Comparing an IRA and a taxable brokerage account? Learn how tax treatment, Withdrawal rules, contribution limits, and Investment flexibility differ in 2026.

Key Highlights

- IRAs provide tax advantages, while taxable brokerage accounts offer greater flexibility and unrestricted access to funds.

- Traditional IRAs may offer tax-deferred growth, while Roth IRAs can provide tax-free qualified withdrawals.

- Many investors use both account types to balance tax efficiency with Liquidity and investment flexibility.

For many investors, the decision is not whether to choose an IRA or a taxable brokerage account, but how to use both effectively. Each account serves a different purpose, and understanding the trade-offs can help investors align their savings strategy with retirement goals, tax considerations, and liquidity needs.

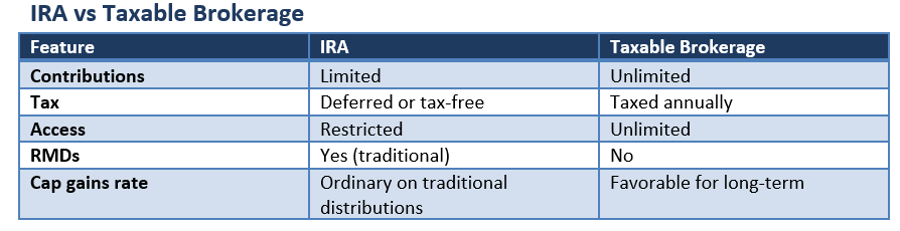

While IRAs are designed to encourage long-term retirement saving through tax benefits, taxable brokerage accounts provide unrestricted access to Capital and greater flexibility. The optimal choice often depends on an investor's time horizon, income level, and financial objectives.

How Tax Treatment Differs

One of the biggest distinctions between these accounts is how investment income is taxed.

Traditional IRAs generally allow investments to grow on a tax-deferred basis. Taxes are typically paid when funds are withdrawn in retirement. Roth IRAs operate differently, with contributions made using after-tax dollars and qualified withdrawals generally remaining tax-free.

Taxable brokerage accounts receive no special Tax Shelter. Interest, dividends, and realized capital gains may generate tax obligations during the year they are earned or realized.

However, taxable accounts do benefit from favorable Long-term capital gains tax rates when qualifying investments are held for more than one year.

Contribution Limits Matter

IRAs come with annual contribution restrictions established by the IRS.

For 2026, eligible individuals can contribute up to $7,500 annually, with an additional $1,100 catch-up contribution available for those aged 50 and older.

Taxable brokerage accounts have no contribution limits. Investors can deposit as much capital as they choose, making these accounts useful once retirement-account contribution limits have been reached.

For higher-income households seeking additional investment capacity, this flexibility can be a significant advantage.

Access to Funds and Liquidity

Retirement accounts are designed for long-term savings, which means access rules apply.

Traditional IRA withdrawals before age 59½ may be subject to taxes and an additional 10% penalty unless an exception applies. Roth IRAs offer greater flexibility for contributions but still maintain rules governing Earnings withdrawals.

Taxable brokerage accounts generally have no age-based withdrawal restrictions or early-access penalties. Investors can buy, sell, and withdraw funds whenever needed.

This liquidity makes brokerage accounts attractive for goals that may arise before retirement.

Required Minimum Distributions

Another important distinction involves required minimum distributions (RMDs).

Traditional IRA owners generally must begin taking RMDs at age 73 under current IRS rules. Failure to do so can result in penalties.

Taxable brokerage accounts do not require minimum withdrawals. Investors retain complete control over when Assets are sold and when gains are realized.

Roth IRAs also do not require RMDs during the original owner's lifetime.

Investment Choices and Control

Both account types provide access to a wide range of investments, including stocks, bonds, mutual funds, and Exchange-traded funds.

Some self-directed IRAs can also hold alternative assets such as real estate, private placements, or precious metals. However, these arrangements often involve specialized custodians and additional compliance requirements.

Taxable brokerage accounts typically offer broader platform flexibility and fewer administrative restrictions.

Why Many Investors Use Both

Rather than viewing the accounts as competitors, many investors use them together.

An IRA can help maximize tax advantages and retirement savings, while a taxable brokerage account can provide liquidity, flexibility, and additional investment capacity beyond IRS contribution limits.

Combining both accounts may allow investors to diversify not only investments but also future tax exposure and withdrawal Options.

Conclusion

The IRA versus taxable brokerage account debate ultimately comes down to priorities. Investors seeking tax-advantaged retirement growth may favor IRAs, while those who value unrestricted access and unlimited contributions may prefer taxable brokerage accounts.

Because each account offers distinct benefits, many households incorporate both into a broader financial strategy. Understanding the tax rules, withdrawal restrictions, and contribution limits can help investors determine how each account fits within their long-term Wealth-building objectives.

Please wait processing your request...

Please wait processing your request...