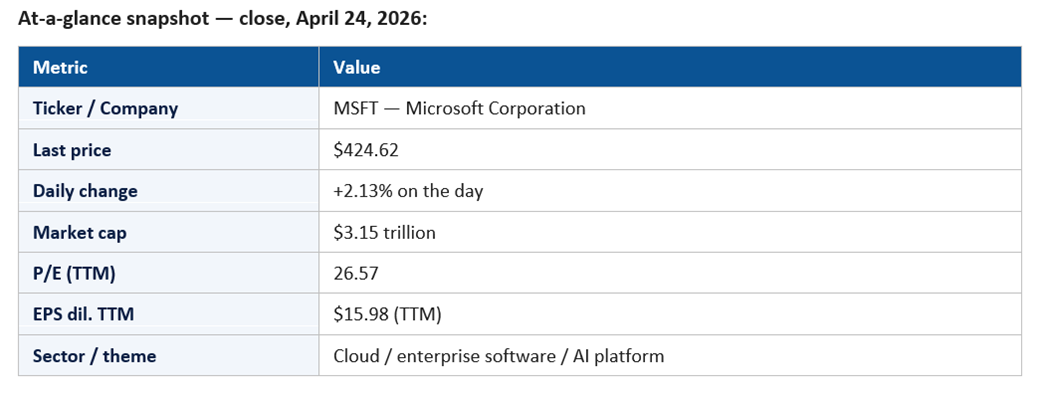

Microsoft (NASDAQ:MSFT) closes at $424.62, $3.15T market cap, P/E 26.57. Microsoft's Azure AI, Copilot & OpenAI edge make it 2026's most undervalued megacap. Deep-dive.

Key Highlights

- At 26.57x P/E, Microsoft is the cheapest megacap AI stock — cheaper than NVIDIA, Apple, and every peer with comparable AI exposure.

- Azure + Copilot + OpenAI form a three-layer AI toll road quietly compounding inside every Fortune 1000 IT budget.

- A +2.13% gain on a chip-led tape confirms MSFT's rare dual role: AI upside on good days, defensive anchor on bad ones.

Microsoft (NASDAQ:MSFT) is the most diversified large-cap AI franchise in the public market. Its commercial cloud — Azure, Microsoft 365, Dynamics 365, Power Platform, GitHub, and the AI services that span all of them — is the operating system of modern enterprise computing. Its Windows, Surface, and gaming franchises are global consumer footholds. Its LinkedIn, advertising, and search businesses sit on top of one of the world's largest first-party data graphs. And underneath it all is one of the most strategic equity stakes in the AI era — its multibillion-dollar relationship with OpenAI.

By 2026, the Microsoft narrative has matured. The company is no longer defending the cloud from AWS or chasing Google in productivity. It is the AI distribution layer for every Fortune 1000 procurement cycle, and that posture is showing up in revenue mix, in gross margin, and increasingly in the multiple.

Stock Performance in 2026 (YTD)

MSFT closed April 24, 2026 at $424.62, up 2.13% in a session that saw the broader market add 0.80% and a chip-led tape force a rotation across megacaps. With a market capitalization of $3.15 trillion and a trailing P/E of 26.57 on $15.98 of TTM diluted earnings, Microsoft trades at a multiple noticeably more reasonable than its peer group — the price of being the boring, durable AI play in a market that wants spectacle.

The implied YTD posture is one of relative leadership without volatility. Microsoft has functioned as the safety blanket of the AI trade — when the chip names crash, MSFT softens the blow; when sentiment turns positive on enterprise spending, MSFT participates almost mechanically through its commercial cloud guidance.

It is hard to overstate how unusual it is for the third-largest U.S. company by market cap to also be one of the cheapest, on a P/E basis, of the megacap AI cohort. That gap is the central tension in the 2026 setup.

Key Price Movements and Milestones

Three milestones define the tape so far. First, the steady defense of the $400-plus price band, which has functioned as a structural floor on dips. Second, Microsoft's relative outperformance on days when AI capex narratives turn positive without going parabolic — the +2.13% session is a textbook example of this regime. Third, the relationship between MSFT and the chip complex has proven more constructive than competitive: when AMD or Intel rally on AI capex, Microsoft's Azure narrative gets re-rated alongside, not against, them.

