Key Highlights

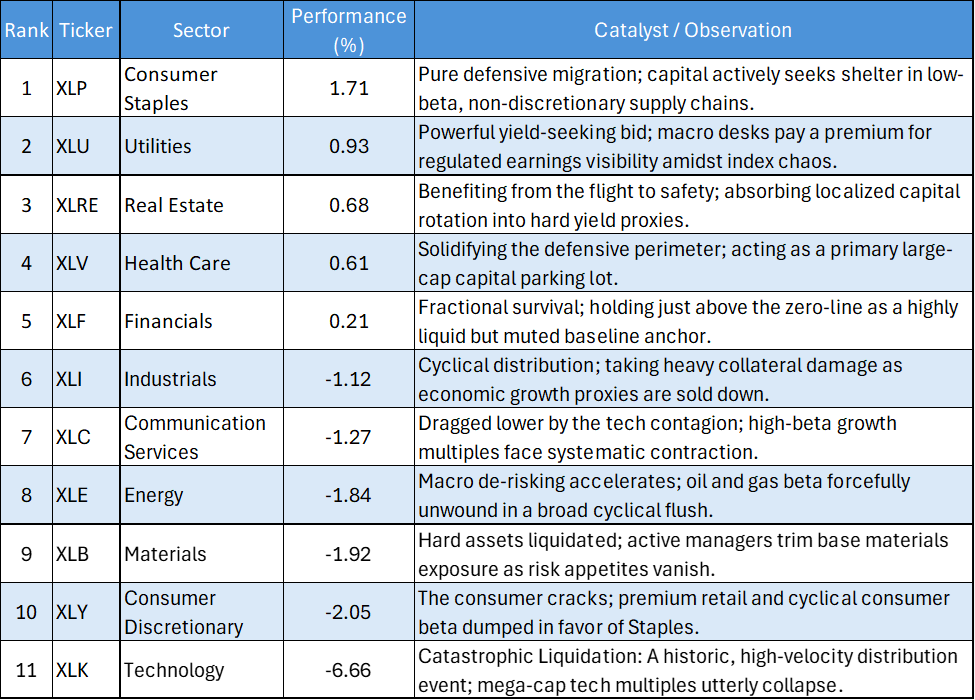

- The Mega-Cap Tech Meltdown: Technology (XLK) suffered a catastrophic structural collapse, plummeting a breathtaking -6.66%. This massive distribution event signals a violent multiple compression and a complete institutional buyer's strike in high-Beta growth.

- Aggressive Flight to Safety: In direct response to the tech carnage, Capital flooded into traditional defensive shelters. Consumer Staples (XLP) surged +1.71%, while Utilities (XLU) and Health Care (XLV) gained +0.93% and +0.61% respectively, confirming a pure risk-off rotation.

- Consumer and Cyclical Contagion: The growth shockwave dragged down the broader cyclical perimeter. Consumer Discretionary (XLY) tumbled -2.05%, closely followed by Materials (XLB) and Energy (XLE), as active managers rapidly de-risked portfolios across the board.

- Yield Proxies Catch a Bid: Alongside Utilities, Real Estate (XLRE) bucked the broader market sell-off with a solid +0.68% advance, absorbing Liquidity from funds hunting for safe-haven yield.

The US Equity market on June 5, 2026, was defined by a historic and violent capital rotation. The session witnessed a brutal, indiscriminate Liquidation of the Technology sector, triggering a shockwave that completely rewired the S&Amp;P 500's structural architecture. As trillions of dollars in mega-cap Market Value evaporated, institutional desks executed a textbook panic-rotation, aggressively stripping capital from high-beta, economically sensitive sectors and forcefully parking it into the lowest-Volatility, non-discretionary yield proxies available.

Daily US Sector Performance Summary

The following table summarizes the day's performance across the 11 major S&P 500 sectors, ordered by highest recorded return:

Key Market Themes

The Tech Wreck

The sheer magnitude of the destruction in Information Technology (XLK) is the defining macro event of the session. A nearly 7% daily plunge in the heaviest weighted sector of the S&P 500 is not a standard pullback; it is a violent, algorithmic liquidation event. Institutional desks systematically dumped mega-cap tech, indicating a profound breakdown in the growth thesis. The absolute evaporation of bid-side liquidity at these levels suggests that active managers are entirely unwilling to defend premium multiples, leaving the sector highly vulnerable to further downside momentum.

The Defensive Stampede

As the tech complex burned, the capital rotation into defensives was aggressive and highly concentrated. Consumer Staples (XLP) led the market with a +1.71% surge, underscoring a desperate need for Earnings certainty. Utilities (XLU) and Health Care (XLV) operated in perfect synchrony, absorbing the billions fleeing the growth complex. This triad of positive prints in a heavily down tape confirms that institutional funds are not moving to cash entirely, but rather executing a rigid, text-book transition into low-beta survival postures.

Cyclical and Discretionary Contagion

The Collateral damage from the tech flush severely wounded the broader cyclical and consumer landscape. Consumer Discretionary (XLY) plunged -2.05%, marking a stark bifurcation against the surging Staples sector, a classic indicator of mounting economic anxiety. Materials (XLB), Energy (XLE), and Industrials (XLI) all suffered deep distribution, confirming that the "risk-off" mandate extends far beyond tech. Global macro desks are forcefully reducing their exposure to any asset tied to cyclical economic expansion.

Financials Tread Water

In a tape characterized by extreme polarization, Financials (XLF) managed to eke out a +0.21% gain. While lacking the velocity of the pure defensive sectors, XLF successfully avoided the cyclical liquidation crossfire. Its ability to hold the green line suggests it is currently functioning as a highly liquid, neutral transition zone for capital reallocations rather than a primary target of either accumulation or distribution.

The empirical data from June 5 dictates an immediate, non-Negotiable shift toward capital preservation. A market that violently distributes its primary growth engine (XLK) by nearly 7% while simultaneously crowding into grocery and Utility stocks is flashing a massive systemic warning sign.

Active managers must respect the severity of the technology breakdown; attempting to catch the Falling Knife in XLK or XLY carries catastrophic portfolio risk. Core allocations must be ruthlessly restricted to the validated defensive sanctuaries (XLP, XLU, XLV) that are currently absorbing institutional flows. In a tape defined by this level of high-velocity, top-heavy destruction, aggressively defending the perimeter with yield and non-discretionary beta is the only mathematically sound survival strategy.

Please wait processing your request...

Please wait processing your request...