2026 IRA contribution limits explained: Compare IRA, Roth IRA, 401(k), Solo 401(k), SEP IRA, and SIMPLE IRA limits, catch-up contributions, and Retirement Planning opportunities.

Key Highlights

- The 2026 IRA contribution limit rises to $7,500, with additional catch-up contributions for eligible savers.

- Workplace retirement plans continue to offer substantially higher annual contribution capacity.

- Self-employed Americans can access some of the largest tax-advantaged retirement savings opportunities.

Understanding 2026 Retirement Contribution Limits

Retirement contribution limits determine how much Americans can save annually in tax-advantaged accounts. These limits are adjusted periodically by the Internal Revenue Service to reflect Inflation and changes in retirement policy.

For workers, Business owners, and self-employed professionals, understanding contribution limits is essential for maximizing retirement savings and long-term Wealth accumulation.

IRA and Roth IRA Contribution Limits

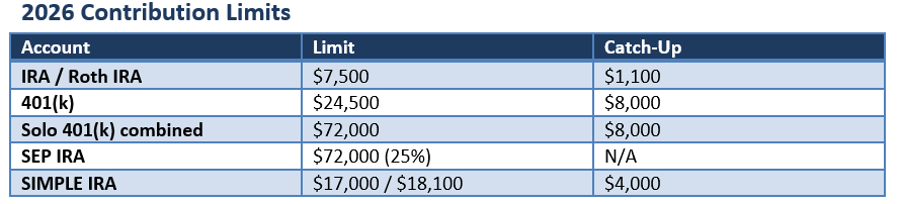

For 2026, individuals can contribute up to $7,500 to a Traditional IRA or Roth IRA combined.

Those aged 50 and older are eligible for an additional $1,100 catch-up contribution, bringing their total annual contribution limit to $8,600.

Roth IRA eligibility remains subject to income-based phaseouts. Investors whose income exceeds IRS thresholds may need to consider alternative retirement savings strategies.

401(k) and Workplace Retirement Plans

Employer-sponsored retirement plans continue to provide significantly higher savings capacity.

For 2026, employees can defer up to $24,500 into eligible workplace plans such as 401(k), 403(b), and governmental 457(b) plans.

Workers aged 50 and older can generally contribute an additional $8,000 catch-up amount. Certain participants aged 60 to 63 may qualify for enhanced catch-up contributions under SECURE 2.0 provisions if their employer's plan permits them.

Higher contribution ceilings make workplace plans a powerful tool for accelerating retirement savings.

Solo 401(k) Limits for Self-Employed Workers

Self-employed individuals and owner-only businesses often benefit from the flexibility of a Solo 401(k).

In 2026, participants may combine employee salary deferrals with employer profit-sharing contributions, allowing total annual contributions of up to $72,000, excluding eligible catch-up contributions.

For entrepreneurs seeking to maximize retirement savings, Solo 401(k) plans remain among the most generous tax-advantaged Options available.

SEP IRA Contribution Limits

A SEP IRA continues to be a popular retirement vehicle for small businesses and self-employed professionals.

For 2026, employer contributions can reach up to 25% of eligible compensation, subject to a maximum contribution limit of $72,000.

Because SEP IRAs rely solely on employer contributions, they can provide substantial retirement funding opportunities for business owners with higher Earnings.

SIMPLE IRA Limits

SIMPLE IRAs are commonly used by smaller employers seeking a streamlined retirement plan.

The 2026 employee contribution limit is $17,000, with certain small employers permitted to offer enhanced contribution limits of $18,100 under updated retirement plan provisions.

Eligible workers aged 50 and older may also make catch-up contributions, further increasing annual savings potential.

Conclusion

Retirement contribution limits represent one of the most important planning tools available to American savers. While IRAs provide accessibility and flexibility, workplace retirement plans and self-employed options offer substantially greater savings capacity. Investors who understand annual IRS limits can potentially improve tax efficiency, increase retirement account balances, and strengthen long-term financial security. Because contribution rules, catch-up provisions, and income thresholds can change over time, reviewing IRS guidance annually remains a prudent step for retirement planning.

Please wait processing your request...

Please wait processing your request...