Discover the most common IRA Investment mistakes in 2026, from overcontributions and missed RMDs to rollover errors and concentrated portfolios that can hurt retirement savings.

Key Highlights

- IRA overcontributions can trigger a 6% annual tax penalty until corrected.

- Prohibited transactions may cause an IRA to lose its tax-advantaged status.

- Missing required minimum distributions can result in costly IRS penalties.

Individual Retirement Accounts (IRAs) remain a cornerstone of Retirement Planning in the United States. While many investors focus on choosing the right investments, some of the most expensive mistakes stem from administrative oversights and tax-rule violations rather than portfolio selection.

From excess contributions to missed required minimum distributions (RMDs), seemingly minor errors can create penalties, unexpected taxes, and long-term setbacks for retirement goals. Understanding these common IRA investment mistakes can help investors protect their retirement savings and avoid unnecessary costs.

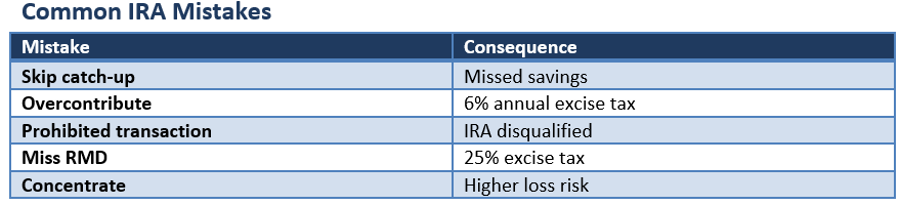

Missing Catch-Up Contributions

Many Americans aged 50 and older Fail to take advantage of catch-up contributions, despite the additional retirement-saving opportunity they provide.

For 2026, eligible investors can contribute an extra $1,100 beyond the standard IRA contribution limit. While this may seem modest, consistent catch-up contributions can meaningfully increase retirement Assets over time through the power of compounding.

Investors approaching retirement should review contribution limits annually to ensure they are maximizing available tax-advantaged savings opportunities.

Overcontributing to an IRA

Overcontributions remain one of the most common IRA mistakes, particularly among higher-income earners contributing to Roth IRAs.

Income thresholds and contribution limits can change periodically, making it easy to accidentally exceed permitted amounts. Excess contributions generally trigger a 6% excise tax for every year the excess remains in the account.

Monitoring annual income levels and contribution limits can help prevent avoidable penalties and administrative corrections.

Engaging in Prohibited Transactions

IRS rules prohibit certain transactions between an IRA and the account owner or other disqualified persons.

Examples may include using IRA-owned assets for personal benefit, lending money between the IRA and related parties, or personally using real estate held within a self-directed IRA.

The consequences can be severe. A prohibited transaction may cause the entire IRA to lose its tax-advantaged status, potentially creating significant tax liabilities. Investors using self-directed IRAs should pay particular attention to compliance requirements.

Missing Required Minimum Distributions

Required minimum distributions continue to be a major source of retirement-account penalties.

Traditional IRA holders generally must begin taking RMDs at age 73 under current rules. Failing to withdraw the required amount can result in a penalty equal to 25% of the shortfall. In some cases, the penalty may be reduced if the error is corrected promptly.

Retirees should monitor distribution deadlines carefully and ensure withdrawals are calculated accurately each year.

Holding an Overly Concentrated Portfolio

Some investors accumulate substantial exposure to a single stock, industry, or Asset Class within their IRA.

While concentration can amplify gains during favorable market conditions, it can also increase downside risk significantly. A sharp decline in a single investment may have an outsized effect on retirement savings that have taken decades to build.

Maintaining Diversification across sectors and asset classes can help reduce portfolio-specific risks over the long term.

Forgetting to Update Beneficiary Designations

Beneficiary forms are often neglected after major life events such as marriage, divorce, remarriage, or the birth of children.

An outdated beneficiary designation may result in retirement assets passing to unintended recipients. Because beneficiary forms generally govern IRA distributions after death, periodic reviews are an important part of retirement and estate planning.

Making Costly Rollover Errors

IRA rollovers can become problematic when investors misunderstand the rules.

The 60-day rollover requirement leaves little room for error. Missing the deadline may result in the distribution becoming taxable and, in some situations, subject to additional penalties.

Direct Trustee-to-trustee transfers are often preferred because they minimize administrative complexity and reduce the risk of accidental non-compliance.

Conclusion

Most IRA investment mistakes are avoidable. Overcontributions, prohibited transactions, missed RMDs, outdated beneficiary designations, and rollover errors typically arise from administrative oversights rather than poor investment decisions.

As retirement rules continue to evolve, investors who regularly review contribution limits, Withdrawal requirements, and account documentation may be better positioned to preserve the tax advantages of their IRA and strengthen their long-term retirement outlook. A proactive annual review can often prevent mistakes that become far more expensive to correct later.

Please wait processing your request...

Please wait processing your request...