The S&P 500 faced significant pressure today as the narrative shifted from AI-driven optimism toward the "duration risk" posed by climbing Treasury yields. Much like the Australian market, the US session was characterized by a flight to "hard assets," leaving interest-rate-sensitive groups vulnerable.

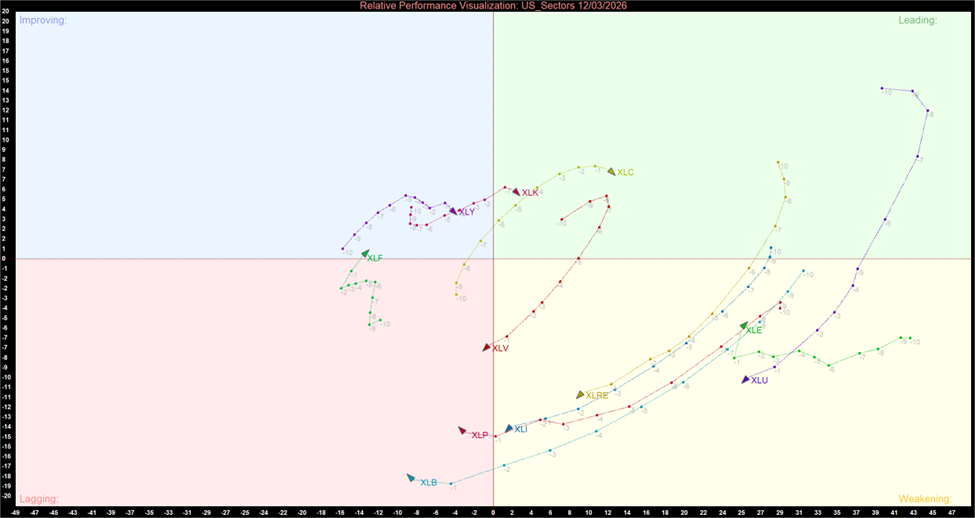

US Sector Relative Momentum Chart

US Sector Relative Momentum Chart (at the closing price of 12th March 2026). Powered by: amibroker.com

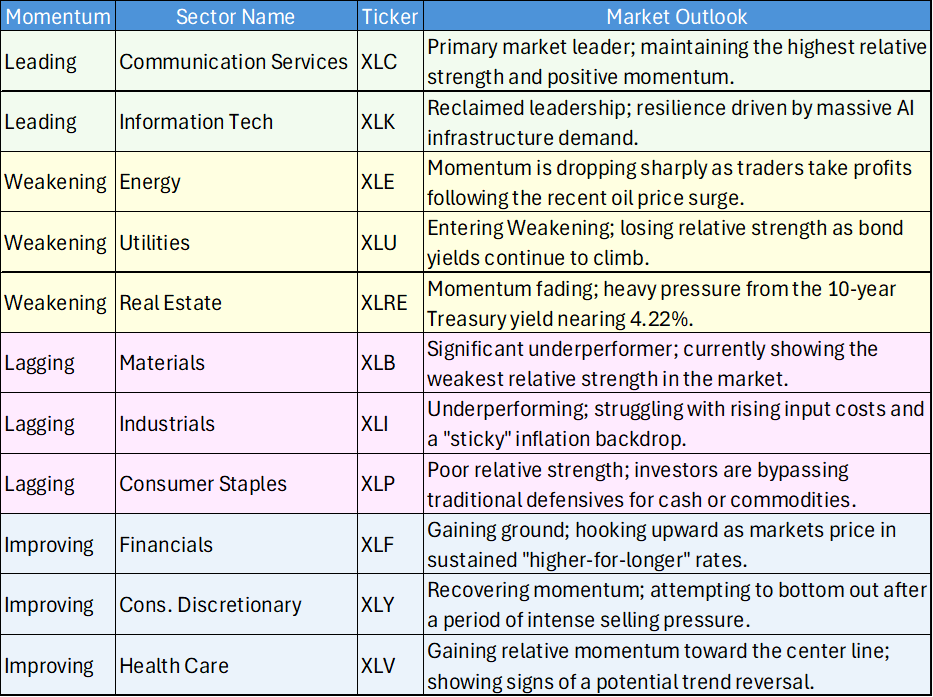

US Sector Momentum Summary Table

Leading Momentum

- XLC (Communication Services): Remains a primary market leader, maintaining the highest relative strength and positive momentum. Mega-cap stability continues to act as a sanctuary for institutional capital.

- XLK (Information Technology): Despite a "valuation squeeze" earlier in the week, Tech has pushed back into the Leading quadrant. The "Oracle effect", driven by a massive $553 billion AI backlog, continues to provide a fundamental floor for software and semiconductor names.

Weakening Momentum

- Although currently in the Weakening quadrant due to short-term profit-taking, the sector is showing strengthening momentum as it heads back toward the Leading quadrant. This suggests that the geopolitical "risk premium" remains firmly in place.

- XLU (Utilities) & XLRE (Real Estate): These sectors are losing their grip on leadership. As the 10-year yield creeps higher, these "bond proxies" are seeing their relative strength fade, regardless of their defensive nature.

Lagging & Improving

- XLB (Materials) & XLI (Industrials): These sectors remain in the Lagging quadrant, though they are beginning to show signs of bottoming. The "Real Assets" trade seen in the ASX is starting to manifest in the US, but it hasn't yet gained enough momentum to clear the Lagging zone.

- XLF (Financials): Financials are currently in the Improving quadrant, hooking upward toward a potential return to leadership as markets price in a higher probability of sustained interest rates.

Bottom Line

- The current US market landscape is defined by a sharp divergence between AI-driven growth and interest-rate-sensitive defensives. While rising Treasury yields pose a significant "duration risk" to broader indices, institutional capital is finding sanctuary in the mega-cap stability of Communication Services (XLC) and the massive backlogs within Information Technology (XLK).

- Concurrently, the persistent geopolitical "risk premium" continues to provide a tailwind for Energy (XLE), which is signaling a return to leadership despite recent profit-taking. Conversely, Real Estate (XLRE) and Utilities (XLU) remain vulnerable "bond proxies" as long as yields continue their ascent.

_06_12_2026_23_00_13_327450.jpg)

Please wait processing your request...

Please wait processing your request...