Key Highlights

- SpaceX is targeting a June 2026 Nasdaq IPO at a reported $1.75 trillion valuation, structured with 10-to-1 super-voting shares granting Elon Musk approximately 79% of votes on 42% Equity.

- OpenAI and Anthropic are expected to follow with hybrid corporate structures that concentrate operational authority with founding executives despite mission-driven framing.

- Historical precedents including WeWork and Enron show that governance designed to appear rigorous on paper can collapse entirely without independent oversight.

- Nasdaq's fast-entry rule compresses the window for new large-cap listings to enter the NASDAQ-100 to 15 trading days, legally compelling passive Capital inflows before governance reforms can be negotiated.

- Institutional investors, led by public pension funds, are lobbying for sunset clauses on dual-class structures with limited success to date.

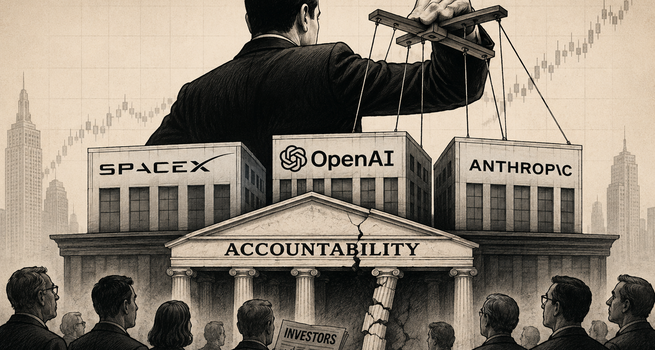

The Governance Architecture Nobody Is Fully Pricing

Three of the most consequential technology companies in history are approaching public markets simultaneously.

SpaceX, the rocket and satellite infrastructure firm that absorbed xAI in February 2026 in an all-stock deal valuing the combined entity at $1.25 trillion, is targeting a June 12 Nasdaq listing under ticker SPCX, seeking to raise up to $75 billion.

OpenAI and Anthropic are expected to follow later in 2026.

Each listing carries a shared structural feature that deserves more scrutiny than valuation multiples are currently receiving: governance frameworks that concentrate authority in individual founders while minimising the mechanisms designed to check them.

This is not an argument against founder-led companies. The case for mission-driven, long-horizon Leadership has genuine intellectual merit. The 2008 financial crisis demonstrated that compliant governance on paper does not prevent institutional failure. The backlash against short-termism in public markets is legitimate. The concern is more specific: the speed, scale, and potential irreversibility of what these companies are building makes the simultaneous weakening of accountability structures particularly poorly timed.

Super-Voting Equity and the Limits of Public Ownership

SpaceX's prospectus confirms a dual-class share structure. Class A shares sold to public investors carry one vote each. Class B shares held by Musk and insiders carry ten votes each. The result is that public shareholders absorb economic risk without acquiring meaningful governance influence. This model, institutionalised at Alphabet (NASDAQ:GOOGL) and subsequently adopted at Meta Platforms (NASDAQ:META), is now standard in large-cap technology. SpaceX applies it at greater concentration than either predecessor.

The WeWork (Delisted, 2023) episode between 2019 and 2020 illustrated the failure mode in practice. Adam Neumann held shares with 20-to-1 voting power, transacted extensively with his own company, and sold $700 million of personal stock ahead of an IPO that collapsed from a $47 billion implied valuation to below $8 billion within weeks of its prospectus release. The board lacked either the independence or the structural authority to intervene before the damage was done. SpaceX's structure does not replicate those specific facts, but the accountability architecture is comparable: a founder whose decisions cannot be reversed by the shareholders bearing the financial consequences.

Compounding this, SpaceX plans to use SEC-permitted controlled company exemptions that allow it to forgo an independent board and compensation committee entirely. These committees exist precisely to prevent a chief executive from setting their own remuneration without external review.

Jurisdiction Arbitrage and Forced Passive Flows

After a Delaware court challenged Elon Musk's Tesla (NASDAQ:TSLA) compensation package on grounds of insufficient board independence, SpaceX reincorporated in Texas, whose Business Court applies more director-friendly standards. Regulatory geography is now a governance variable, not a fixed constraint.

Nasdaq's revised fast-entry rule adds a market structure dimension. Large newly listed companies can now enter the NASDAQ-100 after 15 trading days rather than three months. Index Funds tracking that benchmark are mandated to hold all constituents. The practical effect is that passive capital will be obligated to purchase SPCX within weeks of listing, before institutional investors have time to extract governance commitments through conventional pre-IPO Leverage. Active fund managers lose their primary negotiating tool at the point of entry.

States and exchanges competing for prestige listings are inadvertently producing a Race to the Bottom on governance standards. The issuer captures the benefit; the public investor absorbs the residual risk.

Mission Structures That Protect Founders More Than Missions

OpenAI's restructuring into a Public Benefit Corporation leaves its original nonprofit foundation with a 26% stake and formal authority to appoint directors. Anthropic's Long-Term Benefit Trust is designed so independent experts, rather than shareholders, elect a majority of directors over time. Both structures carry genuine design ambition and represent genuine departures from standard venture-backed governance.

The operational reality is more qualified. OpenAI's nonprofit and PBC boards overlap significantly, with many members installed following the reinstatement of Sam Altman as chief executive. Anthropic's trustees serve one-year terms, must consult the CEO on appointments, and can be removed by a Shareholder supermajority that includes Amazon (NASDAQ:AMZN) and Alphabet without Trustee consent. The trust provides a procedural guardrail. It does not constrain ultimate authority.

A relevant precedent at smaller scale: Ben and Jerry's mission protections embedded in its 2000 Acquisition by Unilever (NYSE: UL) functioned reasonably for years. In 2022 a commercial decision by the parent effectively overrode the Subsidiary's mission-driven board on a significant policy question. Advisory structures hold until the party with final authority decides otherwise.

What Institutional Investors and Regulators Should Consider

Institutional lobbying for sunset clauses, which would automatically convert super-voting shares to ordinary shares after a defined period, represents the most tractable near-term reform. It has not yet produced structural concessions from any of the three companies approaching public markets.

The Theranos case established a related principle: a board populated with prestigious but non-technical members does not substitute for genuine independent oversight. Elizabeth Holmes raised nearly $1 billion before the underlying technology claims were exposed. The board lacked either the expertise or the independence to surface the problem earlier. The parallel to AI companies is imperfect but the structural lesson is not: a board chosen for alignment with the founder rather than independence from them is not performing the function a board exists to perform.

For regulators, the timeline is pressing. Recent previews of frontier AI capabilities from companies including Anthropic have indicated that oversight agencies are already struggling to evaluate what these systems can do, let alone govern the organisations deploying them. Rules written for standard corporate structures, with functional independent boards and stable legal jurisdictions, will have systematic gaps when applied to entities that have deliberately avoided both.

The historic scale of these IPOs reflects genuine technological and commercial achievement. The governance structures surrounding them reflect a different calculation: the systematic reduction of accountability mechanisms at precisely the moment their absence carries the highest potential cost.

_06_12_2026_23_00_13_327450.jpg)

Please wait processing your request...

Please wait processing your request...