Self-directed IRAs offer access to real estate, Private Equity, and alternative Assets, but investors must navigate Fraud risks, prohibited transaction rules, and higher fees.

Key Highlights

- Self-directed IRAs provide access to alternative assets that are typically unavailable in standard brokerage IRAs.

- Prohibited transactions can disqualify an entire IRA and create significant tax consequences.

- Higher fees, Liquidity constraints, and fraud risks make self-directed IRAs unsuitable for some retirement investors.

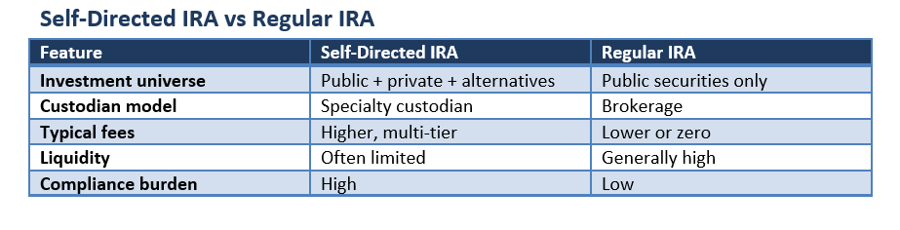

Self-directed IRAs (SDIRAs) have gained popularity among investors seeking greater control over their retirement assets. Unlike traditional brokerage IRAs, these accounts can hold a broader range of investments, including real estate, private businesses, private lending arrangements, and certain precious metals.

The appeal is clear: investors can apply their expertise beyond public markets while retaining the tax advantages associated with retirement accounts. Yet greater control also brings greater responsibility. Compliance requirements, fraud risks, and administrative complexity can make self-directed IRAs significantly more challenging than conventional retirement accounts.

What Makes a Self-Directed IRA Different?

A self-directed IRA is not a separate type of retirement account under IRS rules. Instead, it is a traditional or Roth IRA administered by a Custodian that permits a wider range of permissible investments.

Like other IRAs, contribution limits and tax treatment generally remain the same. For 2026, eligible investors can contribute up to $7,500 annually, with an additional $1,100 catch-up contribution available for individuals aged 50 and older.

The primary difference lies in Investment flexibility rather than tax treatment.

The Appeal of Greater Investment Control

Supporters of self-directed IRAs argue that investors should not be limited to publicly traded stocks, bonds, and mutual funds.

These accounts can provide exposure to:

- Real estate investments.

- Private equity opportunities.

- Private Credit and lending arrangements.

- Certain precious metals that meet IRS standards.

- Limited interests in private businesses.

For investors with specialized knowledge in a particular Asset Class, this flexibility may create opportunities unavailable through traditional retirement accounts.

Diversification Beyond Public Markets

Many retirement portfolios are heavily concentrated in public equities and fixed income securities.

Alternative assets often respond differently to economic conditions than publicly traded investments. As a result, some investors use self-directed IRAs to diversify retirement holdings across multiple asset classes.

However, diversification alone does not eliminate risk. Many alternative investments carry unique challenges, including limited transparency, valuation uncertainty, and reduced liquidity.

The Risks Investors Often Overlook

A self-directed IRA is not automatically a superior retirement vehicle.

Alternative investments can be difficult to value and may not generate predictable Cash Flow. In addition, some assets can be difficult to sell quickly when funds are needed or when required minimum distributions must be taken.

Custodial and administrative costs are also typically higher than those associated with standard brokerage IRAs. These additional expenses can have a meaningful impact on long-term returns, particularly for smaller account balances.

Fraud Concerns Remain Significant

The SEC has repeatedly warned investors that self-directed IRAs can be attractive targets for investment fraud.

A common misconception is that the custodian reviews and approves investments held inside the account. In reality, custodians generally perform administrative functions and do not evaluate the legitimacy, quality, or investment merits of underlying assets.

As a result, investors bear primary responsibility for conducting Due Diligence. Regulators encourage investors to verify financial professionals through FINRA BrokerCheck and the SEC's Investment Adviser Public Disclosure database before committing retirement assets.

Understanding Prohibited Transactions

One of the most important risks involves prohibited transactions under Internal Revenue Code Section 4975.

The rules generally prohibit transactions between the IRA and certain disqualified persons, including the account owner, spouse, ancestors, descendants, and certain controlled entities.

For example, an investor cannot personally use real estate owned by the IRA or rent IRA-owned property to a close family member.

Violating these rules can cause the IRA to lose its tax-advantaged status, potentially triggering taxes and penalties.

Is a Self-Directed IRA the Best Choice?

There is no universally superior retirement account.

Investors with substantial expertise in real estate, private lending, or other alternative assets may find a self-directed IRA useful as part of a broader retirement strategy. Others may prefer the simplicity, lower costs, liquidity, and diversification offered by traditional brokerage IRAs.

The decision ultimately depends on investment knowledge, Risk tolerance, and the ability to manage ongoing compliance requirements.

Conclusion

Self-directed IRAs offer a level of investment control that traditional retirement accounts often cannot match. Access to alternative assets may appeal to investors seeking diversification beyond public markets or those with specialized expertise in a particular sector.

However, increased flexibility comes with meaningful trade-offs. Higher fees, liquidity challenges, fraud risks, and strict prohibited transaction rules require careful attention. For some investors, these benefits may outweigh the complexities. For others, a conventional IRA may remain the more practical and cost-effective retirement solution.

Please wait processing your request...

Please wait processing your request...