Alphabet (NASDAQ:GOOGL) hits all-time close at $344.40, $4.15T cap. Gemini, Cloud growth & Search resilience make Alphabet 2026's most underrated AI compounder. Dive in.

Key Highlights

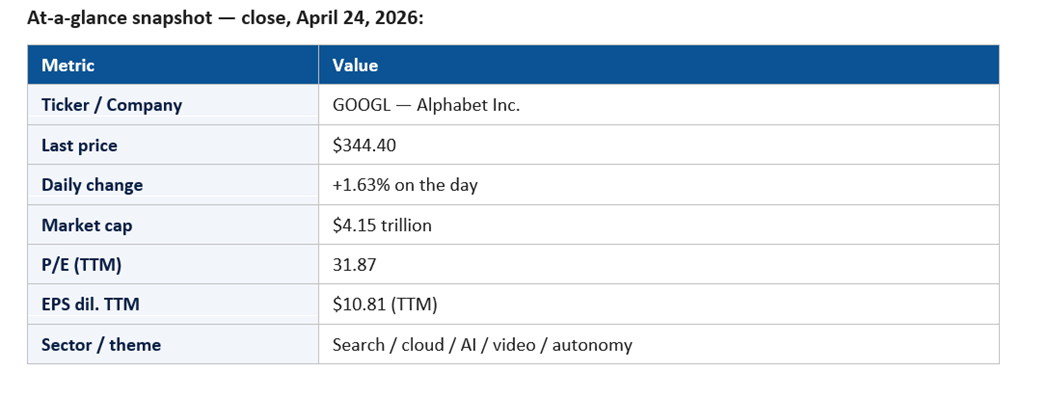

- April 24, 2026 was GOOGL's all-time closing high of $344.40

- At 31.87x P/E on $10.81 TTM EPS, Alphabet is cheaper than Amazon and Apple while sitting above both Apple and Microsoft in market cap at $4.15T.

- Google's $40B Anthropic investment — confirmed on the exact anchor date — makes Alphabet the only megacap simultaneously backing the two leading frontier AI labs.

Alphabet (NASDAQ:GOOGL) is the most multi-engine large-cap on the planet. It owns Google Search, the most monetized question-answering surface in the world; YouTube, the dominant video platform measured in attention and revenue; Google Cloud, the third hyperscaler with a fast-growing AI-platform layer; Android, the dominant global mobile operating system; the Gemini family of frontier AI models; the Pixel hardware franchise; the Waymo autonomous-driving business; and a portfolio of Other Bets including health, biotech, and quantum computing.

By 2026, the strategic story has flipped from defensive to offensive. The narrative that AI would unbundle Google Search has not gone away — but the offset story, in which Gemini-powered cloud, YouTube monetization, Search Ads modernization, and Waymo combine to drive consolidated revenue and margin higher, has gained the upper hand in investor consensus. The company that supposedly missed the moment in 2023 has in fact spent the last 18 months proving that distribution, data, and infrastructure are the AI moats that compound.

Stock Performance in 2026 (YTD)

GOOGL closed April 24, 2026 at $344.40, up 1.63% on the day, with a market capitalization of $4.15 trillion. That cap puts Alphabet decisively above Apple in the megacap pecking order, a reordering of the index that has been one of the year's notable structural shifts. With a P/E of 31.87 on $10.81 of TTM diluted earnings, Alphabet trades at a premium to the broad market but at a discount to several peers in the AI cohort — a multiple that reflects both the franchise quality and the residual market debate about Search disruption.

The implied YTD profile is one of methodical re-rating. Each catalyst — strong Cloud growth, calmer Search-disruption metrics, YouTube ad re-acceleration, Waymo expansion — has compounded into a steadily rising stock. The +1.63% session sits inside a regime where Alphabet participates in AI-infrastructure rallies without being whipsawed by them.

Key Price Movements and Milestones

Three milestones define the 2026 tape. First, the move through the $4 trillion mark and consolidation above it. That break has changed the way Alphabet shows up in passive flows and in benchmarks, with index-rebalancing dynamics now meaningfully supporting the stock on weak days. Second, the relative trade against Apple has reversed: GOOGL has steadily outperformed AAPL on AI-rally days, an inversion of the prior decade's pattern.

