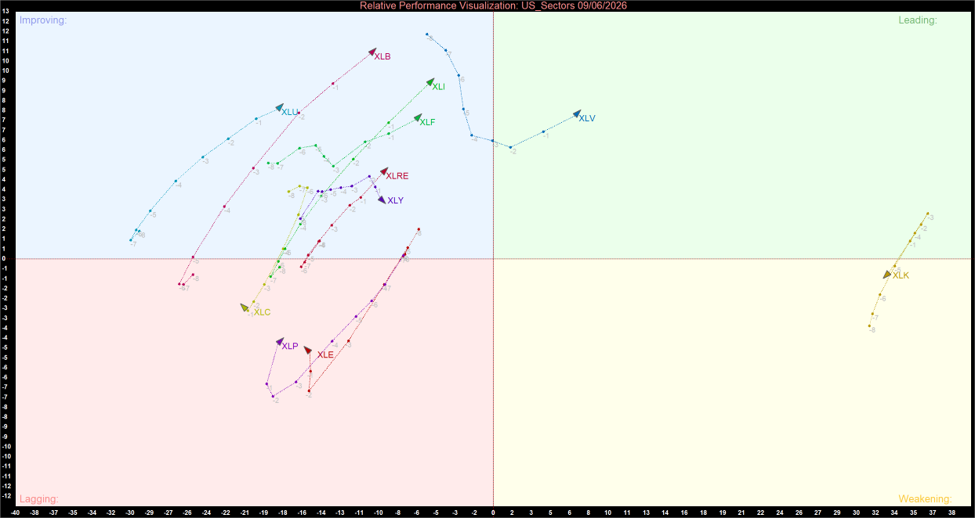

Key Momentum Highlights

- Health Care Emerges as the Market’s Primary Leadership Anchor: Health Care (XLV) remains the only sector positioned firmly inside the Leading quadrant, confirming sustained institutional sponsorship for defensive growth exposure. The sector’s continued North-East trajectory reflects improving relative strength and momentum despite broader market Volatility.

- Technology Recovery Accelerates but Leadership Remains Incomplete: Information Technology (XLK) delivered the strongest absolute performance of the session with a 2.15% rally. However, the sector remains trapped inside the Weakening quadrant, indicating that the rebound still represents an early-stage momentum recovery rather than a fully restored structural leadership regime.

- Defensive Yield Proxies Begin to Roll Over: Utilities (XLU) and Real Estate (XLRE) continue deteriorating despite remaining within the Improving quadrant. Their increasingly negative momentum vectors suggest institutional desks are actively unwinding defensive overcrowding as Capital rotates back toward selective growth and cyclical themes.

- Cyclical Sectors Show Early Signs of Stabilization: Industrials (XLI), Materials (XLB), and Financials (XLF) are all improving on a relative momentum basis. Although these sectors remain left of the relative-strength axis, their North-East trajectories suggest institutional investors are beginning to selectively rebuild cyclical exposure following the recent Liquidation phase.

The US Equity market continues undergoing a highly tactical rotational reset following the extreme volatility observed during the recent correction cycle. The Relative Rotation Graph (RRG) for June 9, 2026, reveals a fragmented market structure characterized by selective institutional accumulation rather than synchronized bullish participation.

Unlike traditional broad-market recoveries, the current environment displays substantial divergence across sectors. Defensive growth leadership remains concentrated in Health Care (XLV), while Technology (XLK) attempts to rebuild momentum following prior liquidation pressure. At the same time, defensive yield-sensitive sectors are beginning to lose institutional sponsorship as investors cautiously reintroduce cyclical exposure into portfolios.

Sector Momentum and Trajectory Summary

US Sector Relative Momentum Chart (at the closing price of 09/06/2026). Powered by: amibroker.com

Quantitative Momentum Themes

The Leading Quadrant (Institutional Leadership Zone)

- Health Care (XLV): Health Care remains the market’s strongest structural leadership sector. Positioned firmly inside the Leading quadrant, XLV continues exhibiting positive relative strength and momentum simultaneously. The sector’s persistent North-East trajectory confirms ongoing institutional Demand for Earnings stability, balance-sheet quality, and defensive growth characteristics.

The Weakening Quadrant (Leadership Under Pressure)

- Information Technology (XLK): Despite generating the strongest Absolute Return of the session, XLK remains positioned inside the Weakening quadrant. This divergence highlights that while institutional dip-buying activity has intensified significantly, the sector has not yet fully re-established dominant relative momentum leadership. The current rebound appears tactical and recovery-driven rather than a confirmed secular breakout.

The Improving Quadrant (Emerging Recovery Candidates)

- Industrials (XLI): Industrials continue improving steadily on a relative momentum basis. The sector’s constructive North-East trajectory suggests institutional investors are selectively rebuilding exposure toward economically sensitive sectors linked to infrastructure, Manufacturing, and logistics.

- Materials (XLB): Materials exhibit one of the strongest momentum improvement profiles on the matrix. Although relative strength remains negative overall, accelerating momentum suggests the previous Commodity liquidation cycle may be stabilizing.

- Financials (XLF): Financials are beginning to recover from recent weakness, with relative momentum gradually improving. However, the sector remains left of the relative-strength axis, implying institutional conviction toward the banking complex remains cautious rather than aggressively bullish.

- Utilities (XLU): Utilities remain technically positioned inside the Improving quadrant, but the sector’s trajectory is beginning to roll over sharply toward the South-West. This confirms that recent defensive overcrowding is being actively unwound as investors rotate capital away from low-volatility yield exposure.

- Real Estate (XLRE): Real Estate displays a similar pattern to Utilities. While short-term stabilization has emerged, deteriorating momentum vectors suggest institutional demand for yield-sensitive Assets is weakening rapidly.

- Consumer Discretionary (XLY): Consumer Discretionary continues hovering near the center of the matrix with relatively balanced positioning. Institutional conviction toward consumer spending trends remains stable, although momentum acceleration has moderated slightly.

The Lagging Quadrant (Structural Underperformers)

- Energy (XLE): Despite staging a strong absolute rebound of 1.14%, Energy remains deeply entrenched inside the Lagging quadrant. This divergence confirms that the latest recovery likely reflects tactical short-covering and oversold mean reversion rather than the beginning of a durable structural leadership cycle.

- Consumer Staples (XLP): Staples continue deteriorating after previously benefiting from defensive capital inflows. The sector’s South-West trajectory reflects fading defensive momentum and increasing institutional profit-taking.

- Communication Services (XLC): Communication Services remain isolated within the Lagging quadrant, confirming that institutional investors continue discriminating heavily within growth sectors. Capital remains concentrated in core Technology exposure while digital media and platform-related equities continue lagging.

Strategic Summary

The June 9 RRG structure confirms that the US equity market remains in a highly rotational and selective environment rather than a synchronized macro expansion phase. Health Care (XLV) currently represents the market’s cleanest leadership structure, while Technology (XLK) is attempting to rebuild institutional sponsorship following its recent correction.

At the same time, the breakdown in defensive yield sectors such as Utilities (XLU) and Real Estate (XLRE) suggests that institutional investors are becoming increasingly comfortable reducing safety exposure and selectively reintroducing cyclical risk.

Maintain tactical focus on sectors exhibiting improving momentum trajectories, particularly Technology (XLK), Industrials (XLI), and Materials (XLB), while remaining cautious toward structurally weak sectors still trapped within the Lagging quadrant. The current market structure continues favoring active rotational management, disciplined sector selection, and flexible risk allocation strategies over passive index exposure.

_06_12_2026_23_00_13_327450.jpg)

Please wait processing your request...

Please wait processing your request...