Can you self-direct a SEP IRA? Learn how self-directed SEP IRAs work, contribution limits, alternative investments, IRS rules, and compliance risks.

Key Highlights

- Self-directed SEP IRAs combine higher contribution limits with broader Investment flexibility.

- Alternative Assets such as real estate, Private Equity, and private lending may be permitted through specialized custodians.

- IRS prohibited transaction rules, valuation requirements, and compliance obligations remain critical considerations.

Many small Business owners and self-employed professionals seek greater control over how their retirement savings are invested. While SEP IRAs are often associated with traditional brokerage investments, they can also be structured as self-directed accounts that provide access to a much broader range of assets.

For investors looking to combine substantial contribution capacity with alternative investment opportunities, a self-directed SEP IRA may offer an attractive solution.

What Is a Self-Directed SEP IRA?

A SEP IRA is an employer-sponsored retirement plan commonly used by small businesses, sole proprietors, and self-employed individuals.

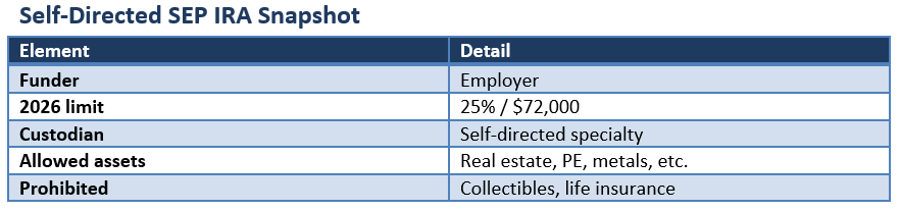

A self-directed SEP IRA follows the same tax and contribution rules as a standard SEP IRA but is held with a specialized Custodian that permits alternative investments beyond conventional stocks, bonds, and mutual funds.

The tax treatment remains unchanged. What differs is the investment flexibility available to the account holder.

Higher Contribution Limits Remain a Key Advantage

One reason SEP IRAs remain popular is their generous contribution capacity.

For 2026, employer contributions can generally reach up to 25% of eligible compensation, subject to a maximum annual contribution of $72,000.

Compared with traditional and Roth IRAs, which have significantly lower annual contribution limits, a SEP IRA can allow business owners to accumulate retirement assets more rapidly during high-income years.

Alternative Investments Expand Portfolio Choices

A self-directed SEP IRA may provide access to investment opportunities unavailable through traditional retirement accounts.

Depending on the custodian, permitted assets may include:

- Real estate

- Private equity investments

- Private lending and promissory notes

- Certain precious metals

- Limited Partnership interests

- Select private placements

This flexibility can appeal to investors seeking broader Diversification or exposure to assets they understand through their professional experience.

IRS Rules Still Apply

Greater investment control does not mean fewer regulations.

Self-directed SEP IRAs remain subject to the same prohibited transaction rules that govern other IRAs. Transactions involving disqualified persons, self-dealing, or personal use of IRA-owned assets can result in significant tax consequences.

For example, using retirement-owned real estate personally or engaging in transactions with certain family members may violate IRS regulations.

Understanding these restrictions is essential before investing in alternative assets.

Valuation and Recordkeeping Matter

Many alternative investments lack publicly quoted market prices.

As a result, annual fair market valuations are often necessary to support custodial reporting requirements. Accurate valuations become particularly important when calculating distributions, transfers, or account balances.

Investors should also expect additional administrative costs compared with traditional brokerage IRAs.

Risks Investors Should Consider

Alternative assets can offer diversification benefits, but they also introduce unique risks.

Illiquidity, valuation uncertainty, higher fees, Fraud exposure, and compliance mistakes can all affect retirement outcomes. Investments that appear attractive from a business perspective may create unexpected tax or regulatory complications inside a retirement account.

Thorough Due Diligence is critical before committing retirement assets to non-traditional investments.

Conclusion

A self-directed SEP IRA can provide business owners with a powerful combination of higher contribution limits and broader investment flexibility. The ability to invest in real estate, private equity, and other alternative assets may appeal to investors seeking greater retirement portfolio control. However, the added flexibility comes with increased responsibility for compliance, valuation, and recordkeeping. Before establishing a self-directed SEP IRA, investors should carefully evaluate both the opportunities and the regulatory obligations involved.

Please wait processing your request...

Please wait processing your request...