Third, the Cloud segment's contribution to consolidated growth has crossed a threshold that materially changes the consolidated revenue model. Cloud is no longer a growth-story option; it is a real-dollar, real-margin contributor to the consolidated print. That has been the most important structural change in the equity story across 2025–2026.

Major Catalysts: Why the Stock Moved

The dominant 2026 catalyst is Gemini-driven Cloud acceleration. Each quarter that Google Cloud prints high-twenties or low-thirties revenue growth — with a clear AI attribution — validates the Gemini-as-platform thesis and narrows the perceived gap to AWS and Azure. The implied operating margin trajectory is more bullish than the headline numbers, because incremental AI revenue carries higher unit economics than legacy infrastructure.

The second catalyst is Search Ads resilience under AI-overview product changes. The bear thesis was that AI-powered answers would crater the ad-load economics of Search; the data has been more nuanced. Investors who feared a step-down have instead seen a sustained, if slower, monetization of the same Search demand through AI-augmented surfaces. That has been the single most important narrative win of the year.

The third catalyst is YouTube. As linear TV continues to bleed share, YouTube — including YouTube TV and Shorts monetization — is the dominant aggregator of viewership and ad spend. Each quarter of double-digit YouTube ad growth supports the multiple.

The fourth catalyst is Waymo, increasingly visible as a genuine commercial line of business. While still a small contributor to consolidated revenue, the visible scaling of robotaxi operations across multiple cities has shifted Waymo from a moonshot narrative to an embedded growth optionality.

Macro and Fed-rate sensitivity is moderate; geopolitics matter mostly through advertising-cycle dynamics and through ongoing antitrust developments in the U.S. and Europe.

Sector Trends Influencing the Stock

Three sector trends underwrite the 2026 thesis. First, AI inference is becoming a hyperscale business. Alphabet's TPU roadmap, paired with Gemini, gives it a vertically integrated cost structure on inference that few competitors can replicate, and that is showing up in Cloud margin progression.

Second, the digital advertising market has stabilized after several years of structural transition. First-party data, AI-improved targeting, and the maturation of Performance Max and similar campaign types have repositioned Google Ads as a measurably higher-ROI channel relative to many alternatives.

Third, the autonomous-driving sector is consolidating around fewer credible players, and Waymo is one of them. As cities issue more permissive operating frameworks and as cost-per-mile improves, Waymo's revenue potential becomes increasingly modelable.

Competitive Positioning

Alphabet's competitive position in 2026 is multi-front. In AI models, Gemini sits among the top tier alongside the OpenAI/Anthropic/Meta cohort, and Alphabet's first-party distribution gives it a deployment advantage that pure-play model labs do not enjoy. In cloud, Google Cloud is closing the gap on AWS and Azure, particularly in AI-first workloads. In Search, the threat from AI-native search products remains real but has been smaller than feared.

In YouTube, the competitive moat is the combination of creator economy depth and monetization sophistication; TikTok remains a meaningful competitor for short-form attention but has not displaced YouTube's commercial primacy. In autonomy, Waymo competes with a small group of credible operators and a long tail of struggling ones.

The most underrated competitive vector is silicon. The TPU program is among the most strategically important assets at Alphabet, and its capacity expansion in 2026 is one of the quieter but more durable competitive advantages.

Financial Highlights

TTM diluted EPS of $10.81 on a $344.40 share price gives Alphabet a P/E of 31.87. Operating margin discipline remains a hallmark, with the consolidated operating margin holding at industry-leading levels even through a heavy capex phase. The combination of revenue growth, margin maintenance, and aggressive capital return is the financial signature of the equity story.

Capex has been substantial — Alphabet is one of the largest infrastructure spenders globally — but cash flow generation has remained healthy, and the buyback program continues to absorb meaningful share supply. Free cash flow conversion is trending in the right direction even with elevated AI spending.

