An equity research deep-dive on Meta Platforms (META), anchored on the April 24, 2026 close. Meta (NASDAQ: META) stock reflects AI-driven ad growth as strong earnings, rising ROI, and disciplined capex support valuation and long-term growth outlook.

Key Highlights

- Meta’s valuation reflects AI-driven advertising efficiency with strong earnings visibility and disciplined capital allocation.

- AI-led targeting and creative tools are materially improving advertiser ROI and revenue growth.

- Balanced capex and strong free cash flow support sustained investment in AI and Reality Labs.

Meta Platforms is the dominant operator of consumer social and messaging surfaces — Facebook, Instagram, WhatsApp, Messenger, Threads — bolted to one of the most efficient advertising machines ever built and a long-term investment program in mixed reality (Reality Labs) and frontier AI (the Llama family of open-weight models). With roughly four billion people using one or more of its apps each month, Meta is the closest thing in technology to a global attention utility.

By 2026, the strategic frame has tightened. Meta is best understood as an AI-native advertising company that happens to operate the world's largest social network, with a side business in open-source model development and a long-duration option on next-generation computing platforms. The capex story that scared investors in prior years has matured into a deliberate, well-explained investment program. The Reality Labs losses are still significant but no longer existentially alarming. And the core ads business — by far the cleanest and most leveraged piece of the consolidated story — is increasingly being shaped by AI-driven targeting, ranking, and creative tooling that has measurably lifted advertiser ROI.

Stock Performance in 2026 (YTD)

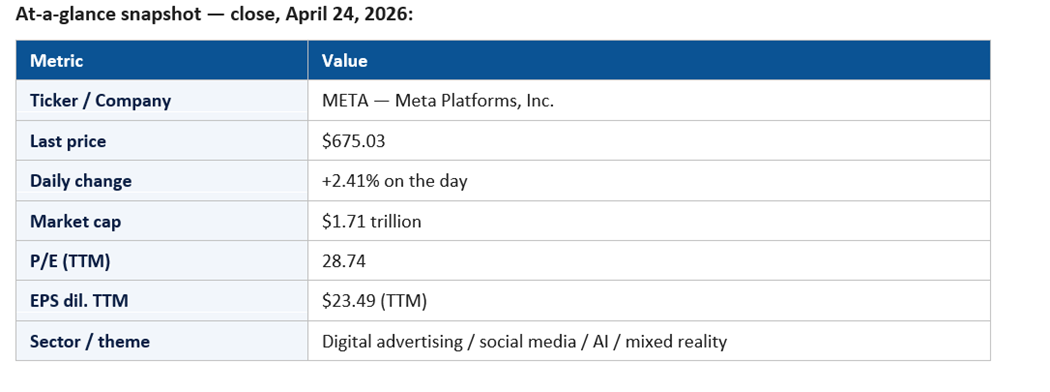

META closed April 24, 2026 at $675.03, up 2.41% on the day, with a market capitalization of $1.71 trillion. With a P/E of 28.74 on $23.49 of TTM diluted earnings, Meta carries the most striking earnings power per dollar of price among the megacap AI cohort — and one of the most reasonable multiples relative to that earnings power.

The implied YTD trajectory has been one of measured re-rating. The stock has participated in AI-led market rallies without becoming a speculative chip-proxy, and it has held up on macro-nervous days because of the underlying durability of advertising revenue. The +2.41% session sits inside a regime where Meta is treated as both an AI beneficiary and an earnings compounder.

The market-cap math tells its own story: $1.71T on $23.49 of TTM EPS implies one of the most defensible price-to-earnings frameworks in big tech. That valuation foundation is what gives portfolio managers the confidence to add to the name on weakness.

Key Price Movements and Milestones

Three milestones define the 2026 tape. First, the consolidation through and beyond the $650 zone, which had functioned as a multi-quarter resistance level. Second, the persistent narrowing of the spread between Meta's multiple and the rest of the megacap AI cohort: META has been re-rated upward as investors increasingly see it as an AI infrastructure beneficiary, not just an advertising name.

