An equity research deep-dive on Advanced Micro Devices (NASDAQ:AMD), anchored on the April 25, 2026 close. The chip stock the market spent two years calling 'second source' just had the kind of session that rewrites the AI-silicon narrative.

Key Highlights

- AMD’s valuation reflects AI-driven growth expectations, with P/E exceeding 130x on forward earnings assumptions.

- Data-center accelerator momentum and EPYC share gains are reshaping revenue mix and growth outlook.

- High valuation sensitivity exposes the stock to execution and competitive risks in the AI cycle.

Advanced Micro Devices (NASDAQ:AMD) is a global semiconductor designer with a portfolio that spans server CPUs (EPYC), client and consumer CPUs (Ryzen), GPUs for gaming and data-center accelerators (Instinct MI series), embedded processors (the legacy Xilinx and Pensando businesses), and a growing AI-software stack. Under more than a decade of CEO Lisa Su's leadership, AMD has executed one of the most successful operational and strategic turnarounds in the history of the chip industry, reclaiming credibility against an Intel that lost its process leadership and emerging as the only credible direct competitor to NVIDIA in data-center AI accelerators.

By 2026, AMD's equity story is a three-part narrative. First, server CPU share gains against Intel have continued, with EPYC retaining a structural performance and total-cost-of-ownership advantage. Second, the data-center AI accelerator franchise — anchored by the Instinct MI series — has matured from credibility to commercial momentum. Third, the embedded and adjacent businesses provide diversification and a base of recurring revenue that smooths the cyclicality of the rest of the portfolio.

Stock Performance in 2026 (YTD)

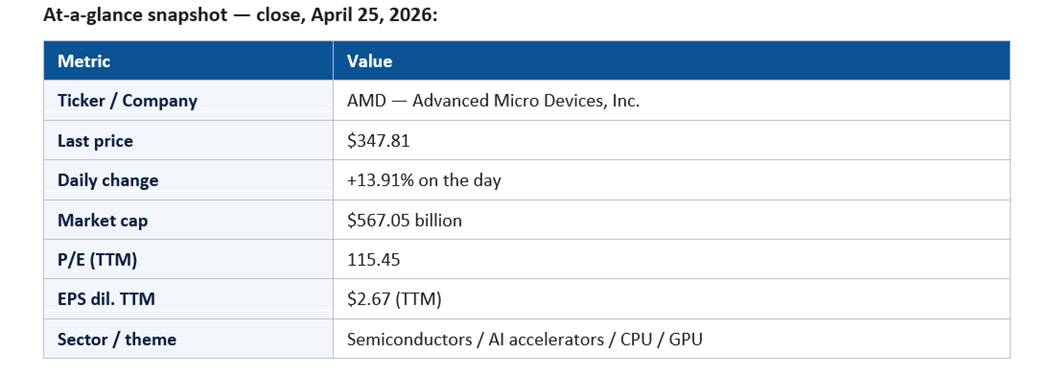

AMD closed April 25, 2026 at $347.81, up an extraordinary 13.91% on the day, with a market capitalization of $567.05 billion. The trailing P/E of 115.45 on $2.67 of TTM diluted EPS reflects a stock priced for very rapid forward earnings growth — a classic high-beta AI accelerator setup.

The April 25 session was the headline event of the week for the chip complex: AMD +13.91%, Intel +23.60%, Qualcomm +11.12%, KLA +6.59%, Micron +3.11%, NVIDIA +4.32%. That dispersion suggests a sector-level rerating in which the market is increasingly comfortable that AI-infrastructure dollars will spread beyond NVIDIA into a broader cohort of beneficiaries.

The implied YTD posture for AMD is one of high volatility tied closely to AI-narrative milestones, with the stock leading on days when the market believes the AI capex pie is expanding and lagging on days when it believes NVIDIA's share gains are unreplicable.

Key Price Movements and Milestones

Three milestones define the 2026 tape. First, the consolidation around and breakout from the $300 zone — a level that had functioned as resistance for several quarters before the April 25 break. Second, the relationship between AMD and NVIDIA has evolved: rather than the two trading purely against each other, both have increasingly traded with each other on days when AI capex narratives turn constructive.

Third, the disclosure cadence around MI-series accelerator design wins, hyperscaler commitments, and software-stack maturity has been the central narrative engine. Each step toward credibility on inference and training performance has shifted how investors price AMD's longer-term share of the AI-accelerator market.

Major Catalysts: Why the Stock Moved

The dominant 2026 catalyst is data-center AI accelerator commercialization. Each disclosure of a major hyperscaler design win, OEM partnership, or shipment milestone has been an immediate catalyst. The +13.91% session is consistent with a market reacting to a constructive AI capex setup that disproportionately benefits second-source silicon.

The second catalyst is server CPU share. EPYC continues to take share in the data-center CPU market against Intel, with each quarter of revenue and unit growth supporting the multiple. Server CPU is the steady, profitable engine underneath the more volatile accelerator narrative.

The third catalyst is the software stack. The maturation of ROCm, the developer-tooling ecosystem, and AMD's growing software talent base have all been narrative tailwinds. Software gravity is the principal moat protecting NVIDIA, and any progress AMD makes in narrowing that moat is read as bullish.

The fourth catalyst is M&A and partnership architecture. Each strategic acquisition, partnership, or co-development announcement that strengthens AMD's position in AI infrastructure has been a discrete narrative event.

Macro and Fed-rate sensitivity is meaningful — AMD is a high-beta name in a duration-sensitive cohort. Geopolitics, particularly export controls and access to China, is a structural overhang.

Sector Trends Influencing the Stock

Three sector trends underwrite AMD's 2026 thesis. First, the data-center AI accelerator market continues to expand faster than any single competitor can saturate, which provides meaningful runway for second-source providers. Second, the server CPU market continues to shift toward AMD even as Intel attempts to stabilize its product roadmap.

