Key Highlights

- The Mega-Cap Distribution: Information Technology (XLK) suffered a severe Liquidation event, plunging 1.69% as institutional Capital aggressively unwound the crowded secular growth trade.

- Energy Dominates: Energy (XLE) surged 1.66%, acting as the market's undisputed leader as investors fiercely sought Inflation protection and hard-asset exposure.

- Defensive Whiplash: Reversing yesterday's Capitulation, traditional safety sectors caught massive bids. Real Estate (XLRE) and Consumer Staples (XLP) jumped 0.97% and 0.90%, respectively.

- Cyclical Breakdown: The economic expansion trade fractured, with Industrials (XLI) dropping 0.89% and Materials (XLB) shedding 0.73%, highlighting deep concerns over global Manufacturing and raw material Demand.

The US Equity market session on April 28, 2026, delivered another bout of severe rotational whiplash. Just one day after institutional Capital pivoted sharply toward the banking sector and stabilized tech, investors violently reversed course. The session was defined by an aggressive distribution out of the market's mega-cap technology anchors and cyclical industrials, with Capital flooding directly into the Commodity complex and battered defensive Yield proxies.

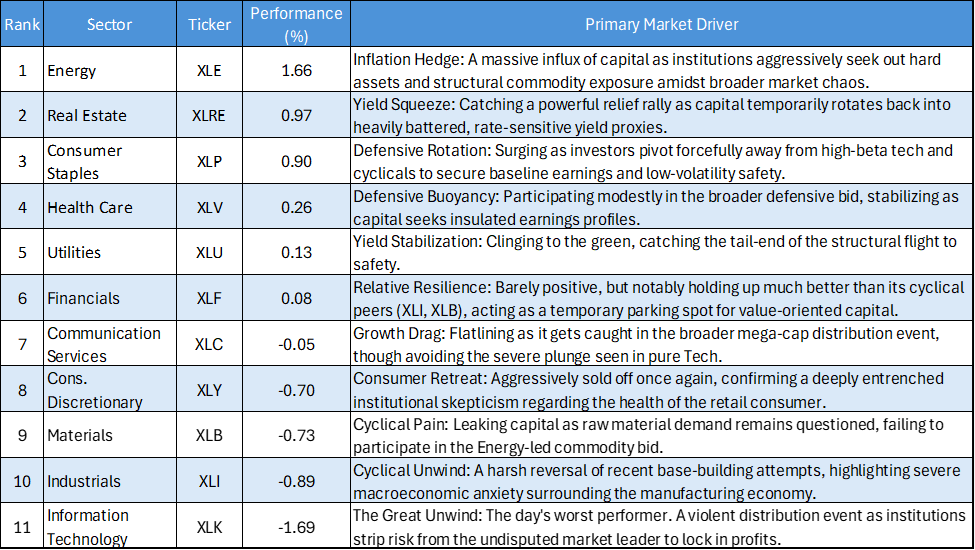

Daily US Sector Performance Summary (28/04/2026)

The following table summarizes the day's performance across the 11 major US S&P 500 sectors, ordered from the strongest to the weakest:

Key Market Themes

The Tech Fortress Fractures

The most critical takeaway from today's session is the aggressive Capitulation in Information Technology (XLK). Dropping a staggering 1.69%, the sector that has acted as the market's zero-duration bunker is suddenly facing intense selling pressure. When combined with the heavy 0.70% drop in Consumer Discretionary (XLY), it is clear that institutions are actively de-risking and moving aggressively to lock in profits from the previously crowded mega-cap growth trade.

Energy's Unstoppable Momentum

While the rest of the market engaged in erratic, risk-off behavior, Energy (XLE) ripped higher by 1.66%. This was not a subtle rotation; it was a definitive institutional mandate. The decoupling of Energy from other cyclicals like Materials and Industrials proves that this is not a broad economic expansion trade. Instead, it is a targeted, structural shift into the Commodity complex to hedge against sticky Inflation and global Supply constraints.

The Defensive Whiplash Returns

The tape showed a violent Reversal in the defensive complex. Yesterday, sectors like Consumer Staples (XLP) and Real Estate (XLRE) were aggressively liquidated. Today, they rocketed to the top of the board. This erratic, day-to-day whiplash in Yield proxies highlights an incredibly fragile market psychology. Capital is not confidently parking in defensives for the long term; rather, it is executing panicky, short-term tactical trades in response to intraday bond Yield Volatility.

Cyclical Vulnerability

The cyclical base-building narrative suffered a major blow today. While Financials (XLF) managed to barely hold the flatline (+0.08%), the broader economic engines, Industrials (XLI) and Materials (XLB), were heavily distributed. The market is demonstrating zero conviction in a broad-based Manufacturing recovery, actively shedding economic sensitivity as recessionary or stagflationary fears creep back into the institutional psyche.

The price action on April 28 confirms a highly treacherous trading environment completely devoid of reliable Market Breadth. The violent distribution in Tech (XLK) removes the market's primary safety net, exposing the broader indices to severe downside risk. Active managers must adopt a highly defensive and selective posture: overweight Energy (XLE) to ride the undeniable structural momentum, use the volatile pops in defensives (XLP, XLRE) to tactically hedge, and aggressively tighten stop-losses across the entire Technology and Cyclical complexes until genuine stabilization occurs.

Please wait processing your request...

Please wait processing your request...