Employer 401(k) vs IRA: Compare contribution limits, employer matching, Investment flexibility, fees, and retirement security strategies for U.S. savers in 2026.

Key Highlights

- Employer 401(k) plans provide higher contribution limits and valuable matching contributions.

- IRAs offer broader investment choices and greater account portability.

- Many retirement professionals view combining both accounts as a practical long-term retirement strategy.

Employer 401(k) vs IRA: Understanding the Retirement Security Debate

For most Americans, retirement security depends on accumulating Assets through workplace retirement plans and personal savings accounts. Two of the most widely used vehicles are employer-sponsored 401(k) plans and Individual Retirement Accounts (IRAs).

While both offer tax advantages and Long-term Growth potential, they serve different purposes within a retirement strategy. Understanding their strengths and limitations can help investors build a more resilient retirement portfolio.

Why Employer 401(k) Plans Remain Powerful

The biggest advantage of a 401(k) plan is scale.

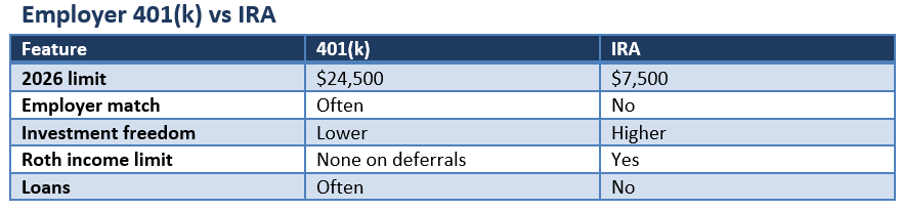

For 2026, employees can contribute up to $24,500 through salary deferrals, substantially higher than IRA contribution limits. Many employers also offer matching contributions, effectively adding extra retirement savings at no direct cost to the employee.

Over decades of investing, employer matching can significantly enhance retirement account balances and compound growth.

For workers with access to a match, this feature alone often makes a 401(k) a foundational retirement savings tool.

Where IRAs Offer Greater Flexibility

IRAs provide a level of investment freedom that many workplace plans cannot match.

Most 401(k) plans limit participants to a curated menu of mutual funds and investment Options selected by the employer. By contrast, IRAs generally provide access to a broader range of securities, including stocks, bonds, Exchange-traded funds, and specialized investment vehicles.

This flexibility allows investors to build portfolios that align more closely with their personal objectives, Risk tolerance, and retirement timeline.

IRAs also remain with the individual regardless of Job changes, making them highly portable.

Fees Can Influence Long-Term Outcomes

Investment costs can have a meaningful effect on retirement Wealth accumulation.

Some large employer-sponsored plans offer institutional pricing and low-cost investment options. Others may carry higher administrative expenses or limited fund choices.

IRAs at major brokerage firms often provide access to low-cost funds and commission-free trading, although costs vary by provider and investment selection.

Comparing fees regularly can help investors improve long-term net returns.

Roth Features and Borrowing Rules

Both account types offer Roth options, but eligibility rules differ.

Roth 401(k) contributions are generally available regardless of income level. Roth IRAs, however, are subject to annual income limits established by the IRS.

Another distinction involves Liquidity. Many 401(k) plans permit participant loans under plan rules, while IRA owners cannot borrow from their accounts without triggering tax consequences and potential penalties.

Why Many Savers Use Both Accounts

Increasingly, Retirement Planning is built around multiple account types rather than a single solution.

A common approach is to contribute enough to a workplace plan to capture the full employer match and then use an IRA to gain additional investment flexibility. Higher-income savers may continue contributing to both accounts where permitted under applicable tax rules.

This layered approach can diversify tax treatment, increase contribution capacity, and reduce dependence on a single retirement vehicle.

Conclusion

Employer-sponsored 401(k) plans and IRAs are not competing retirement solutions so much as complementary ones. A 401(k) offers higher contribution limits and the potential benefit of employer matching, while an IRA provides greater investment flexibility and portability. For many Americans, combining the strengths of both accounts may create a more balanced and durable retirement strategy. As retirement needs evolve, reviewing contribution levels, investment choices, fees, and tax considerations can help ensure long-term financial security remains on track.

Please wait processing your request...

Please wait processing your request...