Key market highlights:

- Geopolitical Relief Rally: US markets staged a tactical recovery as a "Hormuz reprieve" in the Middle East cooled global energy prices and eased immediate supply fears.

- Yield Correction Boosts Tech: The 10-year Treasury yield saw its largest one-day decline since mid-February, falling to 4.219% and reigniting the structural bull market for high-growth software and semiconductor names.

- Energy Sector Profit-Taking: Following a period of intense dominance, the Energy sector (XLE) pulled back as WTI Crude prices sank 4.75% to settle near $93.89 a barrel.

- AI Infrastructure Floor: A fundamental floor remains in the Technology sector, supported by record-breaking backlogs and new market entrants like BlockchAIn Inc. (AIB).

The US equity market faced a significant technical hurdle on Thursday, March 12, 2026, as a dramatic spike in global oil prices and climbing Treasury yields triggered a sharp reversal in investor sentiment. While the broader S&P 500 tumbled 1.5%, the session highlighted a stark divergence between "real economy" leaders and high-duration growth victims.

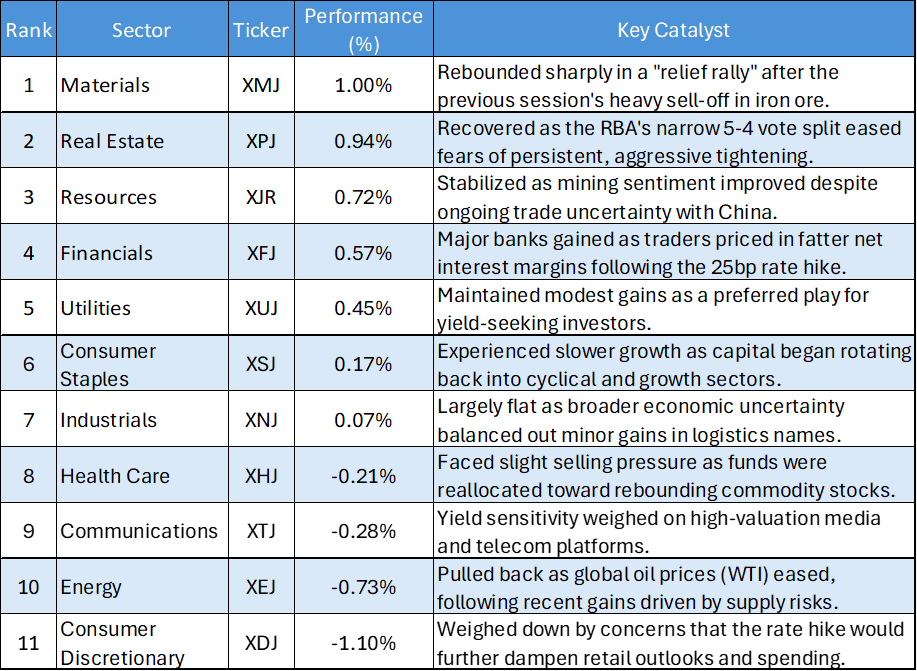

Sector Performance & Market Catalysts

The following table outlines the US sector performances and the fundamental drivers behind the day’s volatility:

Daily S&P 500 Sector Performances – 17/03/2026

Key Market Themes

The "Real Asset" Domination

Despite the broader market slump, Materials (XLB) and Industrials (XLI) continue to act as a sanctuary for capital. This shift represents a structural exit from "paper" growth assets in favor of the real economy, with Energy (XLE) still maintaining the highest risk-adjusted return (Sharpe Ratio of 0.42) year-to-date.

Treasury Yields: The Software Poison

The US 10-year Treasury yield surged to a five-week high of 4.26%, creating a "valuation squeeze" that disproportionately punished the Information Technology (XLK) sector. With a YTD return of -0.40% and high volatility, tech investors are currently not being compensated for the risks associated with rising rates.

The Fed's Hawkish Pivot

Sentiment regarding the Federal Reserve has turned violently hawkish. With oil prices threatening to keep inflation sticky near 3%, traders have pushed back expectations for rate cuts, with some officials now hinting at the possibility of further hikes to maintain price stability.

Bottom Line

The current market landscape is defined by a flight to "hard assets" as rising yields expose the fragility of high-growth valuations. While Energy and Materials provide a geopolitical and inflationary hedge, Real Estate and Consumer Discretionary remain in the "danger zone" as debt servicing costs and household pressures rise.

_06_12_2026_23_00_13_327450.jpg)

Please wait processing your request...

Please wait processing your request...