_05_22_2026_03_02_02_312434.jpg)

Key Highlights

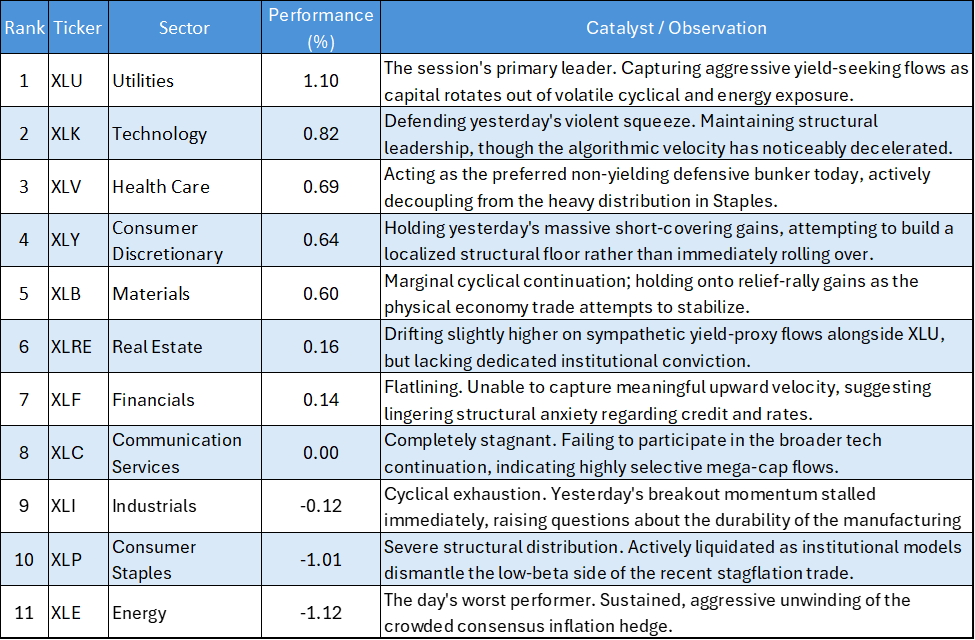

- The Energy Unwind Persists: The systemic Liquidation of the recent Inflation-hedge trade continues. Energy (XLE) was the worst-performing sector on the board, dropping -1.12%, confirming that yesterday's structural breakdown was not a one-off event.

- Utilities Capture the Defensive Bid: After severely lagging the recent rotational whiplash, Utilities (XLU) led the tape with a 1.10% gain. Institutional Capital is rotating back into pure Yield proxies to anchor portfolios amidst the broader market turbulence.

- The Growth Squeeze Decelerates: The violent short-covering event that fueled yesterday's massive tech and consumer rally is losing velocity. Technology (XLK, 0.82%) and Consumer Discretionary (XLY, 0.64%) posted solid gains to defend their recent breakouts, but the explosive algorithmic thrust has clearly cooled.

- A Fragmented Defensive Complex: The traditional safety trade is completely fractured. While Health Care (XLV) caught a solid 0.69% bid, Consumer Staples (XLP) suffered heavy distribution, plunging -1.01%.

The US Equity market session on May 21, 2026, delivered a tape characterized by rotational digestion and fragmented institutional flows. Following the extreme zero-sum whiplash of the prior 48 hours, active managers appear to be pausing to evaluate structural damage. The empirical data points to a market that is aggressively abandoning the previous "Stagflation Barbell" (dumping XLE and XLP), while tentatively defending the newly established growth squeeze (XLK, XLY) and parking excess Liquidity into yield proxies (XLU).

Daily US Sector Performance Summary 21/05/2026

The following table summarizes the day's performance across the 11 major US S&P 500 sectors, ordered from strongest to weakest:

Key Market Themes

The Energy Trap Hardens

The most actionable quantitative data point on the May 21 tape is the continued destruction of Energy (XLE). Dropping another -1.12% following yesterday's -2.43% plunge confirms that the institutional exit from the oil patch is persistent and structural. The "Energy Singularity" thesis has been entirely invalidated. It is no longer a Market Leader; it has transitioned into a primary funding source as active managers ruthlessly extract liquidity from trapped late-buyers.

Digesting the Growth Squeeze

Yesterday’s explosive +2.25% and +2.53% surges in Technology (XLK) and Consumer Discretionary (XLY) carried the exact mathematical footprint of a mechanical short squeeze. Today’s tape provided the crucial secondary test: would those gains immediately roll over, or could they hold? By posting positive follow-through (+0.82% and +0.64%), XLK and XLY successfully defended their higher ground. While the hyper-aggressive momentum has cooled, the lack of immediate distribution suggests institutional capital is tentatively willing to underwrite these higher valuations.

The Fractured Defensive Playbook

Standard market mechanics dictate that traditional defensive sectors (XLU, XLV, XLP) generally move with a high degree of correlation during times of macro uncertainty. Today, that correlation shattered. Utilities (XLU) and Health Care (XLV) were heavily accumulated, while Consumer Staples (XLP) suffered a severe -1.01% liquidation. This divergence suggests that active managers are no longer buying "safety" as a monolith; they are heavily scrutinizing individual sector valuations and yield premiums, actively rotating out of expensive staples to fund cheaper Utility exposure.

Cyclical Momentum Stalls

The highly anticipated revival of the physical economy hit a wall today. While Materials (XLB) managed a modest 0.60% gain, Industrials (XLI) slipped into the red (-0.12%). The inability of the industrial complex to string together consecutive days of powerful accumulation warns that yesterday's cyclical bounce may have been transient mean-reversion rather than the dawn of a durable economic expansion narrative.

The empirical data from May 21 dictates a transition from aggressive repositioning to tactical patience. The violent whiplash of the past 48 hours is settling into a fragmented, low-conviction tape. Active managers must respect the sustained breakdown in Energy (XLE) and enforce strict risk limits on any remaining exposure. The immediate tactical edge lies in monitoring the newly established floors in Technology (XLK) and Consumer Discretionary (XLY), if these sectors can consolidate without surrendering yesterday's massive gains, the mathematical probability of a sustained structural uptrend increases significantly.

_06_12_2026_23_00_13_327450.jpg)

Please wait processing your request...

Please wait processing your request...