_01_13_2026_04_31_32_015906.png)

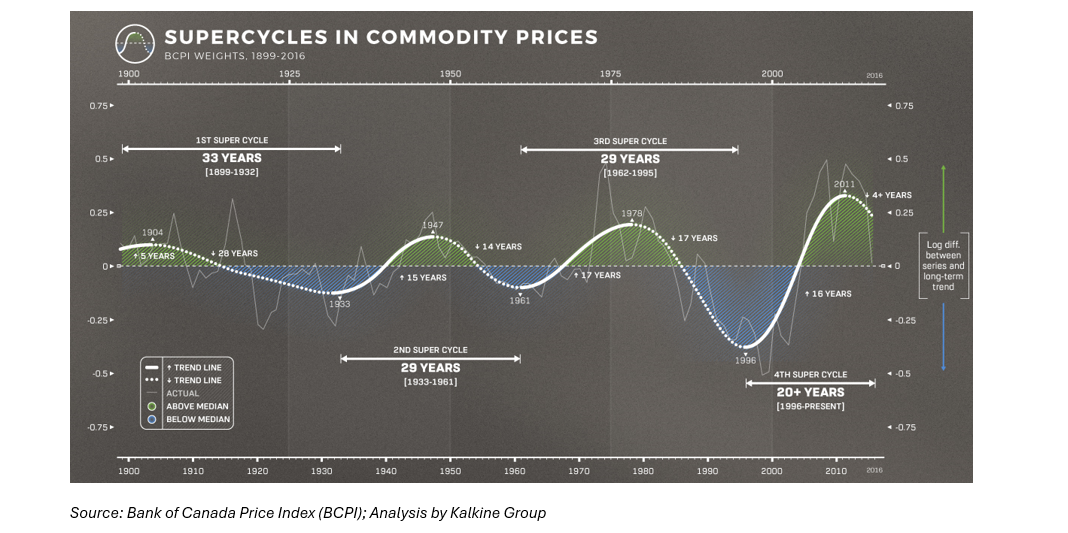

A Commodity Supercycle refers to a prolonged period — often lasting 10 to 20 years or more — during which demand for raw materials rises faster than supply, driving sustained increases in commodity prices. Unlike normal commodity cycles, which are typically driven by short-term economic fluctuations, supercycles are underpinned by structural shifts in the global economy.

As we move through the mid-2020s and into 2026, investors are once again debating whether the world is entering a new Commodity Supercycle — and what that could mean for ASX-listed resource stocks, which remain some of the most commodity-leveraged equities globally.

A Brief History of Commodity Supercycles

Historically, commodity supercycles have coincided with periods of major industrial transformation.

- Post-World War II industrialisation (1940s–1960s): Rapid rebuilding and manufacturing growth in the United States and Europe drove enormous demand for steel, copper, oil, and coal.

- China’s urbanisation boom (early 2000s): China’s entry into the World Trade Organization and massive infrastructure investment triggered a multi-year surge in iron ore, coal, copper, and energy prices — a period that transformed the mining sector.

In each case, the key ingredients were the same: new sources of demand, limited short-term supply elasticity, and years of elevated capital investment across the resources sector.

Why a New Supercycle Is Being Discussed in 2026?

The Current Supercycle thesis differs from past examples. Rather than being driven by a single country’s industrialisation, it is shaped by multiple global forces acting simultaneously:

- Energy Transition and Electrification

The shift toward renewable energy, electric vehicles (EVs), grid-scale storage, and electrification of transport and industry is dramatically increasing demand for battery and conductive metals.

- Decarbonisation Commitments

Governments and corporations are committing trillions of dollars to emissions reduction targets, which require vast quantities of metals such as copper, lithium, nickel, and rare earths.

- Supply Constraints

Years of underinvestment following the last commodity downturn have left supply pipelines thin. New mines are capital-intensive, slow to permit, and increasingly constrained by ESG and geopolitical considerations.

- Geopolitical Fragmentation and Resource Security

Countries are prioritising domestic and allied supply chains, leading to duplication of infrastructure and higher long-term demand for strategic commodities.

Together, these forces have created the conditions for persistent commodity tightness rather than short-lived price spikes.

