Key Highlights

- Energy’s Massive Breakout: Energy (XLE) completely dominated the tape, surging a massive 2.29% as institutional Capital flooded into hard Assets and Inflation hedges.

- The Yield Proxy Liquidation: Traditional defensive sectors were violently unwound. Utilities (XLU) plunged 1.23% as the day's worst performer, while Real Estate (XLRE) dropped 0.61%.

- Tech Anchors the Broad Market: Information Technology (XLK) provided critical structural support, gaining 0.80% as investors utilized mega-cap growth as a zero-duration safety net.

- Cyclical Fracturing: The broader economic base fractured, with Materials (XLB) down 0.86% and Industrials (XLI) down 0.61%, confirming the Energy rally is an isolated Commodity bid rather than a broad economic expansion trade.

The US Equity market session on April 29, 2026, showcased a tape defined by an aggressive and targeted reallocation of institutional Capital. Investors forcefully unwound their exposure to rate-sensitive defensives and cyclical Manufacturing, funneling those proceeds directly into the Energy complex and mega-cap Technology. The session highlighted a market grappling with sticky Inflation expectations, completely abandoning traditional Yield proxies in favor of hard Assets and secular growth.

Daily US Sector Performance Summary 29/04/2026

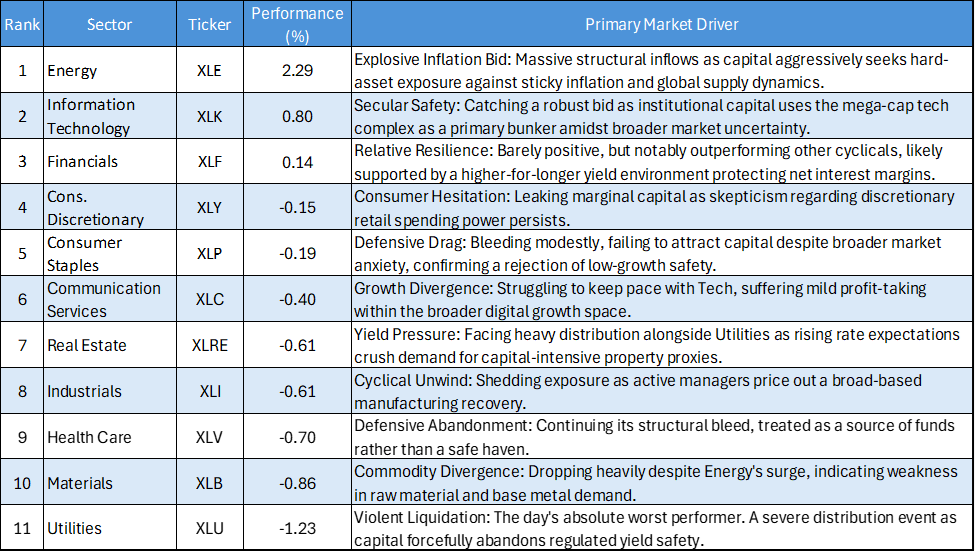

The following table summarizes the day's performance across the 11 major US S&P 500 sectors, ordered from the strongest to the weakest:

Key Market Themes

The Energy Decoupling

The standout feature of the session was the explosive 2.29% rally in Energy (XLE). More importantly, this occurred while the broader Materials (XLB) and Industrials (XLI) sectors suffered heavy losses. This decoupling is a critical macro signal: the market is not pricing in a booming global economy that requires more Manufacturing and raw materials. Instead, this is a highly concentrated, structural bid into energy as a pure-play Inflation hedge and hard-asset safe haven.

The Death of the Yield Trade

The defensive complex suffered an absolute bloodbath, led by a 1.23% plunge in Utilities (XLU) and a 0.61% drop in Real Estate (XLRE). This violent Liquidation suggests that bond yields are causing severe pain for Equity proxies. Institutional Capital is refusing to hide in low-growth, high-Dividend sectors, aggressively unwinding whatever safety trades were built up in prior weeks.

Tech Resumes its Role as the Bunker

With traditional defensives being sold off, Capital desperately needed a parking spot—and it found one in Information Technology (XLK). Generating a robust 0.80% gain on a day when 8 out of 11 sectors finished in the red, Tech proved it is still the market's primary load-bearing pillar. Investors are actively treating mega-cap tech balance sheets as superior safety profiles compared to traditional utilities or consumer staples.

Financials Stand Alone in the Cyclical Wreckage

While the cyclical Manufacturing base (Industrials and Materials) was heavily distributed, Financials (XLF) managed to stay afloat, eking out a 0.14% gain. This relative outperformance aligns with the sell-off in Utilities and Real Estate; a macroeconomic environment featuring sticky Inflation and "higher for longer" interest rates provides a tailwind for banking net interest margins, allowing the sector to weather the cyclical storm.

The tape from April 29 demands that active managers recognize a rapidly bifurcating market. The absolute abandonment of Utilities (XLU) and Real Estate (XLRE) proves that hiding in traditional Yield proxies is a toxic strategy in the current macro environment. Investors must respect the undeniable institutional mandate flowing into Energy (XLE) as an Inflation hedge, while maintaining core, unhedged exposure to Information Technology (XLK), which remains the only reliable structural anchor for broader Equity portfolios. Maintain tight risk parameters around the broader cyclical complex until Industrials and Materials prove they can catch a bid.

Please wait processing your request...

Please wait processing your request...