Key Highlights

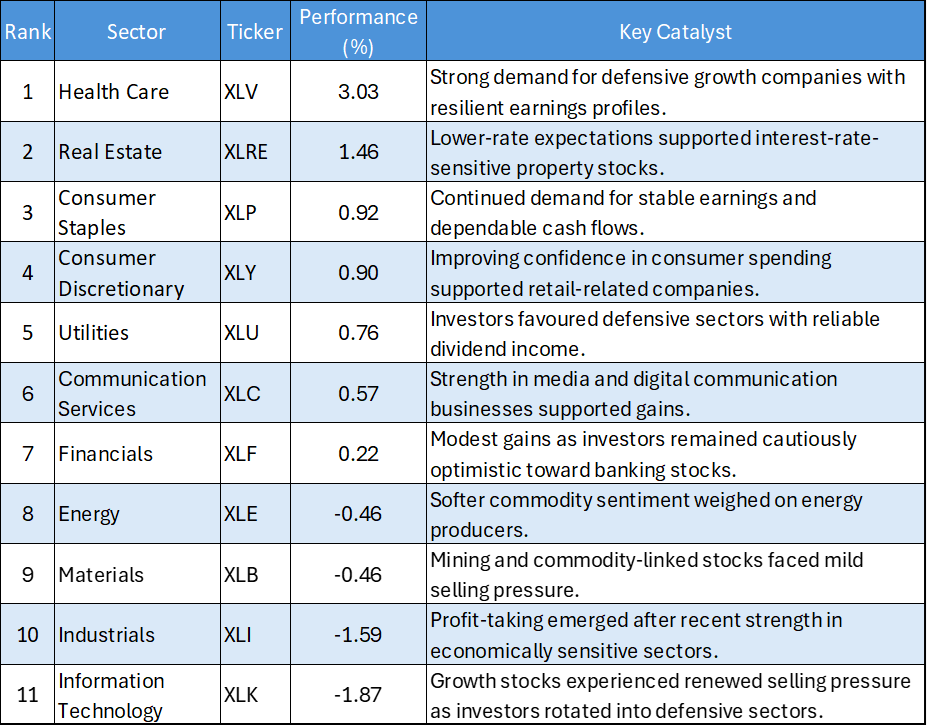

- Health Care Leads the Market: Health Care (XLV) climbed 3.03%, delivering the strongest performance of the session as investors sought defensive growth opportunities and stable earnings.

- Real Estate and Consumer Sectors Advance: Real Estate (XLRE), Consumer Staples (XLP), and Consumer Discretionary (XLY) posted solid gains, reflecting renewed confidence in interest-rate-sensitive and consumer-oriented industries.

- Broad-Based Strength Across Defensive Sectors: Utilities (XLU), Communication Services (XLC), and Financials (XLF) all finished higher, supporting overall market breadth.

- Technology and Industrials Under Pressure: Information Technology (XLK) and Industrials (XLI) recorded the largest declines of the session as investors rotated away from recent market leaders.

The US equity market delivered a mixed but generally constructive performance on June 26, 2026, with investors rotating into defensive and interest-rate-sensitive sectors while reducing exposure to technology and industrial shares. Health Care emerged as the clear market leader, while Real Estate and consumer-related sectors also attracted buying interest.

The session reflected a shift toward sectors offering earnings stability and valuation support, as investors became more selective following the strong advances seen in growth-oriented industries during recent weeks.

Daily US Sector Performance Summary

Key Market Themes

Health Care Takes Control

- Health Care (XLV) surged 3.03%, making it the strongest-performing sector of the session. Investors continued to favour companies offering stable earnings growth and defensive characteristics amid evolving market conditions. The sector's strong advance suggests growing demand for quality businesses capable of delivering reliable financial performance regardless of broader economic fluctuations.

Real Estate and Consumer Sectors Attract Capital

- Real Estate (XLRE) gained 1.46%, while Consumer Staples (XLP) and Consumer Discretionary (XLY) rose 0.92% and 0.90%, respectively. Strength in these sectors indicates increasing investor confidence in domestic economic resilience and the prospect of a more supportive interest-rate environment. Together, these gains reflect balanced positioning between defensive stability and consumer-driven growth opportunities.

Defensive Sectors Continue to Perform

- Utilities (XLU) and Communication Services (XLC) posted gains of 0.76% and 0.57%, respectively. Investors continued allocating capital toward sectors offering predictable earnings and stable cash-flow characteristics. The positive performance of these traditionally defensive sectors reinforces the market's preference for quality and earnings visibility.

Technology Faces Profit-Taking

- Information Technology (XLK) declined 1.87%, making it the weakest-performing sector of the trading session. The decline likely reflected profit-taking following a strong run in large-cap technology shares. While the sector's long-term fundamentals remain constructive, investors appeared willing to rotate capital toward areas offering more attractive near-term valuations.

Industrials and Commodity Sectors Weaken

- Industrials (XLI) fell 1.59%, while Energy (XLE) and Materials (XLB) both slipped 0.46%. The weakness suggests investors reduced exposure to cyclical and commodity-sensitive industries amid uncertainty surrounding future economic growth and commodity demand. Although the declines were relatively modest outside Industrials, sector performance indicates a preference for defensive positioning.

Bottom Line

The June 26 trading session highlighted a clear rotation toward defensive and interest-rate-sensitive sectors. Health Care, Real Estate, Consumer Staples, and Utilities led gains, while Technology and Industrials experienced notable selling pressure.

If investors continue favouring sectors with stable earnings and defensive characteristics, Health Care and Real Estate may remain key market leaders. Meanwhile, weakness in Technology and Industrials suggests sector rotation rather than a broad deterioration in overall market sentiment.

_06_27_2026_21_16_35_168117.jpg)

Please wait processing your request...

Please wait processing your request...