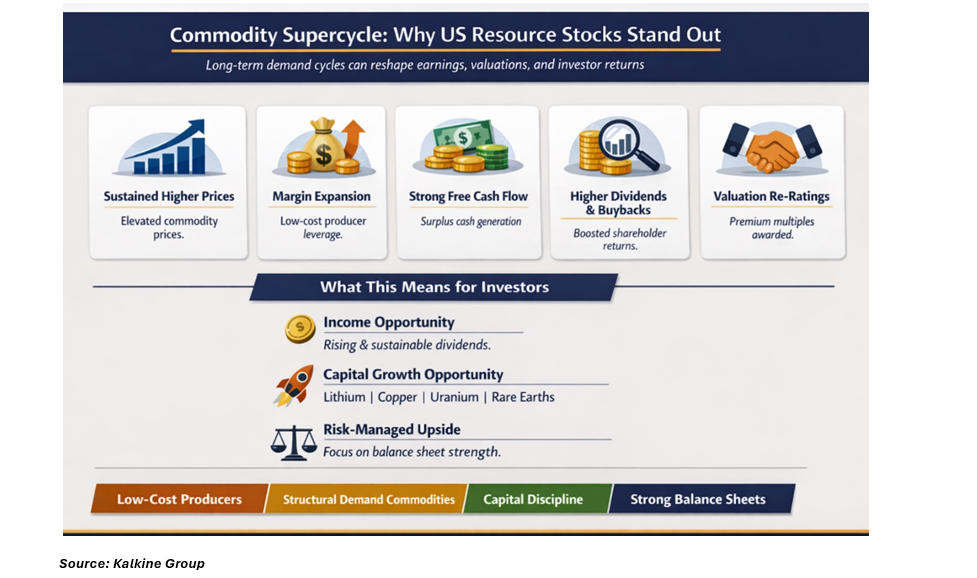

Why This Matters for US Commodity Stocks?

The US equity market is uniquely exposed to commodities. It hosts a large number of globally significant miners, ranging from diversified giants to emerging developers.

Key Commodity Groups and Beneficiaries

Notable US Commodity Players, and Annual % Returns (as on 12 Jan 2026)

- Energy Transition Metals: Copper, Lithium, and Critical Minerals

Energy transition metals remain central to electrification, grid expansion, EV manufacturing, and renewable infrastructure growth in the US.

Selected US-listed players and annual performance:

- Freeport-McMoRan (NYSE:FCX) — Priced at USD 58.71, up 48.97% in the past one year

- Southern Copper (NYSE:SCCO) — Priced at USD 176.00, up 92.50% in the past one year

- Albemarle Corporation (NYSE:ALB) — Priced at USD 169.33, up 85.04% in the past one year

Copper is often described as the “backbone of the energy transition,” given its essential role in power grids, electric vehicles, data centres, and renewable energy systems.

- Bulk Commodities — Still Relevant

While bulk commodities may not lead the next supercycle, they remain essential for infrastructure development and industrial production.

Drivers:

Infrastructure investment, reshoring of manufacturing, disciplined supply growth.

Key commodities:

- Iron ore

- Metallurgical coal

Major US-listed producers and indicative annual returns as on 12 Jan 2026:

- Cleveland-Cliffs (NYSE:CLF) — Iron ore and steel — Priced at USD 12.91, up 23.07% in the past one year

- United States Steel (NYSE:X) — Integrated steel producer — Priced at USD 48.30, up 55.10% in the past one year

- Peabody Energy (NYSE:BTU) — Metallurgical coal exposure — Priced at USD 34.15, up 81.46% in the past one year

Although demand growth may be slower than in previous cycles, supply constraints and capital discipline could support structurally higher prices relative to historical norms.

- Energy: Oil, Gas, and Uranium

Despite the global shift toward renewables, traditional energy sources remain critical to US energy security.

Drivers:

Underinvestment, geopolitical risk, LNG export growth, nuclear power revival.

US-listed exposure and annual returns as on 12 Jan 2026:

- Exxon Mobil (NYSE:XOM) — Global oil and gas — Priced at USD 124.03, up 13.49% in the past one year

- Chevron (NYSE:CVX) — Integrated energy major — Priced at USD 162.34, up 4.50% in the past one year

- Cameco Corp. (NYSE:CCJ) — Uranium producer — Priced at USD 109.79, up 124.98% in the past one year

- Energy Fuels (NYSE:UUUU) — Uranium and rare earths — Priced at USD 19.26, down 267.56% in the past one year

Uranium increasingly stands out as a structural commodity, supported by renewed nuclear investment and domestic fuel supply initiatives.

- Gold and Precious Metals

Gold plays a distinct role during late-cycle and macro-uncertain environments.

Drivers:

Inflation hedging, central bank buying, fiscal deficits, geopolitical uncertainty.

US-listed gold names and yearly returns as on Jan 12 2026:

- Newmont Corporation (NYSE:NEM) — Priced at USD 112.96, up 188.38%% in the past one year

- Barrick Gold (NYSE:GOLD) — Priced at USD 42.83, up 54.45% in the past one year

- Franco-Nevada (NYSE:FNV) — Priced at USD 230.89, up 85.71% in the past one year

Gold often performs best during periods of financial stress, providing diversification when cyclical commodities become volatile.

Who Benefits Most During a Commodity Supercycle?

Not all commodity producers benefit equally. Historically, stronger performers tend to share:

- Low-cost production profiles

- Long-life, high-quality assets

- Strong balance sheets

- Operational scale and pricing leverage

Large-cap miners typically offer stability, while mid- and smaller-cap companies may deliver higher volatility and larger percentage moves.

Risks to Watch

Even in a commodity supercycle, risks remain. A sharper global slowdown could weaken demand, while technological substitution may alter long-term commodity usage. Regulatory intervention, rising royalties, cost inflation, and permitting delays—particularly in the US—can pressure margins and project timelines.

In Conclusion

If a commodity supercycle continues through 2026 and beyond:

- US-listed resource stocks remain strategically positioned

- Energy transition metals—especially copper and lithium—are likely leaders

- Quality assets, cost discipline, and asset longevity remain key differentiators

For long-term market participants, commodities may again represent not just a cyclical exposure, but a strategic allocation amid evolving energy and infrastructure dynamics.

Please wait processing your request...

Please wait processing your request...