Other Bets remain a modest financial drag, but the visible commercialization of Waymo has begun to change the conversation about whether the segment's losses are structural cost or strategic option value.

Key Risks and Challenges

The first risk is antitrust. Alphabet's exposure on multiple fronts — Search, ad-tech, Android distribution — makes the regulatory environment one of the most material risks to the equity story. Remedies that disrupt default-search or ad-tech bundling would be more material than typical antitrust outcomes.

The second risk is AI-driven Search disruption, which has not arrived in its most catastrophic form but remains a tail risk. The product transition to AI-augmented Search is delicate, and a misstep on monetization design could create real revenue pressure.

The third risk is capex digestion. Like the rest of the hyperscaler cohort, Alphabet is investing heavily in AI infrastructure, and any meaningful slowdown in cloud-AI demand growth would compress segment margin before revenue weakness becomes visible.

Finally, capital allocation expectations are increasingly demanding. Investors have come to expect both elevated capex and aggressive buybacks; a perceived shift away from either would create immediate share-price volatility.

Institutional and Investor Sentiment

Institutional sentiment on Alphabet has improved materially in 2026. The narrative of being the AI loser has been replaced by a more nuanced view in which Alphabet is one of the three platform-AI winners, alongside Microsoft and Amazon. Sell-side price targets have moved higher in lockstep, and bear cases have narrowed primarily to antitrust and Search-monetization risks.

The options market reflects a constructive but not euphoric posture, with implied volatility tame and call activity supportive. Alphabet in 2026 has earned its place as a core overweight rather than a story-driven trade.

Signals to Watch in the Coming Quarters

Five concrete signals will define how the Alphabet narrative evolves through the rest of 2026. The first is Google Cloud's growth rate and segment operating margin. Investors are calibrating the gap to AWS and Azure carefully, and any acceleration that demonstrably exceeds Azure's growth would be a major re-rating event for the multiple.

The second signal is Search ad revenue and AI Overview engagement metrics. The market has accepted that AI-powered Search can coexist with paid monetization, but the underlying question — whether AI surfaces sustain or expand revenue per query — has not been definitively answered. Any disclosed metrics on AI-driven query growth, ad load, or monetization-per-query will be central to the bull-versus-bear debate.

The third signal is YouTube. The combination of Shorts monetization, YouTube TV subscription growth, music subscriptions, and connected-TV advertising defines whether the segment continues to outpace traditional video advertising at scale. Each quarter the market wants visible evidence that YouTube is the dominant video monetization platform globally.

The fourth signal is Waymo. Ride volumes, geographic expansion, cost-per-mile improvement, and any disclosed unit economics will determine whether Waymo graduates from optionality to embedded growth. The market is increasingly willing to ascribe value to the segment, but only at a pace that matches commercial proof points.

The fifth signal is capital allocation discipline. Capex remains substantial, the buyback remains aggressive, and the dividend has become a recurring feature. Any meaningful pivot in the balance among these — particularly any deceleration in the buyback or any acceleration in capex without clear ROI commentary — would be a material narrative event.

Outlook for the Rest of 2026

The base case is continuation: Cloud prints accelerating AI-driven growth; Search Ads holds up under product transition; YouTube grows ads and subscriptions; Waymo expands without consuming disproportionate capital; capex moderates as efficiency improves. In that scenario, Alphabet defends its premium multiple and grinds higher.

The bull case is a step-change in Cloud share gains plus Waymo crossing into clear commercial scalability. The bear case is an antitrust outcome that disrupts the default-search economics or ad-tech distribution. The market is pricing the base case more heavily than the tails, but the tails are real.

Alphabet in 2026 has settled the most important question of the AI era: distribution beats novelty. The company with the most users, the most data, and the best AI infrastructure is harder to disrupt than the bears thought.

For now, the +1.63% session on a chip-led tape is the kind of measured participation that has defined Alphabet's year. The trade is no longer about whether Google can compete in AI. It is about how high the multiple goes when investors fully price the answer.

_06_11_2026_22_43_52_812084.jpg)

Please wait processing your request...

Please wait processing your request...