_09_21_2025_14_23_42_317319.jpg)

Image source: © 2025 Krish Capital Pty.Ltd

Highlights

- Social Security, employer-sponsored plans, and personal savings form the core of retirement income.

- Tax-advantaged accounts like 401(k)s and IRAs provide long-term growth opportunities.

- Planning for Medicare coverage and future long-term care needs is a vital part of managing retirement income.

- Budgeting for inflation and healthcare costs helps prevent shortfalls in later years.

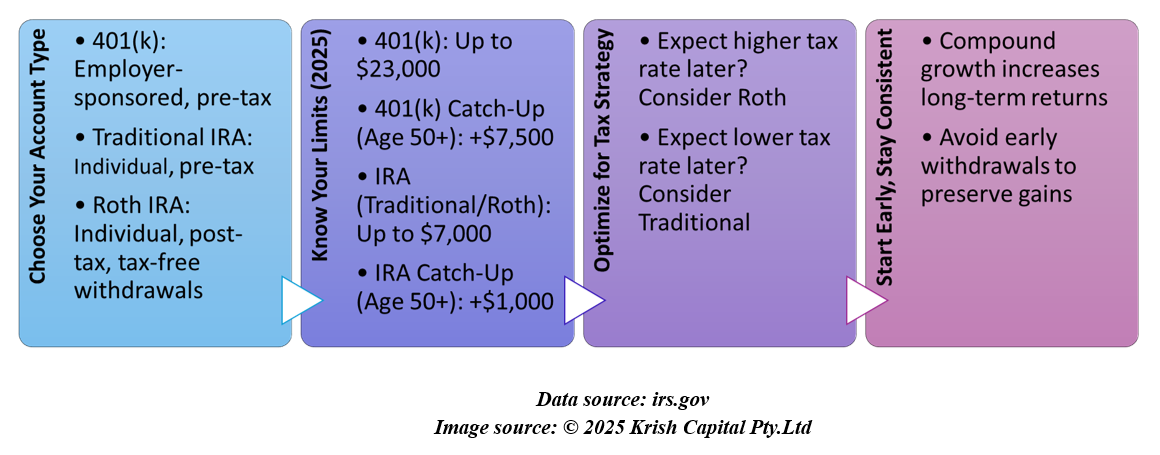

Moving from a steady paycheck to drawing retirement income requires deliberate financial planning to stay on track. In the US, retirement savings accounts are designed to help individuals build long-term financial security while offering tax advantages. The most common types include Individual Retirement Accounts (IRAs) and employer-sponsored plans such as 401(k)s. These accounts allow people to contribute part of their income towards retirement, with investments growing either tax-deferred or tax-free, depending on the account type. Contribution limits and eligibility criteria vary, but all are intended to encourage disciplined, long-term savings.

A Traditional IRA and a 401(k) both allow pre-tax contributions, meaning funds go in before income taxes are applied. This reduces taxable income in the year of contribution, but withdrawals in retirement are taxed as ordinary income. By contrast, a Roth IRA uses after-tax contributions but offers tax-free withdrawals of both contributions and investment gains in retirement, provided certain conditions are met. Some employers also offer Roth 401(k)s, combining the higher contribution limits of a 401(k) with the tax benefits of a Roth structure.

Maximizing Retirement Savings Through Tax-Advantaged Accounts

Integrating Healthcare and Insurance into Your Income Plan

Health-related expenses are a major financial concern for retirees. Medicare becomes available at the age of 65, but it does not cover everything, including most long-term care services. Planning for these costs in advance is essential to avoid depleting retirement savings.

The Centers for Medicare & Medicaid Services advises individuals to evaluate supplemental coverage options such as Medigap or Medicare Advantage plans. In addition, long-term care insurance may offer protection against extended nursing or in-home care expenses.

Budgeting for Longevity and Inflation

Outliving retirement savings is a common fear. To address this, retirees must prepare for inflation-adjusted living expenses and unexpected financial shocks. The Bureau of Labor Statistics reports that inflation can reduce purchasing power over time, especially in categories like housing, utilities, and medical care.

A realistic retirement budget should account for rising costs, potential changes in housing, and discretionary spending. Using tools such as the Consumer Expenditure Survey can help estimate future expenses and align them with income sources.

When and How to Transition

Experts recommend starting retirement planning at least a decade before exiting the workforce, ideally even earlier. Beginning early allows more time for your savings to grow, provides a buffer against market ups and downs, and gives you the flexibility to adapt your strategy over time. Early planning can reduce financial stress later and expand your retirement lifestyle options. This process includes estimating future income needs, consolidating retirement accounts, and reviewing investment allocations to ensure they align with your long-term goals.

Preparing for retirement income requires strategic planning across savings, social security, healthcare, and spending. Government resources provide essential tools to guide individuals through this transition and help them build a sustainable post-salary life.

Please wait processing your request...

Please wait processing your request...