Summary

- Broker Wells Fargo raised its rating on clothing brand Gap from ‘equal weight’ to ‘overweight’.

- The broker also upped its price target on GPS from US$11 to US$16.

- Gap reported net sales of US$3.55 billion and a net income of US$117 million in Q2 2023.

Retailer Gap Inc. (NYSE: GPS) received a rating and price target upgrade from broker Wells Fargo. Praising clothing retailer Gap’s turnaround story, Wells Fargo raised its rating on the stock from ‘equal weight’ to ‘overweight’.

The broker pointed out that Gap’s setup has become compelling with right-sized inventory, better cost controls and fresh management. The new team is expected to help reignite key brands, while the new CEO holds a strong track record with heritage brands.

The broker also stated that inventory is normalizing and the path to gross margin recovery is now visible.

GPS Share Price; Source: EODHD/Others

The stock closed at US$13.06 on Wednesday, October 25, 2023. At Wednesday’s market close, the stock was 5.2% higher intraday and 15.7% higher on a YTD basis. The stock hit its 52-week high of US$15.49 on February 3, 2023.

Wells Fargo sees a 22% upside potential in GPS

Broker Wells Fargo upped its price target on GPS from US$11 to US$16, with the new price target representing a 22% upside potential on Wednesday’s closing price.

EODHD/Others data shows that a total of 19 analysts have covered GPS, of which four have rated it ‘buy’ or higher. Of the remaining, ten have given GPS a ‘hold’ rating and five believe it to be a ‘sell’. The consensus mean price target on GPS is US$11.19, which GPS has already surpassed.

Broker Guggenheim had given GPS a price target of US$18 on September 12, 2023. Meanwhile, the stock has already surpassed the price target of US$11.50 given by broker Crispedia on August 11, 2023.

As per EODHD/Others data, Gap has a mean recommendation rating of 3 on five. Here, one represents a ‘strong buy’ rating while five showcases a ‘strong sell' rating.

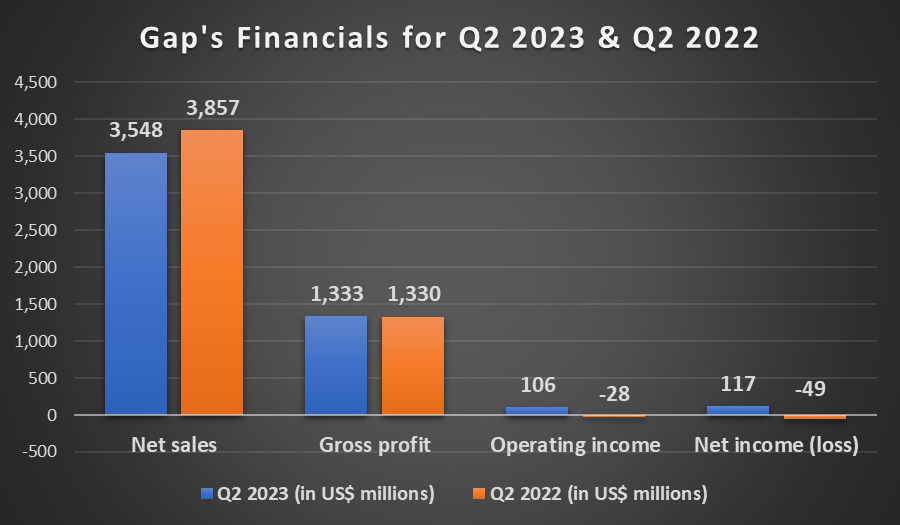

Gap’s financial results for Q2 2023

Gap’s net sales reached US$3.55 billion in Q2 2023, reflecting an 8% decrease compared to the previous year. This decline is attributed to factors such as an estimated 1% foreign exchange challenge and a 2% negative impact from the sale of Gap China.

Gross margin for the quarter stood at 37.6%, marking a 310-basis-point increase compared to last year's reported gross margin and a 160-basis-point increase compared to last year's adjusted gross margin, which did not include US$58 million in inventory impairment charges.

Image Source: ©2023 Kalkine®; Data Source: Company Reports

For Q2 2023, the company reported an operating income of US$106 million and a net income of US$117 million, resulting in reported diluted earnings per share of US$0.32.

The cash and cash equivalents at the end of the quarter amounted to US$1.4 billion, 91% higher over the previous corresponding period.

_06_27_2026_21_16_35_168117.jpg)

Please wait processing your request...

Please wait processing your request...