The April 24 print sits inside a broader 2026 narrative of compounding rather than catalyst-driven jumps. Microsoft tends to move in defensible 1–3% increments rather than in 10% gaps, and that is exactly the price profile risk-aware allocators want from a top-three holding.

Major Catalysts: Why the Stock Moved

Three catalysts dominate the 2026 narrative. The first is Azure AI workload monetization. Each quarter that Azure prints accelerating cloud growth attributable to AI services validates the multi-year narrative that AI inference and training revenue is real, large, and durable. Investors do not need 50% growth; they need clear evidence that AI is a measurable contributor to the cloud line.

The second is Copilot monetization across the Microsoft 365 install base. The pricing thesis — that AI features command a premium per-user subscription on top of an already entrenched productivity base — has gone from speculative to demonstrable, and 2026 is the year management has had to translate that adoption story into hard ARR contribution.

The third is the OpenAI relationship. Microsoft's preferred-partner status with OpenAI gives it both an AI-product distribution advantage and an investor-narrative advantage that is hard to replicate. Every commercial milestone OpenAI hits — enterprise revenue, API usage, agent adoption — feeds back into Microsoft's investment story.

Macro and Fed-rate sensitivity is muted. Microsoft is duration-sensitive in theory, but its commercial cloud has the kind of revenue visibility that lets analysts model through rate scenarios. Geopolitics matter mostly through cloud-region build-out and through cybersecurity demand, both of which have been net positive for the franchise.

Sector Trends Influencing the Stock

Three structural trends underwrite the 2026 thesis. First, enterprise AI is moving from pilots to production. The CIO conversation in 2026 is not whether to use AI but which platform vendor to standardize on, and Microsoft is the default option for an enormous share of the Fortune 2000.

Second, the convergence of cybersecurity, identity, and AI is concentrating spend in a small number of platform vendors, and Microsoft is the most credible single-vendor offering in that bundle. Defender, Entra, Sentinel, and Purview have collectively grown into a security business that few competitors can match in scope.

Third, the gaming franchise post-Activision integration is no longer a quarter-to-quarter swing factor; it is a structural margin-positive engine for the more-personal-computing segment. That removes a previous source of volatility from the consolidated narrative.

Competitive Positioning

Microsoft's competitive position in 2026 is best described as platform-incumbent with AI optionality. Against AWS, the share gap has narrowed materially over the AI cycle. Against Google Cloud, Microsoft retains a structural advantage in enterprise distribution. Against the AI-native upstarts, Microsoft's bundle and procurement footprint give it a sales motion that is nearly impossible to displace.

Where competitive pressure is real is at the model layer. OpenAI is one capable lab among several — Anthropic, Google DeepMind, Meta's Llama family, and a handful of well-funded independents are credible alternatives. Microsoft has hedged by integrating multiple model providers into its enterprise products, but the OpenAI alignment remains the defining narrative.

The sleeper competitive asset is GitHub. As AI moves from chat interfaces into code generation and software automation, GitHub becomes a strategic chokepoint that few competitors can replicate. Copilot in code is a more durable product than Copilot in chat, and the market has only begun to price that asymmetry.

Financial Highlights

TTM diluted EPS of $15.98 on a $424.62 share price is the heart of the bullish setup. A P/E of 26.57 on a business with Microsoft's growth profile, gross margin trajectory, and revenue durability is, by historical megacap standards, a reasonable price for an exceptional asset.

Operating margin discipline is the under-appreciated story. Even as capex has scaled enormously to support AI infrastructure, Microsoft has held operating margins at industry-leading levels. The implied capital-efficiency message is that Microsoft is investing through the cycle without sacrificing the structural profitability that funds the dividend, the buyback, and the ongoing strategic optionality.

Capital return continues to be a steady but secondary part of the equity story. The buyback supports the float; the dividend signals durability. Neither is the primary reason to own MSFT, but together they reinforce the perception that this is a compounder that pays you to wait.

