Can you manage your own retirement account in the USA? Learn how IRAs, Roth IRAs, self-directed IRAs, and Solo 401(k)s provide Investment control.

Key Highlights

- Americans can directly manage retirement investments through IRAs, Roth IRAs, self-directed IRAs, and Solo 401(k) plans.

- Greater investment control often comes with increased compliance and recordkeeping responsibilities.

- Self-directed IRAs and Solo 401(k)s provide the broadest access to alternative investments.

Many investors assume retirement savings must remain inside employer-selected funds or professionally managed portfolios. In reality, Americans have several Options that allow substantial control over retirement investments.

Whether through an IRA, Roth IRA, self-directed IRA, or Solo 401(k), investors can often choose their own Assets, build customized portfolios, and tailor retirement strategies to their financial goals. The trade-off is that greater control typically means greater responsibility.

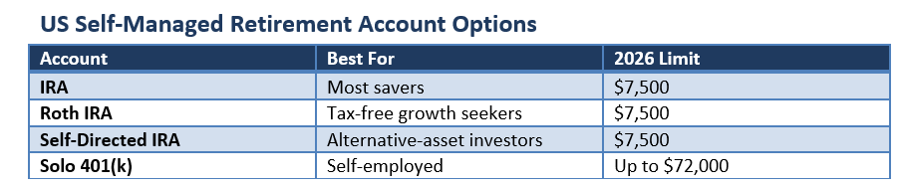

IRA: A Flexible Starting Point

The Individual Retirement Account (IRA) remains one of the most widely used retirement vehicles in the United States.

For 2026, eligible individuals can contribute up to $7,500 annually, with additional catch-up contributions available for those aged 50 and older.

Traditional IRAs allow investors to select from a broad range of publicly traded investments, including stocks, bonds, mutual funds, and Exchange-traded funds. Depending on income and workplace retirement-plan participation, contributions may be tax deductible.

For many investors, an IRA provides a straightforward path to retirement account self-management.

Roth IRA: Greater Tax Flexibility

A Roth IRA offers many of the same investment choices as a traditional IRA but differs in tax treatment.

Contributions are generally made with after-tax dollars, while qualified withdrawals may be tax-free in retirement. This feature makes Roth accounts attractive to investors seeking long-term tax Diversification.

However, Roth IRA eligibility is subject to income limits, which can restrict direct contributions for higher-income households.

Self-Directed IRA: Expanding Investment Choices

Investors seeking broader flexibility often consider self-directed IRAs.

These accounts operate under the same tax framework as traditional or Roth IRAs but permit a wider range of investments. Depending on the Custodian, investors may gain access to real estate, Private Equity, private lending, certain precious metals, and other alternative assets.

The expanded investment universe can increase diversification opportunities, but it also introduces additional compliance, valuation, and prohibited transaction considerations.

Solo 401(k): Designed for Self-Employed Investors

For Business owners and self-employed professionals, the Solo 401(k) offers one of the most flexible retirement structures available.

Eligible participants can make both employee and employer contributions, allowing significantly larger annual retirement savings than an IRA. Total contributions may reach up to $72,000 in 2026, subject to IRS rules.

Many Solo 401(k) plans also support Roth contributions and, in some cases, broader investment authority through self-directed structures.

What Self-Management Actually Means

Managing your own retirement account does not mean personally holding retirement assets or bypassing regulatory requirements.

All IRAs must be maintained through an IRS-approved custodian or Trustee, while Solo 401(k) plans must comply with applicable retirement-plan regulations. Investors remain responsible for understanding contribution limits, prohibited transaction rules, reporting requirements, and distribution obligations.

Greater autonomy requires greater oversight.

Choosing the Right Account

The best account depends on employment status, income level, tax objectives, and investment preferences.

Traditional and Roth IRAs often suit investors seeking simplicity and flexibility. Self-directed IRAs appeal to those pursuing alternative investments. Solo 401(k)s may be particularly attractive for self-employed individuals seeking higher contribution limits and expanded retirement-planning opportunities.

Conclusion

Americans have multiple options for managing their own retirement investments. Traditional IRAs, Roth IRAs, self-directed IRAs, and Solo 401(k)s each offer varying levels of control, flexibility, and tax advantages. While self-management can provide greater customization and broader investment opportunities, it also increases responsibility for compliance and long-term planning. Understanding the strengths and limitations of each account type is essential when building a retirement strategy aligned with individual financial goals.

Please wait processing your request...

Please wait processing your request...