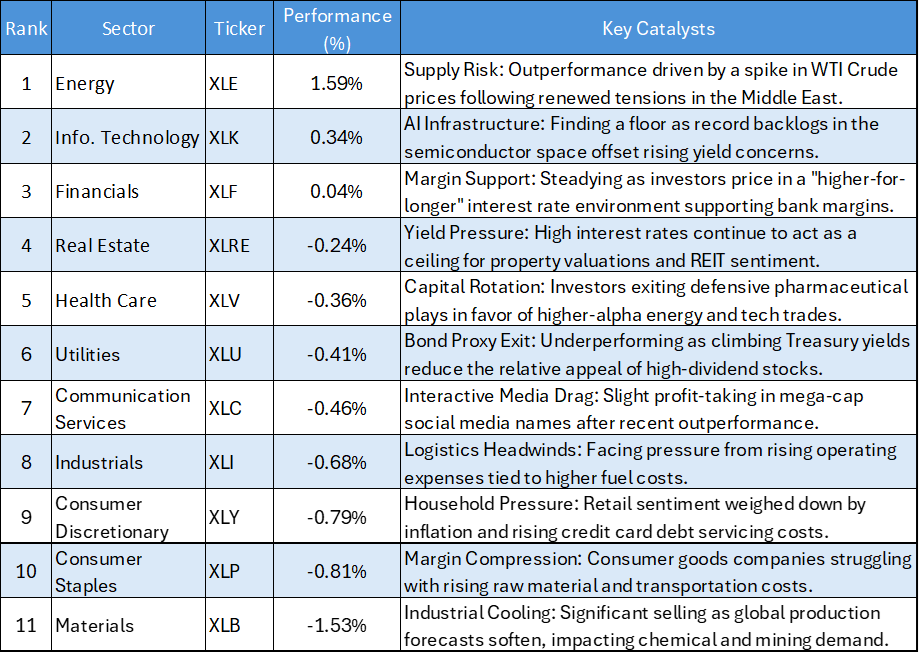

Key Highlights

- Energy Dominance: XLE led the market with a robust 1.59% gain, fueled by renewed geopolitical supply concerns.

- Tech Resilience: XLK managed a positive 0.34% close, showing signs of stabilizing after recent valuation pressures.

- Defensive Fragility: Yield-sensitive sectors like Utilities (XLU) and Real Estate (XLRE) remained in the red as treasury levels kept pressure on "bond proxies."

- Materials Slump: XLB was the day's primary laggard, dropping 1.53% amid cooling industrial demand forecasts.

The US equity market on March 19, 2026, showcased a concentrated rotation into the "Real Economy" and energy plays. While the broader indices faced headwinds from a strengthening dollar and "sticky" inflation data, the session was defined by a clear preference for inflation-hedged assets over broad-based defensive staples.

Sector Performance & Key Catalysts

The following table combines the daily performance data with the primary fundamental drivers influencing each sector:

Daily S&P 500 Sector Performances – 19/03/2026

Key Market Themes

The Energy "Safe Haven"

- Energy (XLE) remains the most consistent performer in the current environment. Unlike the broad market volatility seen in earlier sessions, the 1.59% gain today reflects a structural bid for revenue With oil prices pushing higher, Energy is serving as both a geopolitical and inflationary hedge.

Tech Stabilization

- After several sessions of being rattled by the 10-year Treasury yield, Information Technology (XLK) showed resilience today with a 0.34% gain. This suggests that the "valuation squeeze" is being partially offset by the immense cash flow generated by AI-focused blue-chip

Materials and Discretionary Divergence

- The sharp 1.53% decline in Materials (XLB) and the 0.79% drop in Consumer Discretionary (XLY) highlight a market concerned about the "real economy" impact of sustained high rates. Investors are increasingly wary of sectors sensitive to industrial cycles and consumer purchasing power.

Bottom Line

The session on March 19 highlights a tactical "pivot to power." With Energy and Technology leading while Materials and Staples lag, the market is favoring sectors with either high pricing power or significant structural backlogs. However, the continued weakness in Utilities and Real Estate signals that the market is not yet finished pricing in the risk of elevated interest rates.

_06_12_2026_23_00_13_327450.jpg)

Please wait processing your request...

Please wait processing your request...