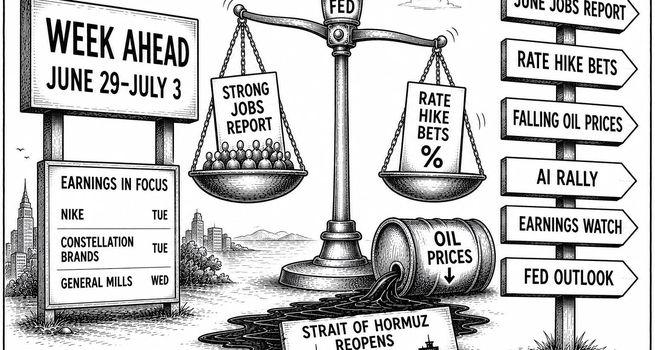

U.S. markets close out a solid first half as the June nonfarm payrolls report on Thursday, ADP employment, JOLTS job openings, and ISM Manufacturing PMI converge with a shortened trading week ahead of the Independence Day holiday, all against a backdrop of easing oil prices and rising rate hike expectations.

U.S. equity markets close out the first half of 2026 with the S&P 500 up more than 7% for the year, but June has been a rougher month, with semiconductor shares seeing outsized volatility as investors calibrate their AI optimism against a Federal Reserve that revealed at its June meeting a laser focus on containing inflation.

PCE data released Thursday showed inflation breaking above 4% for the first time in three years, and Fed funds futures are now indicating better than even odds of a rate hike by the September meeting, a complete reversal from the start of the year when markets were pricing equity-friendly cuts. The Strait of Hormuz ceasefire has driven oil from approximately $100 a barrel a month ago to the $70 range, the most significant disinflationary development of the year. Whether that easing is durable or temporary remains the dominant question as the June jobs report on Thursday becomes the week's defining data point and the clearest signal yet of whether the Fed's next move is a hike or a hold.

Monday, June 29

Market

No economic data or Fed speakers are scheduled. Markets open at the start of the final week of the first half, with attention turning immediately to the week's labour data sequence. The Strait of Hormuz ceasefire and the fall in oil to the $70 range provide a more constructive backdrop than any week in the past four months, but the Fed's hawkish June meeting has reset expectations in ways that oil alone cannot unwind.

Tuesday, June 30

Earnings

Nike (NYSE:NKE) reports in the afternoon as the week's most consequential earnings event and a direct read on discretionary consumer spending under the weight of four months of elevated energy costs. Its results will be watched for evidence of whether falling gasoline prices are beginning to free up household spending for non-essential categories, and for any commentary on international revenue trends given the broader geopolitical and currency dynamics at play. Constellation Brands (NYSE:STZ) also reports Tuesday afternoon, offering an alcohol beverage read on consumer staples spending resilience.

Economic Data

Tuesday carries the week's heaviest data load outside of Thursday. The S&P Case-Shiller Home Price Index for April, prior at 1.2%, provides a lagged but structurally important read on residential real estate valuations. The Conference Board Consumer Confidence Index for June, prior at 93.1, offers a more immediate sentiment read and will be watched for any evidence that falling oil prices and the Iran ceasefire are translating into improved household confidence. JOLTS job openings for May provide the first labour market signal ahead of Thursday's payrolls, with prior job openings at an unspecified level and the consensus pointing to a slowdown to 7.28 million from April's reading. The Chicago Business Barometer PMI for June, prior at 62.7, rounds out Tuesday's calendar.

Wednesday, July 1

Earnings

General Mills (NYSE:GIS) reports before the open, providing a consumer staples and food price inflation read. Its results and commentary on input cost trends will be watched for any early evidence that the easing in energy prices is beginning to flow through to food production costs and consumer price stability at the grocery level.

Economic Data

Wednesday carries the week's manufacturing and employment preview data. ADP private employment for June, prior at 122,000, provides an early directional signal ahead of Thursday's official payrolls. The consensus points to 118,000 private sector jobs added, a slight deceleration from the prior month. ISM Manufacturing PMI for June, prior at 54.0, is forecast to ease slightly to 53.7, still solidly in expansion territory but worth watching for any demand softening tied to the post-ceasefire energy price repricing. The S&P Global US Manufacturing PMI for June, prior at 55.1, provides a cross-check. Construction spending for May, prior at 0.4%, rounds out Wednesday's releases.

Thursday, July 2

Earnings

No major earnings are scheduled Thursday. The focus is entirely on the morning's labour market data.

Economic Data

The June nonfarm payrolls report is the week's defining release. Consensus points to 114,000 jobs added in June, a deceleration from May's 172,000, with the unemployment rate expected to hold at 4.3% for a fifth consecutive month. Average hourly earnings are forecast at 0.3% month-on-month and 3.5% year-on-year, unchanged from May's readings. The composition of the report will matter as much as the headline: a print above 150,000 risks being read as evidence of an overheating economy that would accelerate the rate hike timeline and push Treasury yields higher at a moment when the market is already on edge. A miss below consensus would temper rate hike fears but raise questions about whether the AI-driven growth narrative can sustain equity valuations with the labour market softening. Weekly jobless claims for the week ending June 27 arrive simultaneously, providing the most current real-time labour market read. Factory orders for May, prior at 4.8%, close Thursday's calendar.

Friday, July 3

Market Holiday

U.S. financial markets are closed for the Independence Day holiday. The shortened trading week means Thursday is the only session available to digest the jobs report before the long weekend, a compression that may amplify post-payrolls volatility into a single trading day.

Geopolitical Backdrop

The Strait of Hormuz ceasefire and the resulting fall in oil prices to the $70 range from approximately $100 a month ago represent the most significant disinflationary development of 2026. The volume of tankers crossing the Strait picked up toward the end of June, and energy prices have tumbled, directly easing the market's view of pro-inflationary risk and reducing near-term rate hike probability. However, whether the truce has staying power and whether it translates into a durable normalisation of oil supply routes, a process that could take months even under the most optimistic scenario, remains the dominant uncertainty heading into the second half.

Fed Chair Warsh and Bank of Canada Governor Macklem are both speaking at the ECB's annual Forum on Central Banking this week, in what will be among the first extended public remarks from Warsh since his hawkish June 17 meeting. His comments at the forum will be parsed for any nuance on how the Strait ceasefire and the resulting oil price decline are factoring into his inflation assessment, and whether the September rate hike that futures are now pricing at better than even odds remains his base case or is already being reconsidered in light of easing energy costs.

The Week in Context

By Thursday's close, before the Independence Day holiday compresses the reaction window, the first half of 2026 will have been definitively characterised. The S&P 500's 7% year-to-date gain masks a more complex underlying story: a market driven increasingly by AI-related semiconductors, navigating a Fed that has pivoted from cut expectations to hike probability in six months, sustained by an energy shock that has now partially reversed. The June jobs report will either validate the soft-landing scenario, where the economy generates enough growth to sustain earnings without overheating into a rate hike, or tilt the Fed decisively toward September action. Either outcome resets the second half's policy narrative before the July earnings season begins.

_06_27_2026_21_16_35_168117.jpg)

Please wait processing your request...

Please wait processing your request...