Key Highlights

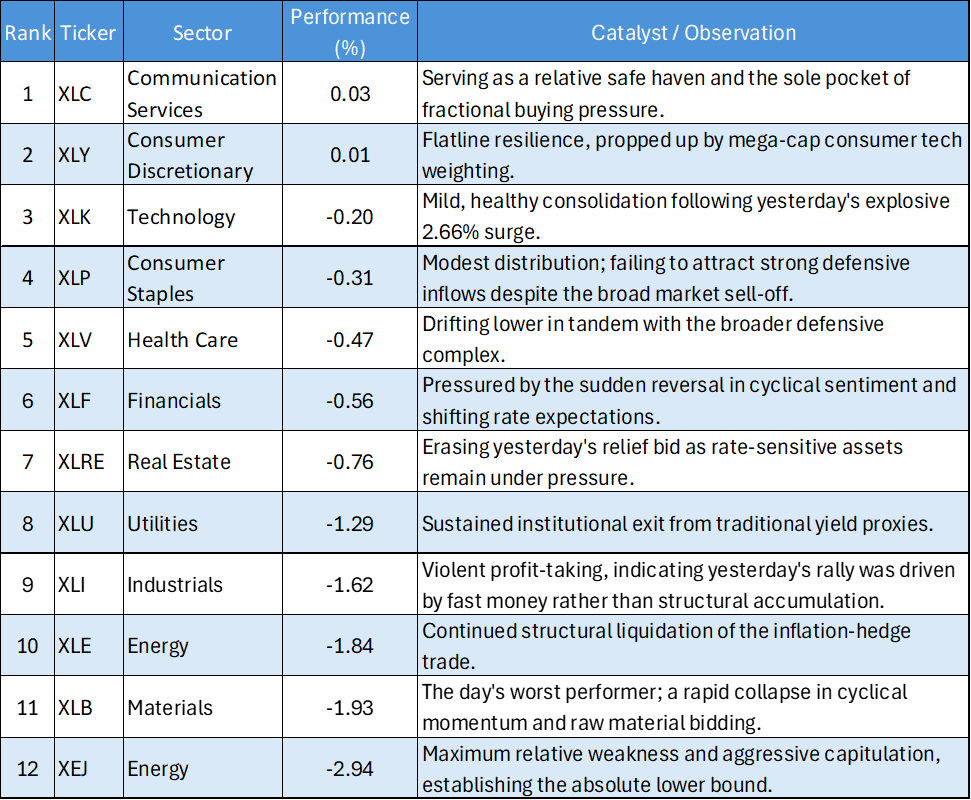

- The Growth Triad Acts as a Bunker: Communication Services (XLC) and Consumer Discretionary (XLY) were the only sectors to finish in positive territory, scraping by with 0.03% and 0.01% gains, respectively. Technology (XLK) saw a mild -0.20% pullback, acting as a relative safe haven.

- Cyclical Whiplash: After exploding higher in the previous session, the physical economy sectors suffered severe profit-taking. Materials (XLB) plunged -1.93% and Industrials (XLI) dropped -1.62%, instantly eroding their recent momentum.

- Energy's Sustained Bleed: The structural Liquidation in the oil patch continued. Energy (XLE) fell another -1.84%, confirming that the prior day's implosion was not a one-off anomaly but a sustained exit by institutional Capital.

- Broad Market Distribution: The tape was overwhelmingly negative, with 9 of the 11 S&P 500 sectors closing in the red, signaling a sharp risk-off recalibration following yesterday's euphoria.

The US Equity market session on May 7, 2026, delivered a severe bout of rotational whiplash. Just 24 hours after institutional capital forcefully bid up cyclical value and Manufacturing, that same capital was aggressively extracted. The tape was characterized by broad-based distribution across the physical economy, Yield proxies, and hard Assets. In a market suddenly devoid of risk appetite, investors defaulted to the fortress balance sheets of mega-cap growth, utilizing the sector as a zero-duration anchor to weather the rotational storm.

Daily US Sector Performance Summary 07/05/2026

The following table summarizes the day's performance across the 11 major US S&P 500 sectors, ordered from strongest to weakest:

Key Market Themes

Mega-Cap Growth as a Defensive Bunker

In a session defined by heavy selling pressure, the top of the board is highly revealing. XLC, XLY, and XLK completely insulated portfolios from the broader market wreckage. The fact that Technology (XLK) only gave up -0.20% after soaring +2.66% the day prior demonstrates immense structural gravity. When macroeconomic narratives shift violently, institutions are refusing to sell their core secular growth holdings, treating these mega-cap tech and communication monopolies as the ultimate defensive bunkers.

The Cyclical Reversal

The most alarming price action occurred in the cyclical complex. The sudden collapse of Materials (XLB) and Industrials (XLI) suggests that the previous session's explosive rally was heavily influenced by short-covering or speculative fast money, rather than high-conviction, long-term accumulation. The inability of the physical economy to string together consecutive days of outperformance warns that the market is still deeply skeptical of a sustained global manufacturing re-acceleration.

Energy Is a Falling Knife

The data from the Energy sector (XLE) demands strict risk management. Following a massive -4.12% liquidation event, the sector immediately followed up with another -1.84% drop. This is textbook distribution behavior. It confirms that the unwinding of the Inflation-hedge trade is ongoing, and institutional capital is systematically lowering its exposure to the energy complex regardless of intraday crude pricing.

The May 7 tape highlights a fragile and highly reactive market environment. The violent whiplash in the cyclical sectors (XLB, XLI) proves that the manufacturing and value trades remain highly vulnerable to sudden capital flight. However, the resilient performance of the Growth Triad (XLC, XLY, XLK) provides a clear empirical signal: secular growth remains the market's path of least resistance. Active managers must respect the ongoing distribution in Energy (XLE) and Utilities (XLU) while continuing to anchor portfolios to the relative safety of mega-cap technology.

_06_12_2026_23_00_13_327450.jpg)

Please wait processing your request...

Please wait processing your request...