Key Market Highlights

- Energy De-escalation: WTI Crude oil prices sank 4.75% to settle near $93.89 a barrel, easing the "geopolitical risk premium" that had recently dominated the market.

- Yield Correction: The 10-year Treasury yield snapped a five-day rising streak, falling to 4.219% in its largest one-day decline since mid-February.

- Tech Resurgence: The Nasdaq Composite led the recovery, climbing 1.1% as lower yields allowed investors to rotate back into high-growth software and semiconductor names.

- New Market Entrants: Amid the volatility, a new AI infrastructure player, BlockchAIn Inc. (AIB), officially commenced trading on the NYSE today.

The US equity markets entered Tuesday with a newfound sense of resilience as a significant cooling in global energy prices triggered a broad-based relief rally. After weeks of being throttled by stagflation fears, the narrative has shifted toward a tactical recovery, supported by a "Hormuz reprieve" and a sharp decline in Treasury yields.

The "Hormuz" Reprieve and Inflation Sentiment

- The primary driver for the session's optimism was a shift in the Middle East conflict's impact on global trade. Reports that the US is allowing Iranian tankers to navigate the Strait of Hormuz, combined with diplomatic efforts to keep the waterway open, significantly reduced immediate supply disruption fears.

- This easing of energy costs has provided a critical breathing room for the Federal Reserve ahead of this week's monetary policy decision. While headline inflation stood at 2.4% in February, the recent spike in oil had threatened to push that figure toward 3.5%. The current retreat in crude prices is being viewed as a stabilizer that may prevent a "hawkish" surprise from policymakers.

The AI "Backlog" Floor

Despite the broader market swings, a clear fundamental floor has emerged in the technology sector. Information Technology (XLK) is no longer trading purely on macro sentiment but is increasingly supported by record-breaking backlogs.

- Oracle (ORCL): Maintained a steady floor at $155.95 after its historic Q3 earnings report, which saw both revenue and non-GAAP EPS grow by over 20% for the first time in 15 years.

- Nvidia (NVDA): Remained a focal point for institutional inflows, as investors prioritize companies delivering tangible returns on AI infrastructure investment.

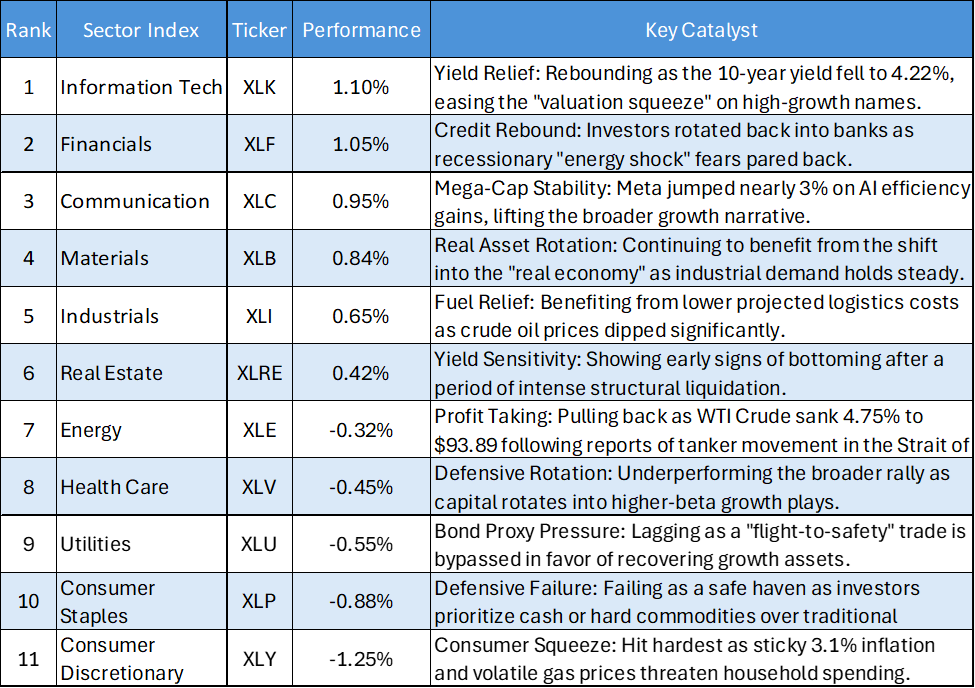

US Sector Performance Heatmap

The Growth Resurgence (XLK & XLC)

- Yield Relief for Tech: Information Technology (XLK) claimed the top spot with a 1.10% gain, directly benefiting from a retreat in the 10-year Treasury yield to 4.22%. This easing reduced the "valuation squeeze" that had recently hammered high-multiple software and semiconductor names.

- Mega-Cap AI Momentum: Communication Services (XLC) rose 0.95%, buoyed by a 3% jump in Meta. The gain was driven by optimism surrounding AI-led efficiency, which helped stabilize the broader growth narrative.

The Cyclical & "Real Economy" Pivot (XLF, XLB, XLI)

- Credit Confidence: Financials (XLF) gained 1.05% as recessionary fears linked to the recent "energy shock" began to fade, prompting investors to rotate back into the banking sector.

- Tangible Asset Support: Materials (XLB) and Industrials (XLI) continued their strong relative performance, gaining 0.84% and 0.65% respectively. Industrials specifically benefited from "fuel relief" as projected logistics costs dropped alongside falling oil prices.

The Energy Retreat (XLE)

- Profit Taking: Energy (XLE) was one of the few sectors to finish in the red, dropping 0.32%. This pullback followed a significant 4.75% sink in WTI Crude to $93.89 as reports of tanker movement in the Strait of Hormuz signaled a reduction in the geopolitical risk premium.

The Defensive Failure (XLV, XLU, XLP)

- Safe Haven Outflows: Traditional defensive sectors like Health Care (XLV), Utilities (XLU), and Consumer Staples (XLP) all underperformed, with losses ranging from -0.45% to -0.88%.

- Rotation to Beta: Investors bypassed these "bond proxies" in favor of higher-beta growth assets, signaling a temporary end to the flight-to-safety trade.

The Consumer Squeeze (XLY)

- Sticky Inflation Concerns: Consumer Discretionary (XLY) remained the worst performer, falling 1.25%. Despite lower gas prices, sticky 3.1% inflation continues to threaten household discretionary spending, keeping the sector under intense pressure.

Bottom Line

The US market has entered a tactical recovery phase as the immediate "oil shock" begins to recede. While Energy and Materials provided the necessary floor during the peak of the conflict, the cooling of 10-year yields to 4.22% has reignited the structural bull market in Tech and Communication Services. For investors, the focus shifts to whether this energy reprieve is permanent or merely a pause in a longer war of attrition.

_06_12_2026_23_00_13_327450.jpg)

Please wait processing your request...

Please wait processing your request...