Key Highlights

- Brent crude surged nearly 13% in three days following US-Israel strikes on Iran, marking the largest oil price jump since 2021

- The Strait of Hormuz handles nearly 20% of global oil flows, making it the single most critical chokepoint in global energy markets.

- Historical oil shocks, including the 1973 oil embargo and 1979 Iranian Revolution, triggered global recessions and massive price spikes

- Energy price shocks transmit directly into inflation, raising costs for fuel, aviation, chemicals, and heavy manufacturing sectors

- Rising geopolitical risk is already visible in financial markets as equity volatility and risk premiums increase across global assets

When the Button Gets Pushed

Military operations and oil markets share an uncomfortable relationship with timing. The Trump administration has demonstrated a clear preference for launching significant military actions over weekends, when energy futures markets are closed, trading desks are understaffed, and the immediate price response is deferred by roughly 36 to 48 hours. The underlying logic is defensible: give markets time to process the shock before liquidity conditions are thin. In practice, the buffer has provided less insulation than intended.

The strikes that killed Iran's Supreme Leader on a late February Saturday, coordinated between American and Israeli forces, targeting nuclear sites and senior leadership simultaneously, represent the most consequential act of direct military intervention in the Middle East in a generation. By Sunday evening, Brent crude had climbed past $82 per barrel. By Monday it settled near $80, still 13% above its pre-strike level. That is the largest three-day price movement in the global oil benchmark since 2021. The weekend strategy absorbed some of the shock. It did not neutralise it.

A Market Pricing Containment It Cannot Guarantee

The $80 price level implies a specific narrative: that the conflict remains bounded, that Iranian retaliation stays within manageable parameters, and that the physical flow of crude from the Gulf region continues without material interruption. Each of those assumptions is contestable.

Iran produces approximately 3.2 million barrels of crude per day, around 3% of global supply. Much of this flows to China through informal trade channels that partially circumvent Western sanctions. A direct disruption to Iranian output, while significant, would not on its own constitute a systemic supply shock. Global spare capacity, concentrated primarily in Saudi Arabia and the UAE, could theoretically offset a portion of lost Iranian volumes, though deployment timelines and political willingness are not guaranteed.

The more consequential risk is not what Iran produces, but where it sits. The Strait of Hormuz, the narrow waterway separating Iran's southern coastline from the Arabian Peninsula, handles somewhere between 17 and 20 million barrels of crude per day in transit. That represents approximately one-fifth of total global oil consumption moving through a corridor that is, at its narrowest, 33 kilometres wide. Saudi Arabia, Iraq, Kuwait, the UAE, and Qatar have no meaningful alternative export route for the majority of their output.

Iran has repeatedly signalled, across multiple administrations and multiple crises, that Hormuz access is a tool of last resort. An existential confrontation of the current magnitude is precisely the kind of scenario that brings last-resort options into consideration.

The Weight of Historical Precedent

Context matters when assessing the scale of what current market pricing is discounting. The 1973 Arab oil embargo, which removed far less than a Hormuz closure would, produced a fourfold increase in crude prices over several months and triggered recession across most of the developed world. The 1979 Iranian Revolution disrupted roughly 4% of global supply and doubled prices within twelve months. The Iraqi invasion of Kuwait in 1990 sent Brent up nearly 140% in a matter of weeks before a coordinated international response stabilised the market.

None of those historical episodes involved a direct American military role in killing a sitting head of state of a major oil-producing nation. The current situation is, by any measure, structurally distinct. That does not mean the outcome is necessarily worse. But the distribution of plausible scenarios is wider than the market's relatively composed response implies.

Macro Transmission: Beyond the Pump

Energy price shocks do not remain confined to commodity markets. The transmission mechanism into broader economic conditions is well-understood and operates across several channels simultaneously.

Consumer fuel costs rise directly. Input costs for energy-intensive industries: chemicals, fertilisers, aviation, heavy manufacturing, increase with a lag. Central banks, already navigating a careful disinflation path following the inflation cycle of 2021 to 2023, face a renewed complication: supply-driven inflation that monetary policy cannot address through demand compression without accepting growth costs.

For emerging market economies that import the majority of their energy requirements — India, Pakistan, much of Southeast Asia and Sub-Saharan Africa, an oil price shock of sustained duration is not merely a fiscal inconvenience. It creates current account deterioration, currency pressure, and in some cases, debt service stress.

The IMF's standard modelling suggests a $10 per barrel sustained increase in crude reduces global GDP growth by roughly 0.15 to 0.2 percentage points annually. A $25 to $30 shock, maintained over two or more quarters, is a materially different proposition.

The Equity Repricing Ahead

Capital markets have been slow to reprice the full range of implications. Energy sector equities: integrated majors, upstream independents, LNG infrastructure operators, stand to benefit from sustained price appreciation, and have moved accordingly.

