_04_27_2026_07_50_29_460180.jpg)

Micron (NASDAQ:MU) stock reflects AI-driven valuation shift as HBM demand, DRAM pricing, and capex cycles reshape earnings visibility and risk outlook.

Key Highlights

- Micron’s valuation reflects a structural shift from cyclical memory to AI-driven earnings visibility.

- HBM demand has reshaped pricing power and capital allocation across the DRAM market.

- Elevated capex and memory-cycle risks remain central to forward earnings volatility.

Micron Technology (NASDAQ:MU) is one of three remaining major DRAM producers globally and a top-tier NAND flash producer. Its product portfolio spans high-bandwidth memory (HBM) for AI accelerators, server DRAM, mobile and client DRAM, automotive and industrial memory, and SSD products that range from consumer to data-center class. Headquartered in the United States and operating fabs across the U.S., Asia, and recently expanding domestic manufacturing capacity, Micron is the strategic Western counterweight to the Korean DRAM duopoly of Samsung and SK Hynix.

By 2026, the equity story has been reshaped by the AI memory cycle. HBM has gone from a niche, low-volume specialty product to one of the most strategically important categories in the entire semiconductor industry, with each AI accelerator shipping with substantial HBM content. That shift has changed the unit economics, pricing power, and capital intensity of the memory business in ways that the long-cycle memory bears underestimated for years.

Stock Performance in 2026 (YTD)

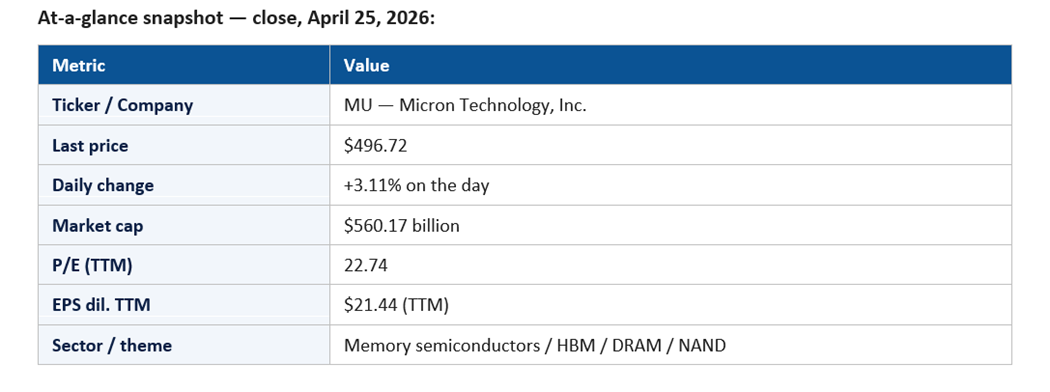

MU closed April 25, 2026 at $496.72, up 3.11% on the day, with a market capitalization of $560.17 billion. The trailing P/E of 22.74 on $21.44 of TTM diluted EPS reflects a fully repriced cyclical that the market has come to view as part of the AI-infrastructure thesis rather than a pure boom-bust commodity stock.

The implied YTD posture is one of constructive participation in the AI-capex narrative, with each set of HBM-related disclosures, hyperscaler order signals, and quarterly earnings prints supporting the multiple. The +3.11% session sits inside a regime in which Micron consistently participates in chip-led rallies and trades on its own as well as on broader sector momentum.

Key Price Movements and Milestones

Three milestones define the 2026 tape. First, the persistent move into and beyond the $400 zone, with the stock having effectively re-rated through what was previously seen as a multi-cycle resistance band. Second, the relationship between MU and the broader AI complex has tightened: Micron has become a near-mandatory expression for any portfolio that wants memory exposure to AI without the volatility of pure-play accelerators.

Third, the disclosure cadence around HBM3E and successor product timelines, qualification at major accelerator customers, and capacity ramp has been the most-watched part of each earnings cycle, with each milestone shifting the trajectory of consensus revenue and EPS estimates.

