Can Business owners use a Solo 401(k) for more retirement control? Learn about Investment flexibility, contribution limits, Roth Options, and compliance rules.

Key Highlights

- Solo 401(k) plans offer business owners greater control over retirement contributions, investments, and plan features.

- Self-directed structures may allow alternative Assets such as real estate and private investments.

- Higher flexibility comes with greater compliance, recordkeeping, and administrative responsibilities.

For self-employed professionals and owner-only businesses, Retirement Planning is often about more than tax deductions. Many entrepreneurs want greater control over how retirement assets are invested and managed.

That is one reason Solo 401(k) plans have become increasingly popular. Compared with many traditional workplace retirement plans, Solo 401(k)s can provide substantial flexibility over contributions, investment choices, and long-term retirement strategy.

Why Solo 401(k)s Appeal to Business Owners

Unlike traditional employer-sponsored retirement plans, a Solo 401(k) is designed specifically for businesses with no employees other than the owner and, if applicable, a spouse.

Because the business owner typically serves as both employer and participant, they gain greater influence over plan design and investment decisions.

This flexibility allows entrepreneurs to tailor retirement savings strategies to match business income, tax planning objectives, and investment preferences.

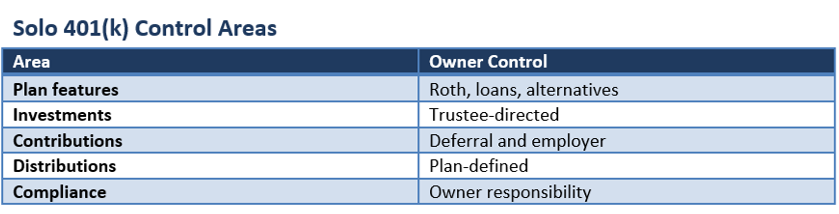

Greater Control Over Plan Features

One of the defining advantages of a Solo 401(k) is customization.

Depending on the provider and plan document, business owners may be able to include features such as Roth contributions, participant loans, rollover provisions, and after-tax contribution options.

These choices are not automatically available in every plan. The governing documents must specifically authorize each feature.

As a result, selecting the right provider can be just as important as selecting the right investments.

Investment Flexibility Can Extend Beyond Traditional Assets

Many standard retirement plans limit participants to a predefined menu of mutual funds and Exchange-traded funds.

Some Solo 401(k) structures allow broader investment authority, including exposure to real estate, private lending, Private Equity, and other alternative assets.

This level of flexibility attracts business owners who prefer direct involvement in portfolio decisions.

However, broader investment freedom does not eliminate IRS restrictions. Prohibited transaction rules continue to apply regardless of the asset being purchased.

Higher Contribution Capacity Supports Long-term Growth

Another major benefit is contribution capacity.

For 2026, eligible participants can contribute up to $24,500 through employee salary deferrals. Combined employer and employee contributions may reach $72,000, with additional catch-up contributions available for eligible individuals.

This often allows significantly larger retirement contributions than many alternative retirement account structures.

For high-income entrepreneurs, the ability to contribute more can have a meaningful impact on long-term Wealth accumulation.

Administrative Responsibilities Increase with Control

Greater flexibility comes with added obligations.

Business owners must maintain plan records, monitor contribution limits, and ensure ongoing compliance with IRS regulations. Once plan assets exceed $250,000, Form 5500-EZ filing requirements generally apply.

Plan documents may also require updates when retirement legislation or regulatory guidance changes.

For some business owners, these administrative responsibilities represent a reasonable trade-off for increased control.

Solo 401(k) vs SEP IRA

While SEP IRAs remain popular among self-employed individuals, Solo 401(k)s often provide more flexibility.

Solo 401(k)s can offer Roth contribution options, participant Loan provisions, and potentially larger contributions at certain income levels. SEP IRAs generally provide simpler administration but fewer customization opportunities.

The appropriate choice depends on income, business structure, and retirement objectives.

Conclusion

A Solo 401(k) can provide business owners with a powerful combination of retirement savings capacity, investment flexibility, and plan customization. The ability to direct investments, incorporate Roth features, and potentially access alternative assets makes the structure appealing for entrepreneurs seeking greater control over retirement planning. Yet that flexibility also creates additional compliance and recordkeeping obligations. For many self-employed individuals, working with retirement plan specialists and tax professionals can help ensure the benefits of a Solo 401(k) are fully realized while maintaining regulatory compliance.

Please wait processing your request...

Please wait processing your request...