The more complex repricing involves sectors that carry energy as a cost input rather than a revenue driver. Airlines, logistics operators, industrial manufacturers, and consumer staples companies with energy-intensive supply chains all face margin pressure that earnings consensus models have not yet fully absorbed.

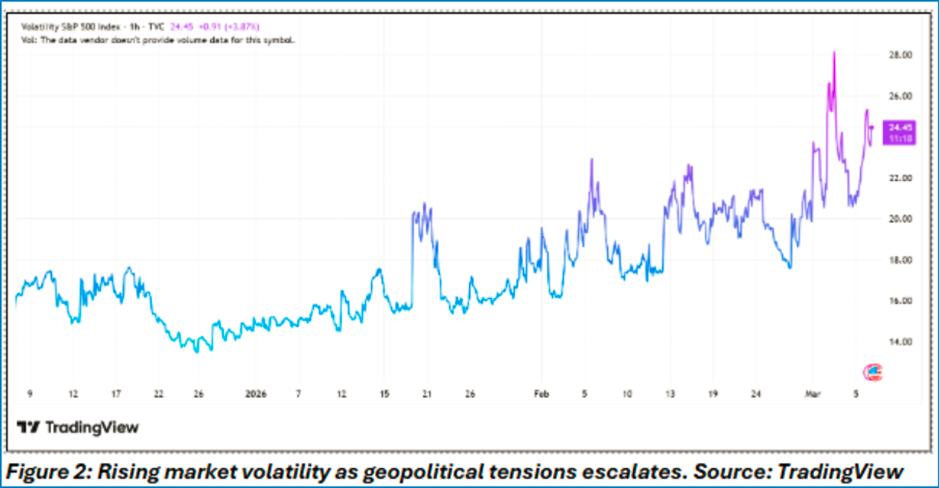

Institutional investors are recalibrating. The question is not whether sector rotation toward energy is warranted, it clearly is, in a sustained price environment but how to manage the correlated risk that a broader regional escalation introduces across asset classes simultaneously. Geopolitical risk of this magnitude does not stay contained in commodity markets. It leaks into credit spreads, equity volatility, and currency risk premiums across affected regions

This shift in risk sentiment is already visible in financial markets. The VIX index often referred to as Wall Street’s “fear gauge”, has moved sharply higher in recent sessions signalling that investors are beginning to price a wider range of geopolitical outcomes.

An Equation Without a Settled Answer

Oil markets are not, at their core, pricing mechanisms for physical barrels. They are discounting mechanisms for future states of the world. The current Brent price near $80 is the market's probability-weighted estimate of what the next six to twelve months look like across a distribution of scenarios ranging from rapid de-escalation to prolonged regional conflict. That distribution has widened materially in the past week.

The structural conditions for a sustained energy shock are present: a major producing nation in direct military confrontation with the world's largest military power, a critical chokepoint under potential threat, regional proxy networks activated across multiple theatres, and strategic petroleum reserves that provide a buffer measured in weeks rather than months. Whether those conditions translate into a durable supply disruption or a contained risk premium depends entirely on decisions being made in Tehran, Washington, and Riyadh in the coming days.

What the market is treating as a ceiling may yet prove to be a floor

Middle East tensions and the killing of Iran’s Supreme Leader have pushed oil markets toward their biggest shock in years. Brent crude has surged while investors price rising geopolitical risk, potential disruption in the Strait of Hormuz, and broader macroeconomic consequences.

FAQs

- Why are oil prices rising due to the Iran conflict?

Oil prices are rising because escalating military tensions in the Middle East increase the risk of supply disruptions, particularly in the Strait of Hormuz, through which roughly one-fifth of global oil trade passes. =

- What is the Strait of Hormuz and why is it important?

The Strait of Hormuz is a narrow shipping corridor between Iran and the Arabian Peninsula. Around 17–20 million barrels of oil per day transit through it, making it one of the most critical energy chokepoints in the world.

- Could the Iran conflict cause a global oil shock?

Yes. If military escalation disrupts production or shipping routes, global oil prices could spike significantly, similar to historical shocks such as the 1973 oil embargo or the 1979 Iranian Revolution.

- How do oil price shocks affect the global economy?

Oil price shocks raise fuel and transportation costs, increase inflation, pressure central banks, and slow global economic growth by raising production costs for energy-intensive industries.

- Why are financial markets becoming more volatile?

Geopolitical conflicts increase uncertainty for investors. As risks rise, financial markets often experience higher volatility, widening credit spreads, and shifting investment flows toward safer assets.

_06_12_2026_23_00_13_327450.jpg)

Please wait processing your request...

Please wait processing your request...