance relative to the Dow and S&P reflects the chip-heavy composition of the index; the Intel-Apple announcement is lifting the index disproportionately relative to the broad macro backdrop.

- A jobless claims print above 240,000 would offer the Fed cover to hold at the July meeting and temper December hike pricing; a sub-210,000 print would accelerate the hawkish re-rating that began Wednesday.

- Risk note: with no session Friday, any negative surprise in today's data or any sign of Iran deal deterioration will carry into the following Monday with no intraday opportunity to adjust.

Please wait processing your request...

Please wait processing your request...