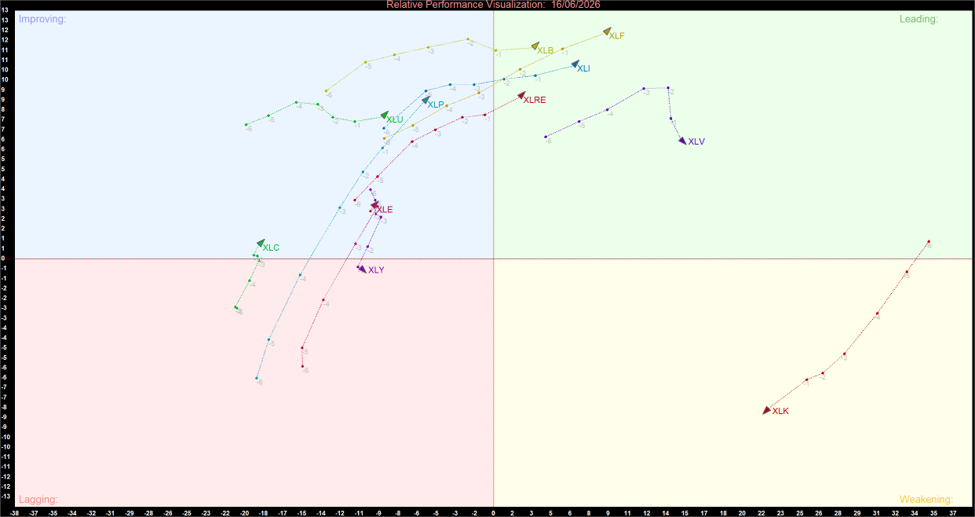

Key Momentum Highlights

- Financials Extend Market Leadership: Financials (XLF) remain firmly positioned in the Leading quadrant and continue to display strengthening relative strength and momentum, reinforcing their status as a primary leadership group.

- Broadening Leadership Across Cyclical Sectors: Industrials (XLI), Materials (XLB), and Real Estate (XLRE) remain in the Leading quadrant, highlighting expanding institutional participation beyond traditional growth sectors.

- Defensive Sectors Continue Improving: Utilities (XLU), Consumer Staples (XLP), and Communication Services (XLC) remain in the Improving quadrant, reflecting continued positive momentum development.

- Technology Remains Under Pressure: Information Technology (XLK) remains isolated in the Weakening quadrant despite maintaining superior relative strength, indicating that leadership is broadening away from the sector.

The US equity market continues to exhibit a constructive rotational structure as leadership expands across multiple sectors. The latest Relative Rotation Graph (RRG) for June 16, 2026, shows Financials, Industrials, Materials, Real Estate, and Health Care occupying the Leading quadrant, while several additional sectors continue to improve.

Unlike previous periods when market performance was heavily dependent on Technology, the current rotation profile reflects broader participation across both cyclical and defensive sectors. This diversification of leadership generally supports a healthier and more sustainable market environment.

Sector Momentum and Trajectory Summary

US Sector Relative Momentum Chart (at the closing price of 17/06/2026). Powered by: amibroker.com

Quantitative Momentum Themes

The Leading Quadrant (Expanding Leadership Base)

- Financials (XLF): Financials remain one of the strongest sectors on the chart, exhibiting positive relative strength and momentum simultaneously. The sector continues to advance deeper into the Leading quadrant, suggesting sustained institutional sponsorship and growing confidence in the sector's outlook.

- Industrials (XLI): Industrials continue to display a constructive trajectory within the Leading quadrant. The sector's strong relative performance indicates ongoing investor confidence in economic growth, manufacturing activity, and infrastructure-related themes.

- Materials (XLB): Materials remain firmly positioned in Leading after recently completing their transition from Improving. The sector continues to exhibit favorable momentum characteristics and remains an important contributor to the market's broadening leadership profile.

- Real Estate (XLRE): Real Estate continues to strengthen following its recent entry into the Leading quadrant. The sector's improving relative strength suggests growing investor demand for yield-sensitive assets and diversified exposure beyond traditional growth sectors.

- Health Care (XLV): Health Care remains one of the market's most consistent leadership groups. Although momentum has moderated compared with earlier periods, the sector continues to demonstrate strong relative strength and defensive appeal.

The Improving Quadrant (Emerging Opportunities)

- Utilities (XLU): Utilities remain firmly positioned in the Improving quadrant with positive momentum characteristics. The sector continues to progress toward leadership territory, reflecting ongoing demand for defensive income-generating assets.

- Consumer Staples (XLP): Consumer Staples continue to improve on a relative momentum basis. The sector's constructive trajectory suggests investors remain interested in stable earnings and lower-volatility opportunities.

- Communication Services (XLC): Communication Services remain near the benchmark axis but continue to build momentum. The sector's improving trajectory indicates a gradual recovery in relative performance compared with the broader market.

- Energy (XLE): Despite recent weakness in absolute performance, Energy remains in the Improving quadrant. The sector's positive momentum profile suggests underlying relative conditions are stabilizing and may support a longer-term recovery.

The Weakening Quadrant (Leadership Transition)

- Information Technology (XLK): Technology remains the most notable sector within the Weakening quadrant. While the sector continues to possess exceptionally strong relative strength, momentum has deteriorated steadily in recent periods.

- This development does not necessarily imply a bearish outlook. Instead, it reflects a market environment in which leadership is becoming more diversified as capital flows into Financials, Industrials, Materials, and Real Estate.

The Lagging Quadrant (Relative Underperformers)

- Consumer Discretionary (XLY): Consumer Discretionary remains the only sector positioned in the Lagging quadrant. Relative strength and momentum remain below benchmark levels, indicating that institutional conviction toward consumer-focused equities continues to lag other sectors.

- Although short-term rallies may occur, the sector requires further improvement before it can challenge for a position within the Improving quadrant.

Strategic Summary

The June 16 RRG structure continues to support a constructive outlook for US equities. Financials (XLF), Industrials (XLI), Materials (XLB), Real Estate (XLRE), and Health Care (XLV) remain firmly established as leadership sectors, while Utilities (XLU), Consumer Staples (XLP), Communication Services (XLC), and Energy (XLE) continue to strengthen.

Meanwhile, Technology (XLK) remains in the Weakening quadrant and Consumer Discretionary (XLY) continues to lag. Overall, the rotation profile points to expanding market breadth and a healthier leadership structure, with multiple sectors contributing to relative strength rather than relying solely on Technology-driven performance.

Please wait processing your request...

Please wait processing your request...