Self-directed IRA rules explained: Learn how alternative Assets, custodians, prohibited transactions, and IRS requirements shape retirement Investment control.

Key Highlights

- Self-directed IRAs allow retirement investors to access alternative assets beyond traditional stocks and bonds.

- Greater investment control comes with stricter compliance, valuation, and recordkeeping responsibilities.

- Prohibited transactions can trigger significant tax consequences and potentially disqualify an IRA.

As investors seek greater Diversification and control over retirement savings, self-directed IRAs have become an increasingly popular option. Unlike conventional retirement accounts that focus primarily on stocks, bonds, mutual funds, and Exchange-traded funds, self-directed IRAs can provide access to a much broader range of investments.

However, expanded flexibility also brings additional responsibilities. Understanding IRS rules, prohibited transactions, and valuation requirements is essential before moving retirement assets into alternative investments.

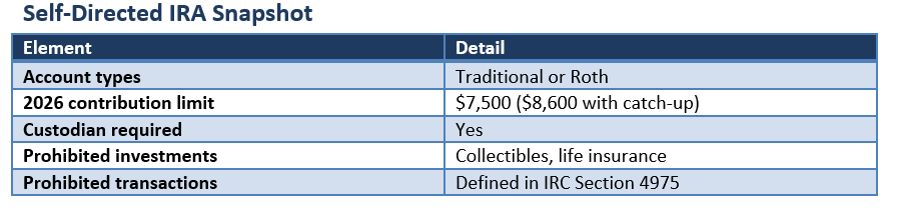

What Makes a Self-Directed IRA Different?

A self-directed IRA operates under the same tax framework as a traditional IRA or Roth IRA. The difference lies in the range of investments available.

Rather than being limited to a standard brokerage menu, account owners can direct retirement funds into alternative assets such as real estate, private companies, private lending arrangements, certain precious metals, and other qualifying investments.

The IRS generally focuses less on what investors can own and more on what they cannot own or how they use those assets.

The Custodian's Role Remains Essential

Despite the term "self-directed," investors cannot hold retirement assets directly.

Every IRA must be maintained through an IRS-approved custodian or Trustee. The custodian executes transactions, maintains records, and files required tax forms with the IRS.

Importantly, custodians typically do not evaluate investment quality, verify asset valuations, or determine whether an investment is suitable. Those responsibilities largely remain with the account owner.

Alternative Assets Expand Investment Choices

One of the main attractions of a self-directed IRA is broader portfolio diversification.

Common investments include rental properties, real estate Debt, Private Equity interests, Limited Liability company stakes, approved precious metals, tax liens, and certain crowdfunding opportunities.

These investments may offer diversification benefits, but they often carry greater Liquidity, valuation, and operational risks than publicly traded securities.

Understanding Prohibited Transactions

The greatest compliance risk for self-directed IRA investors is violating prohibited transaction rules.

The IRS prohibits self-dealing and transactions involving certain disqualified persons, including the account owner and close family members. For example, an IRA generally cannot purchase property already owned by the investor or provide personal benefits to the account holder.

Violations can result in severe tax consequences and potentially cause the account to lose its tax-advantaged status.

Valuation and RMD Challenges

Alternative assets often lack daily market pricing, making valuation more complex.

Custodians generally require annual fair-market-value reporting for IRS purposes. Investors holding Illiquid assets must also prepare for required minimum distributions once they reach the applicable age threshold for traditional IRAs.

Generating sufficient cash to satisfy distribution requirements can become challenging when retirement assets are tied up in private investments or real estate.

Investor Control Does Not Eliminate Risk

Greater investment freedom should not be confused with greater investment certainty.

The U.S. Securities and Exchange Commission has repeatedly warned investors that self-directed IRAs can be used to market speculative, illiquid, or fraudulent investments. Thorough Due Diligence remains essential regardless of the asset type involved.

Understanding the sponsor, Business model, valuation assumptions, and liquidity profile of each investment can be just as important as understanding the tax rules.

Conclusion

Self-directed IRAs offer Americans an opportunity to expand retirement portfolios beyond traditional financial assets. They provide access to real estate, private markets, and other alternative investments while retaining the tax advantages of a traditional or Roth IRA. Yet greater control comes with greater responsibility. Investors must navigate valuation requirements, prohibited transaction rules, and ongoing compliance obligations carefully. For many retirement savers, professional guidance can help balance the benefits of broader investment choice against the added complexity that accompanies self-direction.

Please wait processing your request...

Please wait processing your request...