_05_17_2026_23_43_52_917151.jpg)

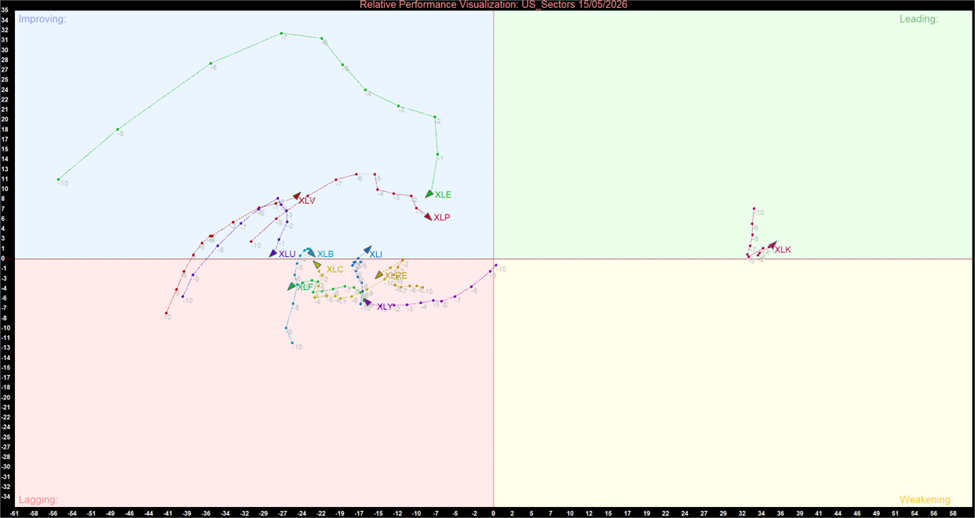

Key Momentum Highlights

- The Resilient Anchor: Despite a brutal absolute price drop, Information Technology (XLK) maintained its position in the Leading quadrant. This mathematical divergence proves that while tech suffered heavy absolute distribution, its relative structural strength remained superior to a rapidly collapsing broader market.

- The Energy Singularity: Energy (XLE) is the solitary momentum leader of the tape. Printing an aggressive North/North-East vector in the Improving quadrant, it is actively accelerating as Capital seeks an immediate, highly concentrated Inflation or geopolitical hedge.

- Defensive Bunkers Breached: The premium on non-yielding safety evaporated. Both Health Care (XLV) and Consumer Staples (XLP) rolled over, printing East/South-East vectors. They are bleeding relative vertical momentum as institutional de-risking forces a rotation into cash.

- Cyclical Destruction: The physical economy trade was completely dismantled. Industrials (XLI) and Materials (XLB) printed aggressive South/South-East hooks, invalidating any lingering thesis of a stealth cyclical accumulation phase.

The empirical momentum data from the May 15, 2026, session captures one of the most extreme structural stress tests in recent market history. The Relative Rotation Graph (RRG) illustrates a tape suffering from a severe macroeconomic shock. Capital violently abandoned the recent "Tech + Safety" barbell strategy, indiscriminately distributing both cyclical growth and traditional defensive bunkers. Yet, beneath the absolute price carnage, the quantitative footprint reveals that institutional models refused to completely decouple from the Tech anchor, while funneling all remaining rotational velocity into a singular, stagflationary hedge: Energy.

Sector Momentum and Trajectory Summary

The following chart details the momentum quadrant positioning and visual trail vectors for the 11 major US S&P 500 sectors based on the May 15 close:

US Sector Relative Momentum Chart (at the closing price of 15/05/2026). Powered by: amibroker.com

Quantitative Momentum Themes

The Relative vs. Absolute Paradox

The most critical quantitative lesson from the May 15 tape is the divergence between absolute price action and relative structural momentum. Information Technology (XLK) dropped a staggering -1.81% on the day, yet its RRG profile remained firmly rooted in the Leading quadrant. How? Because RRG measures performance relative to the benchmark. The broader market, dragged down by catastrophic losses in cyclicals and the Liquidation of defensives, deteriorated so rapidly that XLK's relative standing actually held the line above the 100 thresholds for RS-Ratio and RS-Momentum. Tech bled, but it bled slower than the rest of the market, confirming its status as the institutional default in times of panic.

The Energy Singularity

The RRG visually isolates Energy (XLE) as a singularity. In a tape where ten out of eleven sectors are printing vectors pointing South or East (indicating momentum decay or stagnation), XLE is the only asset driving aggressively North/North-East. This confirms a highly specific, forced capital migration. Active managers are not building diversified portfolios; they are executing a concentrated, binary trade to hedge against a sudden stagflationary or Commodity-driven shock.

The Breach of the Defensive Bunkers

Yesterday, the structural data dictated a "Tech + Safety" barbell. Today, the safety side of that barbell snapped. The rollover in Health Care (XLV) and Consumer Staples (XLP), evidenced by their sudden East/South-East vectors, proves that non-yielding safety is no longer immune to the macro shock. When these low-Beta bunkers bleed vertical momentum simultaneously with high-beta cyclicals, the empirical conclusion is that active managers are raising cash equivalents across the board to meet de-risking mandates.

Cyclical Capitulation

Any empirical edge supporting a stealth accumulation in the physical economy has been wiped out. The aggressive South/South-East hooks in Industrials (XLI) and Materials (XLB) confirm massive institutional capitulation. The market is aggressively unwinding global growth proxies, entirely rejecting the thesis of a near-term Manufacturing expansion.

The RRG momentum data from May 15 flashes a severe macro warning and dictates an extreme defensive posture. The structural resilience of Information Technology (XLK) in the Leading quadrant suggests holding core, high-conviction mega-cap tech is mathematically justifiable on a relative basis, but carries immense absolute drawdown risk in the near term. The tactical edge currently belongs entirely to cash equivalents and the isolated momentum singularity of Energy (XLE). All exposure to the fractured growth complex, Yield proxies, and the rapidly decaying cyclical trade must be rigorously managed or aggressively cut.

_06_12_2026_23_00_13_327450.jpg)

Please wait processing your request...

Please wait processing your request...