Key Highlights

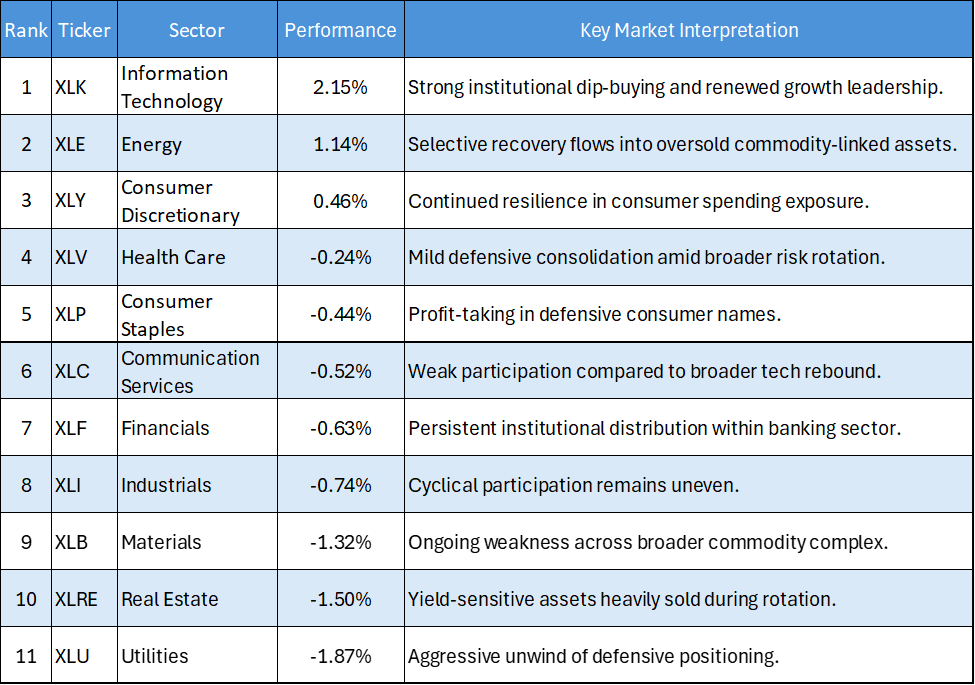

- Technology Leads Aggressive Market Recovery: Information Technology (XLK) surged 2.15%, decisively leading the US sector leaderboard as institutional investors aggressively rotated back into high-growth exposure. The sharp rebound suggests active managers are rapidly unwinding defensive positioning and re-entering secular growth Assets following the recent correction.

- Energy Stages Tactical Rebound: Energy (XLE) advanced 1.14%, marking one of the strongest recoveries among cyclical sectors. The rally indicates that deeply oversold Commodity-linked equities are beginning to attract selective bargain-hunting flows from institutional desks.

- Defensive Sectors Experience Heavy Profit-Taking: Utilities (XLU) declined 1.87%, while Real Estate (XLRE) dropped 1.50% and Consumer Staples (XLP) fell 0.44%. The synchronized weakness across defensive Yield sectors confirms that investors are actively rotating Capital away from safety trades and back toward higher-Beta opportunities.

- Consumer Discretionary Continues Relative Strength: Consumer Discretionary (XLY) gained 0.46%, outperforming broader defensive sectors and reaffirming institutional confidence in resilient US consumer spending trends despite ongoing macro uncertainty.

The US Equity market session on June 8, 2026, marked a significant Reversal in sector Leadership dynamics following the previous session’s sharp risk-off Liquidation. Institutional capital aggressively rotated away from defensive sectors and back into high-growth and cyclical exposures, producing a highly tactical recovery rally led by Technology and Energy.

Importantly, the rebound was not broad-based across all sectors. Instead, the market displayed highly selective institutional positioning. Growth-oriented sectors such as Technology attracted concentrated buying interest, while traditionally defensive sectors simultaneously suffered aggressive de-risking activity. This divergence suggests that investors are transitioning toward a rotational, stock-picker-driven environment rather than a synchronized macro expansion.

Daily US Sector Performance Summary

The following table summarizes the performance of the major US sectors from strongest to weakest return:

Key Market Themes

Technology Reclaims Institutional Sponsorship

- The defining development of the session was the explosive rebound in Information Technology (XLK). After experiencing significant liquidation pressure during the prior selloff, the sector re-emerged as the dominant leadership engine of the market. The 2.15% surge reflects more than a short-covering rally; it signals renewed institutional sponsorship of secular growth exposure as portfolio managers reposition for potential medium-term recovery.

- The recovery in XLK occurred simultaneously with aggressive selling across Utilities and Real Estate, confirming that investors were actively reallocating capital from defensive sectors into high-duration growth assets rather than simply deploying fresh Liquidity into the market.

Defensive Rotation Begins to Reverse

- The defensive trade that dominated recent sessions showed clear signs of exhaustion. Utilities (XLU), Real Estate (XLRE), and Consumer Staples (XLP) all suffered coordinated declines as institutional desks harvested profits from previously overcrowded safety trades.

- Utilities’ sharp 1.87% decline was particularly notable from a structural perspective. The sector had recently served as one of the market’s primary Volatility shelters, but its breakdown now suggests that investors are becoming increasingly comfortable reintroducing cyclical and growth-oriented exposure into portfolios.

Energy Attracts Selective Recovery Flows

- Energy (XLE) delivered one of the strongest performances of the session, advancing 1.14% following a period of sustained weakness. The magnitude of the rebound indicates that active managers are beginning to selectively accumulate discounted commodity-linked assets amid improving short-term risk appetite.

- However, Materials (XLB) failed to participate meaningfully in the recovery rally, declining another 1.32%. This divergence suggests institutional investors currently prefer targeted energy exposure rather than broad-based reaccumulation across the wider commodity complex.

Financials Continue to Lag

- Despite the broader recovery in risk sentiment, Financials (XLF) remained under pressure, declining 0.63%. The continued weakness within the banking sector suggests institutional conviction remains limited, with financial stocks still functioning as a liquidity source for rotational flows into higher-growth opportunities.

- The inability of Financials to stabilize alongside the broader market recovery raises concerns regarding the durability of the rally. Historically, sustained bull phases become increasingly difficult when major banking institutions remain under persistent distribution pressure.

The June 8 session highlighted a major tactical rotation within the US equity market. Institutional capital aggressively rotated away from defensive yield-sensitive sectors and back into high-beta growth exposure, with Information Technology (XLK) emerging as the dominant leadership driver.

Nevertheless, the recovery remains highly selective rather than universally bullish. Technology and Energy attracted concentrated inflows, while Financials and Materials continued exhibiting structural fragility. This divergence reinforces the view that the market is transitioning toward a more tactical, rotation-driven environment rather than a synchronized broad-market advance.

Active managers should continue focusing on validated growth leadership and selectively improving cyclical sectors while maintaining disciplined risk management around structurally weak areas of the market. Technology (XLK) and Consumer Discretionary (XLY) currently remain among the strongest institutional accumulation zones, while ongoing weakness in Financials (XLF) and defensive sectors may continue driving elevated cross-sector volatility.

Please wait processing your request...

Please wait processing your request...