Third, the disclosure cycle around AI-driven ad performance has matured. Each quarter that management can point to measurable, AI-attributable lifts in advertiser ROI has reinforced the multiple. Meanwhile, Reality Labs disclosure has shifted from purely defensive (about losses) to constructive (about hardware progress and software ecosystem growth).

Major Catalysts: Why the Stock Moved

The dominant 2026 catalyst is AI-driven ad efficiency. Each step-change improvement in Meta's recommendation, targeting, and creative-generation systems shows up almost mechanically in advertiser performance metrics, which translates into advertiser budget reallocation toward Meta. Investors have increasingly treated this loop as the core thesis: AI is the operating system of the advertising business.

The second catalyst is Reels and short-form monetization. The closing of the monetization gap between short-form and feed has been one of the most important commercial transitions in social media, and Meta is on the productive side of it. Each quarter of expanding short-form ad revenue strengthens the consolidated growth narrative.

The third catalyst is Llama and the open-weight strategy. Meta's commitment to open-weight frontier models is increasingly viewed as both a strategic moat — anchoring developer mindshare and ecosystem leverage — and a cost-management tool. Investors have come to see open-weight Llama models as a way to lower Meta's own AI infrastructure cost over time, not as a giveaway.

The fourth catalyst is messaging monetization, particularly through business messaging and click-to-message ads. WhatsApp's monetization curve, after years of deliberate slowness, has begun to inflect.

Macro and Fed-rate sensitivity is moderate; geopolitics matter mostly through the regulatory environment in Europe and through the U.S.-China advertiser dynamic.

Sector Trends Influencing the Stock

Three sector trends underwrite Meta's 2026 thesis. First, the digital advertising market has stabilized after several years of structural transition. Privacy changes and signal loss have become manageable; Meta has reconstructed its measurement and targeting infrastructure to run on first-party signals augmented by AI inference.

Second, AI-generated and AI-assisted creative is moving from edge case to default. Advertisers increasingly delegate creative production to Meta's tools, which both improves advertiser ROI and deepens platform lock-in. Each cycle of creative-tooling improvement compounds the platform's strategic position.

Third, mixed-reality hardware adoption is finally reaching a level at which the developer ecosystem and content library can begin to support a self-reinforcing growth loop. Reality Labs is still loss-making, but the strategic optionality has gotten more credible.

Competitive Positioning

Meta's competitive position in 2026 is unusually strong. In digital advertising, the duopoly with Alphabet remains intact, with Amazon's retail-media expansion the most visible third entrant. In short-form video, Meta has competed credibly with TikTok at the platform level and has, in many advertiser conversations, become the higher-ROI option.

In AI, Meta's open-weight Llama strategy has built ecosystem leverage that closed-weight competitors cannot easily replicate. Developers, enterprises, and academic users continue to gravitate to Llama as the default open-weight option, which strengthens Meta's downstream commercial position even when the immediate revenue impact is indirect.

In mixed reality, Meta is the dominant first-party hardware operator, with Apple's Vision line as the premium-tier competitor. The competitive dynamic in MR remains early, but Meta's installed base advantage is meaningful.

Financial Highlights

TTM diluted EPS of $23.49 against a $675.03 share price gives Meta a P/E of 28.74. That is the financial heart of the bull case: an AI-leveraged growth story trading at a multiple lower than several lower-quality peers.

Operating margin discipline is central. Even with elevated AI infrastructure capex and continued Reality Labs investment, Meta has held consolidated operating margins at industry-leading levels in the family-of-apps segment. The capital return program has been increased meaningfully across the cycle, with a significant buyback and a now-recurring dividend.

Free cash flow generation has accelerated as the AI capex cycle has matured and as ad revenue has compounded. The ability to fund both Reality Labs and AI infrastructure out of operating cash flow is one of the quietly impressive features of the financial profile.