Third, the broader semiconductor cycle has remained constructive in 2026, with HBM, advanced packaging (CoWoS and competing technologies), and foundry capacity at TSMC all experiencing tight supply. AMD's ability to access the same scarce capacity as NVIDIA — at competitive terms — has been one of the under-appreciated structural enablers of the recent share-gain narrative.

Competitive Positioning

AMD's competitive position in 2026 is multi-front. In server CPU, AMD continues to be the share-taking incumbent against Intel, with EPYC's performance-per-watt and TCO advantages translating into design wins across the hyperscaler and enterprise customer base. In AI accelerators, AMD's MI series has emerged as the only credible direct competitor to NVIDIA's GPU lineup — not equal, but commercially viable for a meaningful subset of inference and training workloads.

In client CPU, AMD continues to compete with Intel for share in PC, gaming, and workstation segments. In embedded, the legacy Xilinx and Pensando portfolios provide stable, high-margin revenue and strategic optionality in adjacent markets like networking and edge AI.

The most underrated competitive vector is the open-software strategy. AMD's commitment to open-source ROCm and ecosystem support — combined with hyperscaler interest in not being permanently single-sourced on accelerators — has positioned the company as a strategic counterweight in customer procurement decisions.

Financial Highlights

TTM diluted EPS of $2.64 against a $347.81 share price gives AMD a P/E of 131.51. That multiple reflects an earnings base still scaling into the AI-accelerator opportunity; the market is paying for forward earnings growth, not for current run-rate.

Revenue mix has continued to shift toward higher-margin segments. Data-center revenue — both EPYC and Instinct — is the fastest-growing and the most-watched. Gross margin trajectory is constructive as the mix shifts, though near-term margin can be choppy depending on product cycle dynamics and inventory normalization.

Free cash flow has continued to scale as the AI franchise grows, providing the capital base to fund continued R&D investment, opportunistic M&A, and a measured capital return program.

Key Risks and Challenges

The first risk is competition with NVIDIA. NVIDIA's product cadence, software ecosystem, and customer relationships are all formidable, and AMD's ability to take and hold share against that incumbent is the central risk to the long-term thesis.

The second risk is execution. AMD's roadmap requires consistent delivery — on silicon performance, software stack maturity, and supply chain capacity. Any meaningful slip would compress the multiple sharply.

The third risk is China and export controls. A non-trivial portion of historic AI accelerator demand has been linked to China-related markets, and continued tightening of export rules constrains addressable demand.

The fourth risk is valuation gravity. A P/E above 130 leaves the stock highly sensitive to any disappointment, even a small one, and to broader risk-off rotations.

Institutional and Investor Sentiment

Institutional positioning in AMD is generally overweight in growth and tech-sector mandates. Sell-side opinion is broadly constructive, with the bull case anchored on AI accelerator share gains and the bear case anchored on competitive pressure from NVIDIA and on valuation.

The options market reflects elevated implied volatility, consistent with a high-beta AI name. Retail investor enthusiasm is meaningful and has been amplified during sessions like April 25's +13.91% print, which produces feedback loops between option flow and underlying price action.

Signals to Watch in the Coming Quarters

Five concrete signals will define how the AMD narrative evolves through the rest of 2026. The first is data-center accelerator revenue trajectory. Each quarter the market wants visible evidence that MI-series shipments are accelerating, that hyperscaler design wins are translating into volume, and that the implied dollar content per accelerator is consistent with the bull-case roadmap.

The second signal is server CPU share. Hyperscaler EPYC adoption, enterprise CPU mix, and Intel's competitive response collectively determine whether AMD's multi-year CPU share-gain trajectory continues. Any meaningful Intel product-cycle improvement is a watch item, but the AMD lead has been structural rather than cyclical for several years.

The third signal is software-stack maturity. ROCm version progression, developer-ecosystem momentum, framework integrations, and customer commentary on ease-of-deployment collectively determine whether AMD is closing or merely chasing the CUDA gap. Software gravity remains the principal NVIDIA moat, and any AMD progress here is read as bullish.

The fourth signal is supply chain and capacity allocation. Access to advanced TSMC nodes, advanced packaging (CoWoS or alternatives), and HBM availability are gating factors on revenue translation. Any visible improvement or constraint will move the consensus model.

The fifth signal is gross margin trajectory. The mix shift toward data-center accelerators is structurally margin-positive, but quarterly gross margin can be choppy depending on inventory dynamics, customer mix, and product transitions. Investors are calibrating both the long-run trajectory and the near-term volatility around it.

Outlook for the Rest of 2026

The base case is a continued grind higher in data-center revenue, with both EPYC and MI-series contributing. Software ecosystem progress reinforces customer adoption; capacity at TSMC and packaging partners remains adequate to meet demand. In that scenario, the AI accelerator share story sustains the multiple even if it does not expand it.

The bull case is a step-change in MI-series adoption — a hyperscaler signaling a meaningfully larger commitment than the consensus expects, paired with continued EPYC share gains. The bear case is a competitive setback (a meaningfully better NVIDIA product cycle than expected, or a credibility issue in MI-series rollout) that compresses the multiple from speculative to merely growth.

AMD in 2026 is the chip stock for investors who believe the AI capex pie is bigger than one company can serve. The April 25 session was the market putting real money behind that belief.

For now, the +13.91% print stands as the year's most explosive single-day move among the megacap chips. It reframes the AI-silicon narrative from monoculture to oligopoly. Whether AMD can sustain the move depends on the next two earnings cycles delivering on the implicit promises the tape is already pricing.

_06_11_2026_22_43_52_812084.jpg)

Please wait processing your request...

Please wait processing your request...