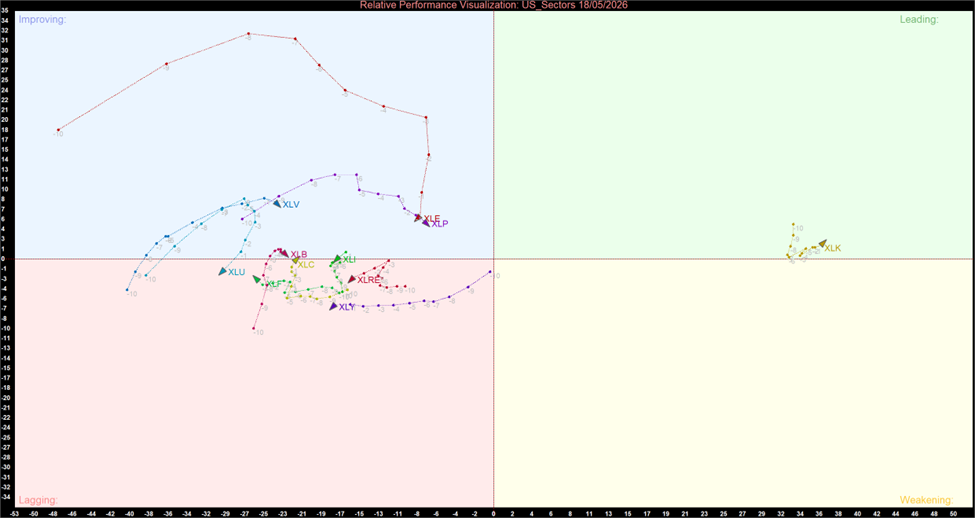

Key Momentum Highlights

- The Resilient Anchor: Despite another brutal absolute price drop (-1.08%), Information Technology (XLK) maintained its position as the solitary occupant of the Leading quadrant. This mathematical divergence proves that its relative structural strength remains superior to a rapidly collapsing broader market.

- The Stagflation Barbell: The Improving quadrant is exclusively occupied by Energy (XLE), Consumer Staples (XLP), and Health Care (XLV). This precise configuration confirms a forced institutional rotation into a stagflationary playbook: hedging Inflation via oil while hiding in absolute low-Beta safety.

- The Graveyard Quadrant: Seven of the eleven S&P 500 sectors are trapped in the Lagging quadrant. While rate-sensitive sectors like Financials (XLF) and Real Estate (XLRE) posted absolute daily gains, they remain structurally broken below the zero-line.

- Cyclical Capitulation: The physical economy trade is completely dismantled. Industrials (XLI) and Materials (XLB) continue to bleed relative momentum deep within the Lagging space, actively pricing in severe economic contraction.

The empirical momentum data from the May 18, 2026, session captures a market operating under extreme structural duress. The Relative Rotation Graph (RRG) presents a stark, highly polarized reality: the S&P 500 has fractured into a solitary, bruised anchor, a highly concentrated stagflationary life-raft, and a massive graveyard of structural laggards. Capital is entirely bypassing broad economic expansion trades, funneling rotational velocity exclusively into inflation hedges and non-yielding defensive bunkers.

Sector Momentum and Trajectory Summary

The following chart details the momentum quadrant positioning and visual trail vectors for the 11 major US S&P 500 sectors based on the May 18 close:

Quantitative Momentum Themes

The Relative vs. Absolute Paradox

The most critical quantitative lesson from the May 18 tape is the extreme divergence between absolute price action and relative momentum. Information Technology (XLK) closed at the absolute bottom of the performance board, yet it remains the only sector in the Leading quadrant. Because RRG measures performance relative to the benchmark, the broader market, dragged down by the structural collapse of cyclicals and the severe lag of consumer discretionary, is deteriorating so rapidly that XLK's relative standing holds the line. Tech is bleeding, but mathematically, the rest of the market is hemorrhaging faster.

The Ultimate Stagflation Barbell

The Improving quadrant provides a flawless mathematical footprint of institutional macroeconomic anxiety. Only three sectors are currently building upward relative velocity: Energy (XLE), Consumer Staples (XLP), and Health Care (XLV). Active managers are completely ignoring economic expansion trades. Instead, they are utilizing XLE to capture the Alpha of raw Commodity pricing power, while simultaneously utilizing XLP and XLV to drastically reduce portfolio beta.

The Unconfirmed Relief Bounces

Active managers must exercise extreme caution regarding the absolute daily gains seen in Financials (XLF, +1.25%) and Real Estate (XLRE, +1.20%). While these sectors provided index-level relief, their RRG profiles reveal them to be trapped deep within the Lagging quadrant. Their upward visual hooks are localized technical mean-reversions, classic dead-cat bounces following massive prior distribution, not the start of a confirmed structural accumulation phase.

The RRG momentum data from May 18 demands ruthless portfolio discipline and a total rejection of broad-Market Index tracking. The structural data dictates a highly concentrated, binary strategy. The "Staples + Energy" barbell (XLP, XLE) is the only confirmed source of upward relative velocity in the market. While Information Technology (XLK) mathematically retains its anchor status, its absolute momentum bleed requires strict risk management. All other exposure, particularly within the Lagging cyclical and rate-sensitive spaces, must be systematically liquidated, as they possess zero institutional momentum.

_06_12_2026_23_00_13_327450.jpg)

Please wait processing your request...

Please wait processing your request...