Defined benefit pension vs self-directed IRA: Compare retirement income security, Investment control, portability, risks, and long-term Retirement Planning Options.

Key Highlights

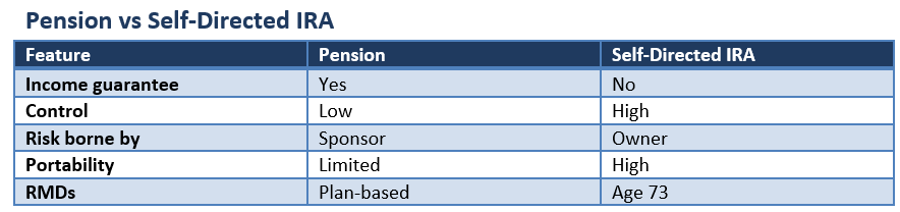

- Defined benefit pensions provide predictable retirement income but offer little investment control.

- Self-directed IRAs give investors broad authority over investments but transfer Market Risk to the account owner.

- Many retirees combine guaranteed income sources with self-managed retirement accounts to balance security and flexibility.

Retirement planning often involves a trade-off between certainty and control. Few comparisons illustrate this more clearly than the choice between a defined benefit pension and a self-directed IRA.

One approach focuses on delivering predictable retirement income. The other emphasizes investment flexibility and personal decision-making. Understanding how each structure works can help investors evaluate their long-term retirement strategy.

What Is a Defined Benefit Pension?

A defined benefit pension is an employer-sponsored retirement plan that promises a specific retirement benefit based on a formula, often tied to salary history and years of service.

The employer is generally responsible for funding the plan and managing its investments. Participants receive retirement income according to plan terms, regardless of how underlying investments perform.

This structure shifts much of the investment and longevity risk away from employees and onto the plan sponsor.

Why Pensions Appeal to Retirees

The primary attraction of a defined benefit pension is income certainty.

Retirees typically receive regular monthly payments that continue throughout retirement. This predictable Cash Flow can simplify budgeting and reduce concerns about market Volatility.

Many private-sector pensions also receive protection from the Pension Benefit Guaranty Corporation (PBGC), which may provide benefits if a covered plan becomes insolvent, subject to federal limits.

For investors prioritizing financial stability, pensions can serve as a valuable retirement income foundation.

Understanding Self-Directed IRAs

A self-directed IRA takes a very different approach.

Instead of guaranteeing future income, the account gives investors broad control over how retirement Assets are invested. Depending on the Custodian, investments may include stocks, bonds, real estate, Private Equity, private lending, and certain precious metals.

The account owner determines the investment strategy and bears responsibility for the results.

This flexibility appeals to investors who want greater involvement in Portfolio Management and asset selection.

The Trade-Off Between Control and Risk

The advantages of a self-directed IRA are closely tied to its risks.

Broader investment freedom may create opportunities for Diversification and Long-term Growth. However, investors assume responsibility for market fluctuations, asset selection, compliance requirements, and retirement income planning.

Unlike a pension, a self-directed IRA does not guarantee monthly income. Future retirement resources depend largely on investment performance and Withdrawal decisions.

As a result, retirement outcomes can vary significantly from one investor to another.

Portability and Ownership Matter

Another important distinction involves portability.

Self-directed IRAs remain under the individual's ownership and can generally move with the investor throughout different stages of employment and retirement.

Pensions are typically tied to a specific employer and governed by plan-specific distribution rules.

For workers who change jobs frequently, personal retirement accounts often provide greater flexibility.

Why Many Retirees Use Both

Increasingly, retirement planning is not an either-or decision.

Many Americans combine multiple retirement income sources, including pensions, IRAs, 401(k) plans, Social Security benefits, and taxable investment accounts.

This diversified approach can help balance income stability with investment flexibility while reducing dependence on any single source of retirement funding.

Conclusion

Defined benefit pensions and self-directed IRAs represent two very different retirement philosophies. Pensions prioritize income security, professional management, and predictable cash flow, while self-directed IRAs emphasize investment choice, portability, and personal control. Neither structure is inherently superior in every situation. The most effective retirement strategy often depends on an individual's Risk tolerance, income needs, investment knowledge, and long-term financial objectives. For many investors, combining guaranteed income sources with self-managed retirement assets may provide a balanced path toward retirement security.

Please wait processing your request...

Please wait processing your request...