Key Risks and Challenges

The first risk is AI capex digestion. Microsoft is one of the largest buyers of AI infrastructure in the world, and any sign that capex efficiency is deteriorating could compress operating margin even before revenue weakens. The second risk is regulatory: Microsoft's footprint in cloud, productivity, gaming, and AI is now broad enough that antitrust scrutiny — particularly in Europe — is a structural feature rather than a one-off concern.

The third risk is the OpenAI-relationship narrative. Any disruption to the partnership, real or perceived, would create immediate stock volatility even if the underlying commercial impact were modest. Investors should expect periodic noise on this front and price it accordingly.

The fourth, quieter risk is enterprise IT-budget slowing. Microsoft's revenue base is closely tied to corporate IT spending, and a sustained slowdown there would test the resilience of the cloud-and-AI growth narrative.

Institutional and Investor Sentiment

Microsoft is, alongside NVIDIA, the most-owned name in 2026 institutional portfolios. It is a structural overweight in growth, core, and even some value mandates because of the unusual combination of revenue durability and AI exposure. Sell-side coverage is deeply constructive, with the bear case typically focused on multiple compression rather than business deterioration.

The options market reflects the calm: implied volatility into earnings has been muted, skew on downside puts sits at moderate levels, and there is a healthy amount of upside-call activity that signals expectation of further outperformance without euphoria.

Signals to Watch in the Coming Quarters

Five concrete signals will define how the Microsoft narrative evolves through the rest of 2026. The first is the Azure growth rate net of foreign-exchange and any reported AI-services contribution. Investors are no longer satisfied with a single consolidated cloud number; the question is how much of the growth is AI-attributable, how much is durable, and how the AI piece is trending sequentially. Each quarterly print that delineates these components will move the stock more than the headline.

The second signal is Copilot per-seat economics. The market wants visible evidence that the Copilot premium is not just an attach event but a sustained subscription with low churn and rising functionality. Enterprise renewal rates for Copilot-bearing seats and any disclosure of average revenue per AI seat will be among the most-watched data points in management commentary.

The third signal is capex efficiency. Microsoft spends among the largest absolute dollar capex of any company on the planet, and the implied return on that investment — measured by the gross profit dollars produced per dollar of cloud capex — is the swing variable for operating margin in 2026 and 2027. Any commentary that clarifies the depreciation roadmap or the useful-life assumptions on AI infrastructure will be material.

The fourth signal is gaming. Activision integration, content-pipeline strength, and Game Pass subscriber growth collectively determine whether More Personal Computing operates as a stable margin contributor or as a swing factor. The pattern in 2026 has been the former; the question is whether that holds through the holiday cycle.

The fifth signal is the OpenAI relationship structure. Periodic narrative updates on commercial terms, capacity allocation, governance, and any structural evolution of the partnership will continue to be a recurring source of stock volatility. Investors should expect this to remain a live topic and price it accordingly rather than treating each update as a surprise.

Outlook for the Rest of 2026

The base case is continuation: Azure prints high-teens to low-20s growth with AI as a clear contributor; Copilot ARR climbs to a level that materially moves the productivity-and-business-processes line; GitHub becomes an increasingly important narrative chapter; and capex moderates as AI infrastructure efficiency improves. In that scenario, the market gets comfortable paying 28–30x for Microsoft, and the stock grinds toward $475–$500 by year-end without doing anything dramatic.

The bear case is a combination of margin compression from capex and a slowdown in the cloud-attach to AI workloads. Either alone is manageable; both together would be the kind of multi-quarter pause that compresses the multiple back to the low 20s.

Microsoft in 2026 is the rare AI investment that does not require you to believe in spectacle. It just requires you to believe enterprises will keep paying for productivity. They will.

For now, the +2.13% session on a chip-led tape is exactly the trade investors keep paying for: AI exposure with adult supervision. Until that combination breaks, MSFT remains the easiest core position in the index.

_06_11_2026_22_43_52_812084.jpg)

Please wait processing your request...

Please wait processing your request...