Major Catalysts: Why the Stock Moved

The dominant 2026 catalyst is HBM. Each step in HBM3E maturity, each qualification at a major AI accelerator customer, and each disclosure on capacity allocation has been a discrete catalyst. The structural fact is that HBM's pricing power and capital intensity have shifted DRAM economics meaningfully higher than prior cycles.

The second catalyst is server DRAM. Even excluding HBM, the broader server DRAM environment has been constructive in 2026, with hyperscaler buildouts driving steady demand for high-density, high-performance DRAM modules.

The third catalyst is NAND. While NAND remains structurally lower-margin than DRAM, data-center QLC SSDs and high-density consumer products have provided incremental support. NAND is no longer the drag on the consolidated story it has historically been.

The fourth catalyst is U.S. manufacturing investment. Micron's domestic capacity expansion, supported by CHIPS Act funding, has positioned the company as the principal American DRAM operator at a time when supply-chain resilience is a strategic priority for hyperscalers and government customers.

Macro and Fed-rate sensitivity is meaningful — Micron is a high-beta cyclical with structural improvement. Geopolitics matter through export controls, China-related demand restrictions, and broader supply-chain dynamics in Asia.

Sector Trends Influencing the Stock

Three sector trends underwrite Micron's 2026 thesis. First, the memory cycle has structurally improved due to disciplined supply growth, consolidation among DRAM producers, and the unique characteristics of HBM as a higher-value, longer-life-cycle product. Second, AI infrastructure spending has produced a demand backdrop that is materially different in scale and durability from previous cycles.

Third, the domestic-manufacturing trend in the U.S. has positioned Micron favorably for both customer preference and government policy support. Each step toward domestic fab activation reinforces the strategic-value narrative.

Competitive Positioning

Micron's competitive position in 2026 is one of structurally improved pricing power and operational discipline. The DRAM market is effectively a three-player industry — Samsung, SK Hynix, Micron — and the rationality of supply growth across the cohort has been a defining feature of the recent cycle. In HBM specifically, all three players are participating, but with differentiated qualification and capacity profiles.

Micron's strategic edge is twofold. First, its operational track record on technology transitions has been competitive with Korean peers across recent generations. Second, its U.S. domicile and domestic manufacturing investment provide a structural advantage in customer relationships where supply-chain considerations matter.

In NAND, the competitive set is broader and the economics are tougher, but Micron has continued to deliver competitive product roadmaps and to manage the segment for cash flow rather than purely for share.

Financial Highlights

TTM diluted EPS of $21.18 on a $496.72 share price gives Micron a P/E of 23.45. That multiple is a striking signal that the market has fundamentally repriced memory as a more durable earnings stream than prior cycles suggested.

Gross margin has expanded materially as the HBM mix has grown and as DRAM pricing has remained constructive. Operating expenses have been managed with discipline; capex remains substantial as HBM capacity expansion proceeds, but the implied capital efficiency on incremental HBM bits is favorable.

Free cash flow has scaled meaningfully across the cycle, providing the funding base for continued capacity expansion and a measured capital return program. The balance sheet has been managed conservatively, providing flexibility through commodity-cycle volatility.

Key Risks and Challenges

The first risk is the memory cycle. Despite structural improvements, memory remains cyclical, and any meaningful softening in DRAM ASPs would compress earnings quickly.

The second risk is HBM competition. Samsung and SK Hynix are both formidable HBM operators, and any meaningful share loss to those competitors at major AI accelerator customers would dent the bull case.

The third risk is China exposure. Chinese demand and competitive dynamics, plus the regulatory framework around U.S. export controls, are recurring narrative variables that affect both addressable market and pricing.

The fourth risk is execution. HBM capacity expansion, technology transitions to next-generation HBM standards, and customer qualifications all carry execution risk.

