Key Highlights

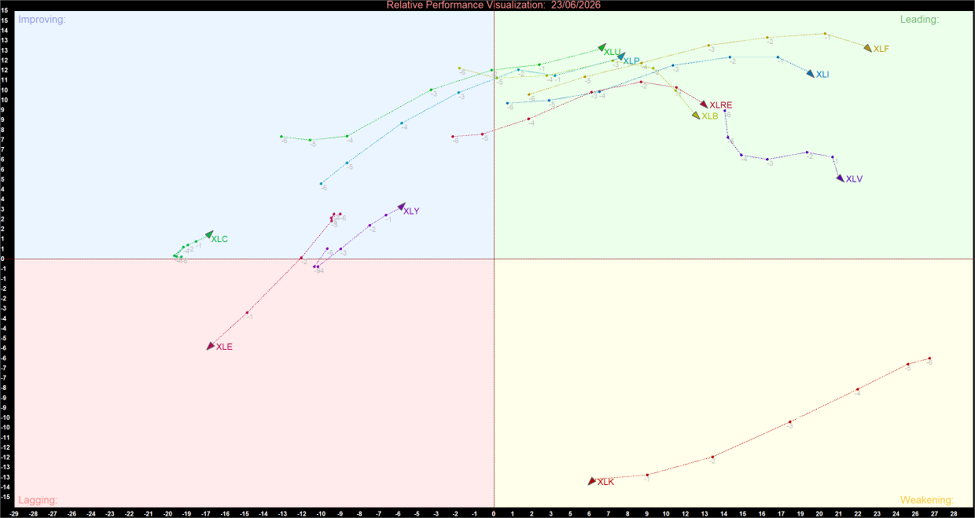

- Defensive Sectors Dominate Leadership: Consumer Staples (XLP), Utilities (XLU), Health Care (XLV), and Real Estate (XLRE) remain firmly positioned within the Leading quadrant, reflecting continued institutional preference for defensive and lower-volatility sectors.

- Financials Remain the Strongest Leader: Financials (XLF) occupy one of the most dominant positions within the Leading quadrant, maintaining superior relative strength despite a modest moderation in momentum.

- Technology Remains Isolated in Weakening: Information Technology (XLK) continues to be the sole occupant of the Weakening quadrant, highlighting significant momentum deterioration following an extended period of market leadership.

- Consumer and Communication Sectors Continue Improving: Consumer Discretionary (XLY) and Communication Services (XLC) remain in the Improving quadrant and continue to build positive momentum.

- Energy Recovery Continues: Energy (XLE) remains the only sector within the Lagging quadrant but continues to rotate North-East, suggesting gradual improvement in relative momentum.

The US sector rotation profile shifted further toward a defensive posture on June 23, 2026. The latest Relative Rotation Graph (RRG) shows defensive sectors consolidating leadership positions while Technology continues to lose momentum. At the same time, Consumer Discretionary and Communication Services are steadily improving, indicating that capital is selectively rotating into sectors showing strengthening relative momentum.

The overall structure suggests investors are prioritising capital preservation and earnings stability while maintaining selective exposure to areas showing improving momentum characteristics.

US Sector Momentum Summary

US Sector Relative Momentum Chart (at the closing price of 23/06/2026). Powered by: amibroker.com

Key Market Theme

Defensive Leadership Becomes More Dominant

- The most notable development on the chart is the strengthening leadership profile of defensive sectors. Consumer Staples (XLP) and Utilities (XLU) continue to advance within the Leading quadrant, while Health Care (XLV) remains one of the strongest sectors from a relative-strength perspective despite some loss of momentum.

- The strong positioning of these sectors aligns with the latest daily performance data, which showed significant buying interest in defensive industries. This suggests institutional investors are increasingly favouring stability and income-generating opportunities amid a more cautious market environment.

Financials Maintain Market Leadership

- Financials (XLF) remain among the strongest sectors on the entire chart. Although momentum has moderated slightly in recent sessions, the sector continues to display superior relative strength and remains firmly entrenched within the Leading quadrant.

- The persistence of Financials as a market leader indicates continued confidence in credit conditions, economic resilience, and earnings prospects across the banking sector.

Industrials and Materials Begin to Lose Momentum

- Industrials (XLI) remain comfortably within the Leading quadrant but have started rotating South-West, indicating a gradual loss of momentum. Materials (XLB) are exhibiting a similar pattern, suggesting investors are beginning to lock in profits after a period of relative outperformance.

- While both sectors remain leaders for now, continued momentum deterioration could eventually result in a migration toward the Weakening quadrant.

Technology Breakdown Accelerates

- Information Technology (XLK) remains isolated within the Weakening quadrant and continues to display one of the weakest momentum profiles on the chart. The sharp decline recorded during the latest session reinforces the ongoing loss of relative momentum.

- Although Technology continues to possess strong historical relative strength, institutional investors appear increasingly willing to diversify capital into other sectors offering stronger near-term momentum.

Consumer and Communication Sectors Continue Improving

- Consumer Discretionary (XLY) and Communication Services (XLC) remain firmly positioned within the Improving quadrant and continue to travel North-East. Their trajectories suggest strengthening investor sentiment and improving relative momentum.

- Should current trends persist, both sectors may eventually transition into the Leading quadrant and become part of the next wave of market leadership.

Energy Remains the Market's Sole Laggard

- Energy (XLE) continues to occupy the Lagging quadrant. However, unlike previous weeks, the sector is displaying a clear North-East trajectory, indicating that relative momentum is improving.

- While Energy remains the weakest area of the market from a relative-strength perspective, the current rotation suggests the sector may be entering the early stages of a longer-term recovery process.

Bottom Line

The June 23 RRG highlights a market increasingly dominated by defensive leadership. Consumer Staples, Utilities, Health Care, Real Estate, and Financials continue to occupy the Leading quadrant, reflecting strong institutional demand for stable earnings and lower-volatility exposures.

Meanwhile, Consumer Discretionary and Communication Services continue to strengthen within the Improving quadrant, Technology remains the market's primary area of weakness, and Energy continues its gradual recovery from Lagging. Overall, the current sector rotation profile suggests investors are favouring defensive positioning while selectively adding exposure to sectors exhibiting improving momentum characteristics.

Please wait processing your request...

Please wait processing your request...