A crowded macro calendar meets peak Earnings season. Tuesday brings results from GM, UPS, Coca-Cola, and Starbucks alongside the Consumer Confidence print and the Fed's first day of deliberations, the week's first real test of whether the April rally extends beyond AI.

Key Highlights

- Over one-third of S&P 500 companies report this week; Tuesday's slate spans autos, logistics, consumer staples, and tech.

- Semiconductors up 40% in April; the narrowest rally carrying the broadest index to record highs.

- Three Central Bank decisions in four days; no rate moves expected, but Powell's Wednesday tone is the week's real policy event.

- Brent above $106 as Iran talks collapse; fuel cost exposure runs through GM, UPS, and JetBlue simultaneously.

- S&P 500 Earnings growth revised to 15.1% for the year; Tuesday tests whether that holds beyond AI hardware.

Market Snapshot

U.S. Equity futures are little changed in early trading. The S&P 500 closed Monday at a record 7,173.91, up 0.12%, while the Nasdaq Composite gained 0.20% to 24,887.10. The Dow Jones Industrial Average slipped 0.13%, to 49,168. Brent Crude eased back toward $106 per barrel after reaching nearly $108 earlier in Monday's session, following reports that Iran submitted a new ceasefire proposal via Pakistani mediators. WTI futures are trading near $96. The U.S. 10-year Yield holds at 4.31%.

The Macro Context

April 28 is not a routine session. The S&P 500 has reached record territory in April, but on the back of a single trade in artificial intelligence hardware. Tuesday is where the Earnings story broadens into industrials, transport, consumer staples, and discretionary names. If the rally has limits, this week is where they begin to show.

The Iran conflict has entered its ninth week, with the IEA describing it as the largest energy Supply shock on record. The Strait of Hormuz remains effectively closed, constraining crude exports and sustaining upward pressure on global energy markets. That variable runs directly through GM, UPS, and JetBlue, three of Tuesday's most consequential reporters.

The Federal Reserve begins its two-day meeting today. No rate move is expected, but Powell's language on Inflation persistence and the labour market sets the interpretive frame for the rest of the week. The FOMC is already in pre-meeting communications blackout.

Economic Data to Watch

8:15 a.m. ET: ADP NER Pulse (Weekly Private Payroll Estimate) For the four weeks ending April 4, private employers added an average of 54,750 jobs per week, the fifth consecutive week of improvement. Any deceleration sharpens pre-Fed uncertainty.

9:00 a.m. ET: FHFA House Price index (February) A secondary release, but housing price trends feed directly into the Inflation expectations central to the rate path debate.

10:00 a.m. ET: Conference Board Consumer Confidence (April) The morning's most important print. March's headline reading was 91.8, but the forward-looking Expectations index fell to 70.9, a level historically associated with Recession risk, as anticipated discretionary spending declined across most categories. Further deterioration complicates the Earnings narrative for every consumer-facing name on today's calendar.

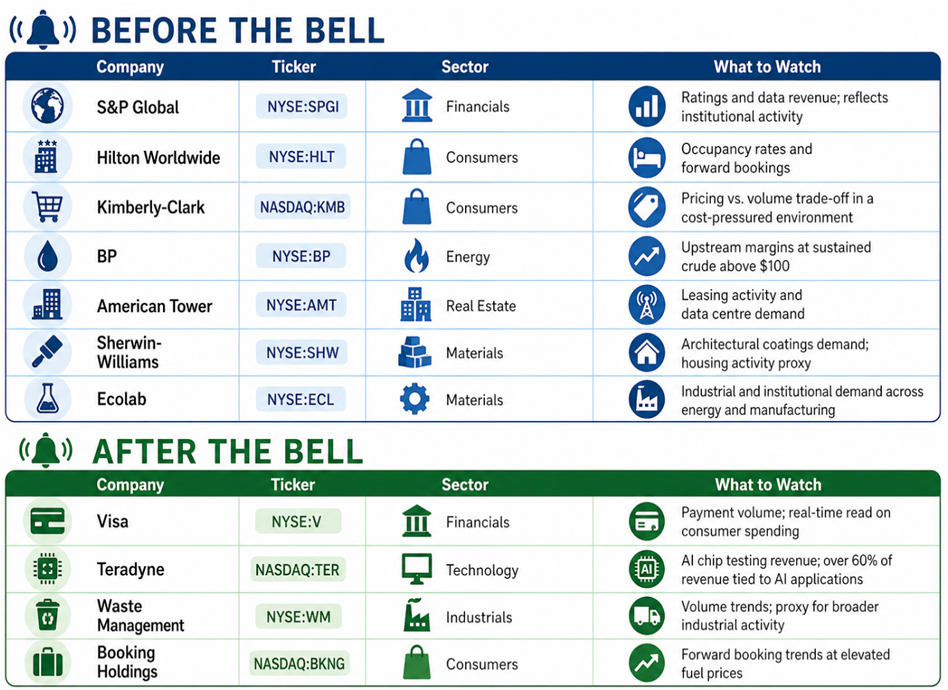

Earnings: Before the Bell

General Motors (NYSE:GM) Guidance on Volume trends and second-half pricing power matters more than the headline EPS. High-Margin trucks and SUVs anchor GM's Margin structure; sustained crude above $100 tests that thesis directly.

United Parcel Service (NYSE:UPS) Down more than 11% from its February high. Fuel Surcharge disclosures and forward Volume guidance determine whether this print marks a floor or extends the decline.

Coca-Cola (NYSE:KO) The session's most predictable reporter, having met or beaten estimates in each of its last 18 quarters. Watch organic Revenue growth in emerging markets, where pricing dynamics diverge most sharply from the U.S. Business.

Spotify (NYSE:SPOT) Gross Margin progression on podcasts and audiobooks is the operative metric. Profitability trajectory, not user growth, is what institutional investors are tracking.

JetBlue Airways (Nasdaq:JBLU) Highest variance of the morning. Jet fuel costs compound pre-existing structural constraints. Forward load Factor and Yield guidance drives the stock.

Corning (NYSE:GLW) Underrated on this calendar. Its optical connectivity Business is a direct read-through on hyperscaler Capital-expenditure/">Capital Expenditure commitment and the durability of the AI infrastructure buildout.

Earnings: After the Bell

Starbucks (Nasdaq:SBUX) The week's highest-stakes turnaround test. Starbucks has beaten estimates in fewer than 40% of the last 18 quarters against a GAAP EPS expectation of 41 cents. International Margin trends and return on structural Capital spending are the operative questions. A miss carries outsized weight given the recovery narrative already priced in.

Robinhood Markets (Nasdaq:HOOD) Trading volumes, Assets under custody, and Margin Loan growth serve as a real-time gauge of retail risk appetite at record market levels.

Also Reporting Tuesday

Source: Kalkine

One Number to Watch

The Magnificent Seven companies reporting this week face elevated expectations, needing to deliver solid Revenue growth to validate heavy AI spending. Alphabet (Nasdaq:GOOGL), Amazon (Nasdaq:AMZN), Meta Platforms (Nasdaq:META), and Microsoft (Nasdaq:MSFT), all reporting Wednesday, are each up more than 10% this month. Tuesday's industrial and consumer results provide the first read on whether the broader economy is keeping pace with the AI trade that has driven April's rally. The answer becomes considerably clearer by Wednesday's open.

Please wait processing your request...

Please wait processing your request...