Key Risks and Challenges

The first risk is regulatory. Europe in particular has been a structural source of pressure on Meta's data practices and ad-targeting tools, and any tightening of the Digital Services Act or Digital Markets Act regimes could meaningfully affect ad monetization. The U.S. environment, while less aggressive, is not benign.

The second risk is platform-level signal. Meta's revenue growth ultimately depends on user attention and advertiser ROI, both of which require continued product excellence. A misstep — algorithmic or strategic — could compress growth meaningfully.

The third risk is Reality Labs. The losses are real, persistent, and dilutive to consolidated margin. Investors have come to tolerate them as the cost of strategic optionality, but a sustained miss on hardware adoption milestones could re-introduce the bear case that capital is being misallocated.

The fourth risk is capex digestion. AI infrastructure has become a substantial line item, and any deceleration in the AI-attributable ad-revenue lift could create a margin air pocket.

Institutional and Investor Sentiment

Institutional positioning in Meta in 2026 has shifted to overweight-and-comfortable. The combination of AI-driven ad efficiency, disciplined capital return, and a still-reasonable multiple has made META a near-consensus core position. Sell-side coverage is broadly constructive, with bear cases largely focused on regulatory tail risk and Reality Labs spending.

The options market reflects a balanced posture, with implied volatility behaving normally for a high-beta megacap and skew suggesting investors are willing to pay for downside protection without panicking.

Signals to Watch in the Coming Quarters

Five concrete signals will define how Meta's 2026 narrative evolves. The first is Family of Apps revenue growth net of foreign-exchange, with the implied advertiser-ROI commentary. Investors want to see continued evidence that AI-driven targeting and creative tools are translating into measurable lifts in advertiser performance — and that those lifts are translating into incremental ad spend rather than budget reshuffling.

The second signal is Reels and short-form ad-revenue contribution. The closing of the monetization gap between short-form and feed has been a multi-quarter project; the market wants visible confirmation that the gap is essentially closed and that Reels is a consolidated tailwind rather than a managed mix-shift drag.

The third signal is Reality Labs financials. Operating loss trajectory, hardware sell-through milestones for the latest mixed-reality device generation, and ecosystem metrics like developer activity and content library growth collectively determine whether the segment is converging on a credible path to scale. The market's tolerance for ongoing losses depends on these proof points.

The fourth signal is capex and capacity. Meta's AI infrastructure investment has been substantial, and the implied return — measured in advertiser-ROI lift and in cost savings on inference — is the swing variable for operating margin. Any commentary on capex discipline, depreciation roadmap, or open-weight Llama economics will move the multiple.

The fifth signal is regulatory exposure. Each major regulatory event in Europe, the U.S., or major emerging markets affects the practical operating environment for ad targeting and platform conduct. Investors should expect a steady drumbeat here and price it as a structural feature, not a sequence of surprises.

Outlook for the Rest of 2026

The base case is continuation: ad revenue compounds in the mid-teens; Reality Labs losses moderate as hardware milestones are hit; AI capex remains heavy but operating margin stays at industry-leading levels; the buyback continues to absorb a meaningful share of float. In that scenario, EPS growth runs ahead of revenue growth and the multiple defends itself on fundamentals.

The bull case is a step-change in AI-driven ad ROI plus an upside surprise on Reality Labs hardware adoption. The bear case is a regulatory shock to ad targeting plus a Reality Labs miss; that combination would test the multiple in a way it has not been tested in 2026.

Meta in 2026 has done what almost no one believed possible in 2022: turned a controversial multi-year capex bet into the cleanest AI-leveraged earnings story in the megacap universe.

For now, the +2.41% session is exactly the kind of measured participation that has defined the year. Meta is no longer the comeback trade of 2023. It is the compounder of 2026.

_06_11_2026_22_43_52_812084.jpg)

Please wait processing your request...

Please wait processing your request...