IRA overcontributions can trigger a 6% annual IRS excise tax until corrected. Learn how excess IRA contributions happen, available correction methods, and how to avoid costly retirement account penalties in 2026.

Key Highlights

- Excess IRA contributions may trigger a 6% IRS excise tax for every year they remain uncorrected.

- Removing excess contributions and associated Earnings before the tax deadline can help avoid penalties.

- Roth IRA income limits, contribution errors, and rollover mistakes are among the most common causes of overcontributions.

Contributing to an Individual Retirement Account (IRA) is one of the most effective ways to build retirement savings. However, exceeding IRS contribution limits can create unexpected tax consequences. While an IRA overcontribution is usually correctable, failing to address the issue promptly may result in recurring penalties that reduce long-term retirement Wealth.

Understanding how overcontributions occur and the available correction Options can help investors avoid unnecessary costs and maintain compliance with IRS retirement rules.

What Is an IRA Overcontribution?

An IRA overcontribution occurs when an investor contributes more than the annual IRS limit or makes a contribution that is not permitted based on eligibility requirements.

Several situations can create an excess contribution, including:

- Contributing more than the annual IRA limit.

- Making IRA contributions without sufficient Earned income.

- Exceeding Roth IRA income eligibility thresholds.

- Incorrectly reporting or processing rollover transactions.

- Making contributions to multiple IRA accounts that exceed the combined annual limit.

Because contribution rules vary based on income, filing status, and account type, excess contributions are more common than many investors realize.

The 6% IRS Excise Tax

The IRS generally imposes a 6% excise tax on excess IRA contributions for each year the excess amount remains in the account.

The penalty does not disappear automatically. If the overcontribution remains uncorrected, the excise tax can continue to apply annually, increasing the overall cost of the mistake.

For investors who discover an overcontribution early, acting before applicable tax deadlines can significantly reduce potential penalties.

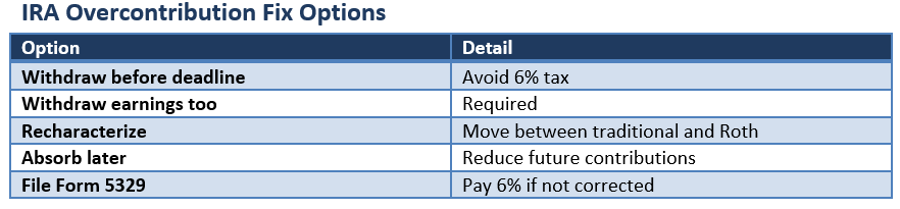

How to Correct an Excess IRA Contribution

The most straightforward correction method is to remove the excess contribution along with any earnings attributable to that contribution before the federal tax filing deadline, including extensions where applicable.

Removing both the excess amount and associated Investment gains is generally necessary to fully resolve the issue under IRS rules.

Many IRA custodians offer dedicated correction procedures and can assist account holders throughout the process.

Can You Recharacterize the Contribution?

In some circumstances, investors may be able to recharacterize an IRA contribution by moving it from one type of IRA to another, such as from a Roth IRA to a Traditional IRA.

Recharacterization may help resolve eligibility-related contribution issues, particularly when income exceeds Roth IRA limits. However, specific IRS requirements apply, and not every situation qualifies for this option.

It is also important to note that Roth conversion recharacterizations have generally not been permitted since 2018.

Using Future Contributions to Absorb the Excess

Some investors may be able to eliminate an excess contribution over time by reducing future-year contributions below the allowable limit.

This strategy can help correct certain overcontributions without withdrawing funds immediately. However, the 6% excise tax may continue to apply until the excess amount is fully absorbed, making early correction the more efficient solution in many cases.

Understanding Form 5329

If an excess contribution is not corrected before the applicable deadline, taxpayers may need to file IRS Form 5329.

This form is used to calculate and report the excise tax associated with excess IRA contributions and certain other retirement-account penalties.

Proper filing helps ensure compliance while documenting any corrective actions taken.

Conclusion

IRA overcontributions are often the result of simple administrative mistakes, but they can become costly if left unresolved. The IRS generally imposes a 6% excise tax on excess contributions for every year they remain in an account, making prompt action important.

Whether the excess stems from Roth IRA income limits, contribution miscalculations, or rollover errors, investors have several correction options available. Reviewing contribution limits annually, monitoring eligibility requirements, and addressing mistakes before tax deadlines can help preserve the long-term benefits of tax-advantaged retirement savings.

Please wait processing your request...

Please wait processing your request...