IRAs can hold a wide range of investments, but IRS rules restrict collectibles, Life insurance, and prohibited transactions. Here is a clear 2026 guide to permitted and restricted IRA Assets.

Key Highlights

- Most mainstream financial assets are permitted in an IRA, including stocks, ETFs, bonds and mutual funds.

- IRS rules prohibit collectibles and life insurance contracts inside IRAs.

- Prohibited transactions with disqualified persons can disqualify the entire retirement account.

Individual Retirement Accounts (IRAs) are often viewed as flexible Investment vehicles, but their boundaries are defined by tax law rather than investor preference. The Internal Revenue Service does not provide an exhaustive list of allowed investments. Instead, it defines prohibited categories and applies strict rules on transactions and ownership structures.

Understanding what an IRA can and cannot hold is essential for avoiding tax penalties and ensuring compliance with federal retirement regulations.

How IRA Investment Rules Are Structured

IRA investment rules are based primarily on two legal foundations:

- Section 408 of the Internal Revenue Code, which defines IRA eligibility and prohibited assets

- Section 4975, which governs prohibited transactions and disqualified persons

Rather than approving specific investments, the IRS restricts certain asset types and behaviors. Custodians then determine what investments they are willing to administer within those legal boundaries.

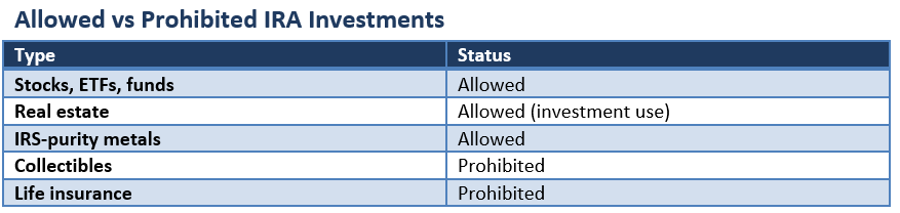

Commonly Permitted IRA Investments

Most traditional financial instruments are permitted inside IRAs. These include:

- Publicly traded stocks and equities

- Exchange-traded funds (ETFs)

- Mutual funds

- Government and corporate bonds

- Certificates of deposit (CDs)

- Money Market instruments

These assets form the core of most brokerage-based IRA portfolios due to their Liquidity, transparency and regulatory oversight.

Alternative Assets Often Held in IRAs

Beyond traditional markets, certain alternative assets may also be permitted, particularly through self-directed IRAs.

Common examples include:

- Real estate held strictly for investment purposes

- Private Equity and private Credit investments

- Limited liability company (LLC) interests

- Tax Lien certificates

- Certain precious metals that meet IRS purity requirements

- Cryptocurrency through approved custodial structures

While these assets may be permitted, they often require specialized custodians and additional compliance oversight.

Assets That Are Explicitly Prohibited

IRS rules clearly prohibit certain asset categories within IRAs.

Collectibles

Under Section 408(m), IRAs generally cannot hold collectibles, including:

- Artwork and antiques

- Rugs and rare items

- Gems and most precious stones

- Most coins (with limited exceptions for specific bullion coins)

- Alcoholic beverages and similar tangible collectibles

Life Insurance

Life insurance contracts are also prohibited within IRAs under Section 408(a). This restriction prevents IRAs from being used as insurance investment vehicles.

Prohibited Transactions and Disqualified Persons

Even if an asset is technically allowed, IRS rules under Section 4975 prohibit certain transactions involving “disqualified persons.”

These typically include:

- The IRA owner

- Spouse of the IRA owner

- Parents and grandparents

- Children and grandchildren

- Certain controlled entities and fiduciaries

Examples of prohibited activity include:

- Personally using IRA-owned real estate

- Renting IRA property to family members

- Selling personal assets to the IRA

- Providing services to IRA-held property

A prohibited transaction can result in the IRA losing its tax-advantaged status, creating immediate tax consequences.

Role of IRA Custodians

Custodians do not determine whether an investment is legally allowed under IRS rules. Instead, they decide what assets they are operationally willing to hold and administer.

This means two layers of restriction apply:

- IRS rules define what is legally permitted

- Custodians define what is practically available

As a result, investment choice can vary significantly across IRA providers.

Practical Considerations for Investors

While many assets are technically permitted, practical constraints often matter more than legal eligibility.

Key considerations include:

- Liquidity: Some assets may be difficult to sell quickly

- Valuation: Private and alternative assets may lack transparent pricing

- Fees: Self-directed IRAs often carry higher administrative costs

- Compliance complexity: Alternative assets require stricter documentation and monitoring

These factors can materially affect long-term retirement outcomes.

Conclusion

IRAs offer broad investment flexibility, but they are not unrestricted investment accounts. The IRS draws clear boundaries around prohibited assets such as collectibles and life insurance, while also enforcing strict rules on transactions involving disqualified persons.

For most investors, traditional financial assets remain the core of IRA portfolios due to their simplicity and regulatory transparency. Alternative investments may expand opportunity, but they also introduce additional complexity and compliance risk.

Understanding both the permitted investment universe and the underlying tax restrictions is essential for maintaining the integrity of retirement savings over time.

Please wait processing your request...

Please wait processing your request...