Why Micron Is the Memory Cycle Investors Stopped Calling a Cycle

For thirty years, the universal explanation for memory underperformance has been the same: it is a commodity, the cycle is brutal, and the only way to make money is to time it. The 2026 narrative has rewritten that script. HBM is not a commodity in the historical sense. It is a specialty product with multi-quarter qualification cycles, customer-specific design integration, and pricing power that more closely resembles advanced logic than legacy DRAM. That structural change is what has allowed Micron to trade at a multiple memory companies almost never sustain.

What makes MU specifically advantaged is the combination of operational track record, U.S. domicile, and customer relationships. Micron's domestic manufacturing footprint, supported by CHIPS Act funding, is a strategic asset at a moment when hyperscalers and government customers are explicitly valuing supply-chain resilience. Combine that with HBM3E qualifications at the major AI accelerator customers, and Micron has positioned itself as the Western counterweight to the Korean DRAM duopoly precisely as that positioning has become a strategic, not just commercial, consideration.

The result is an equity that has earned its re-rating through repeated demonstration of the new economics. Each quarter that HBM revenue grows, each AI accelerator design that Micron qualifies into, each domestic capacity milestone — these are not catalysts for a cyclical bounce. They are evidence that the earnings power of the franchise has structurally shifted to a higher level than the historical model assumed. The market has begun to price that shift, and the next several quarters will determine how much further the re-rating runs.

Institutional and Investor Sentiment

Institutional positioning in Micron in 2026 is generally constructive, with the stock featured in many AI-thematic and tech-sector mandates. Sell-side coverage has shifted decisively positive over the past 12–18 months, with the bull case anchored to HBM and the broader AI-memory thesis.

The options market reflects elevated but moderating implied volatility, consistent with a stock that has graduated from speculative momentum to a more institutional ownership profile.

Signals to Watch in the Coming Quarters

Six concrete signals will define how the Micron narrative evolves through the rest of 2026. The first is HBM revenue and bit-share commentary. Each quarter the market wants visible evidence that HBM revenue is scaling and that Micron's bit-share with major AI accelerator customers is consistent with the bull-case trajectory.

The second signal is DRAM ASP dynamics. Server DRAM, mobile DRAM, and PC DRAM pricing collectively define the broader memory cycle outside HBM. The market wants stability or modest improvement; any meaningful ASP weakening would compress consolidated earnings quickly.

The third signal is NAND profitability. NAND has historically been a drag on consolidated economics; the 2026 narrative has improved, with QLC data-center SSDs and high-density consumer products providing support. Any disclosed gross margin trajectory in NAND will be parsed for sustainability.

The fourth signal is U.S. manufacturing milestones. CHIPS Act-supported domestic capacity expansion remains a strategic priority, and each construction milestone, equipment install, and fab activation event reinforces the strategic-value narrative.

The fifth signal is HBM next-generation product progression. Each step toward HBM4 qualification, power-efficiency improvement, and capacity-density advancement determines whether Micron maintains competitive parity with Samsung and SK Hynix in the most strategically important DRAM category.

The sixth signal is capex commentary. Memory capex has historically been the swing variable for the cycle. The market wants disciplined commentary that ties capex expansion to contracted demand rather than speculative supply growth, which is the pattern that has supported the 2026 multiple.

Outlook for the Rest of 2026

The base case is continuation: HBM demand remains tight; DRAM pricing holds firm; NAND remains modestly profitable; capex expansion is funded by operating cash flow without straining the balance sheet. In that scenario, EPS continues to grow and the multiple defends itself on a combination of fundamentals and AI-narrative support.

The bull case is a step-change in HBM-related order visibility — for example, a multi-year supply commitment from a major hyperscaler or AI accelerator producer — that materially raises forward EPS estimates. The bear case is a meaningful softening of DRAM pricing combined with execution issues on HBM ramp.

Micron in 2026 has done something memory companies almost never do: convert a commodity business into a strategic asset. As long as the AI build-out continues, that conversion holds.

For now, the +3.11% session is the kind of measured participation that has framed the year. Memory is no longer the AI trade's hidden ingredient. It is the trade investors increasingly want to own outright.

_06_11_2026_22_43_52_812084.jpg)

Please wait processing your request...

Please wait processing your request...