Image Source : Krish Capital Pty Ltd

Index Update: The S&P 500 edged higher as investors awaited Nvidia’s earnings, viewed as a key test for the AI-fueled rally. The Nasdaq rose 0.1% and the Dow added 135 points, while Nvidia shares were steady despite expectations of major volatility and strong year-over-year growth. AI optimism lifted MongoDB (+36%) and Okta (+3%) after strong results, while Cracker Barrel jumped 7% after reversing a controversial logo change. US stock futures fell after Nvidia dropped about 3% post-earnings despite beating forecasts, as data center sales lagged and H20 chip sales to China were absent from guidance. The decline weighed on other chipmakers, though analysts maintained a positive outlook for AI. Meanwhile, major indexes closed higher in the previous session, with the S&P 500 hitting a record.

Market Movers: On Wednesday, the top gainers were Sharps Technology Inc (+52.52%), followed by MongoDB, Inc. (+37.96%). On the contrary Super X AI Technology Limited. (-31.67%), and Nukkleus Inc (-25.34%) declined the most the same day.

Commodities Update: WTI and Brent crude futures slipped, erasing prior gains as traders weighed slowing U.S. fuel demand with the summer driving season ending, despite a larger-than-expected drop in U.S. crude stockpiles and Cushing inventories. Pressure from U.S. tariffs on India and its continued Russian oil imports kept supply risks in focus, while losses were partially offset by Russia-Ukraine attacks on energy infrastructure and optimism over potential U.S. rate cuts.

Gold edged higher near record levels, supported by political uncertainty after President Trump moved to dismiss a Fed governor and growing expectations of a September rate cut, now priced at 89%. Strong Asian demand, particularly from China, added further support as investors awaited fresh Fed signals and inflation data.

Macro Updates: Dollar Steadies as Rate Cut Bets Rise

The dollar index hovered near 98.1 after surrendering earlier gains, as markets priced in an 89% chance of a September Fed rate cut amid dovish signals from policymakers and political pressure from President Trump. Investors now await PCE inflation data for policy cues, while the dollar eased against the euro despite political uncertainty in France.

Bonds Commentary: The 10-year US Treasury yield fell to a two-week low below 4.23% as expectations for a September Fed rate cut rose to 89%. Sentiment turned more dovish after President Trump moved to replace a Fed governor and officials signaled cuts were under consideration. Markets now await the PCE inflation data and upcoming payrolls report for further guidance.

Futures Update: U.S. stock index futures traded mostly higher, with the tech sector lagging following Nvidia’s earnings. Dow futures showed modest gains, S&P 500 futures inched higher, while Nasdaq futures slipped slightly. Major indices recently closed higher, with the S&P 500 reaching a record level. All three benchmarks are on track for monthly gains, with the Dow leading, followed by the S&P 500 and Nasdaq.

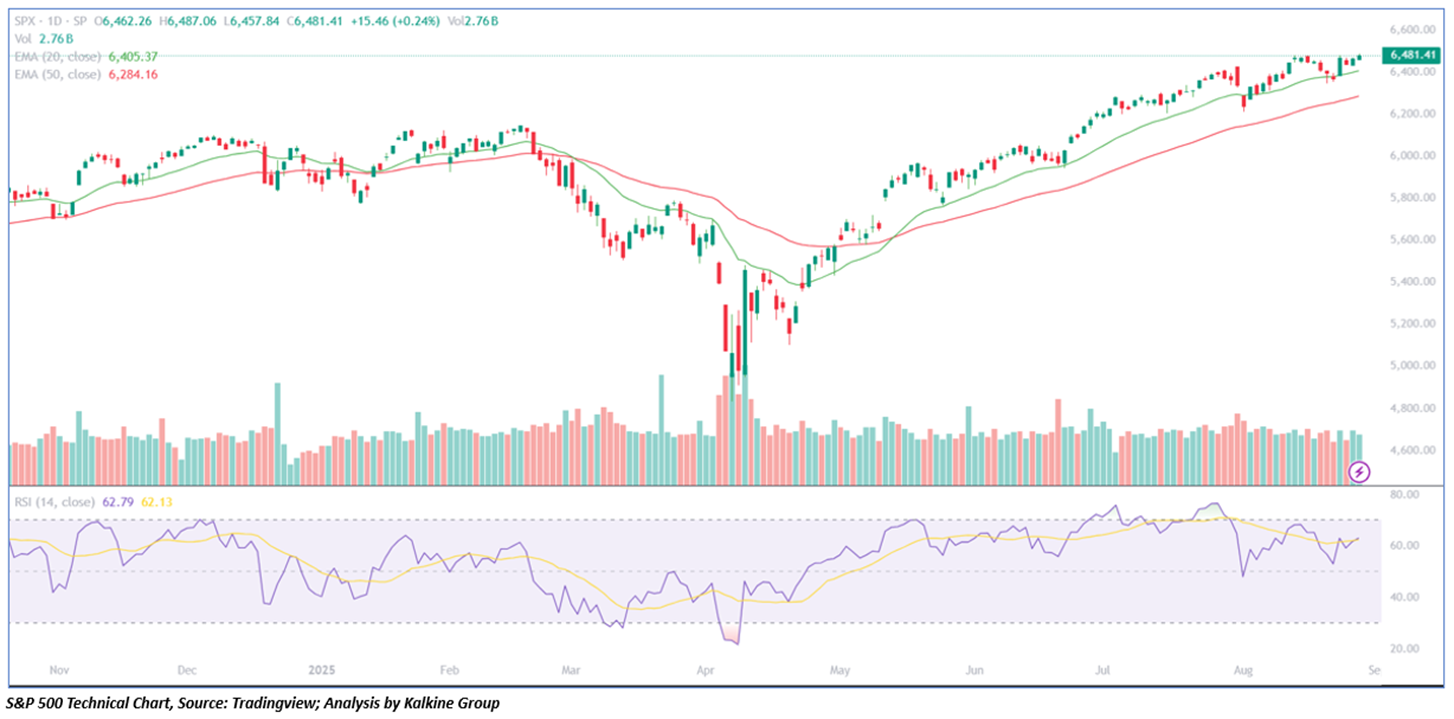

Following yesterday’s primarily upward but choppy trading session, stocks experienced further gains on Wednesday. The S&P 500 rose by 15.46 points, or 0.24%, closing at 6,481.41. From a technical standpoint, the index found support at the 21-period simple moving average and remains above this level, indicating the potential for additional upward movement in the near term. Additionally, the 14-day RSI bounced off the midpoint, suggesting a possible bullish bias. Key support levels are around 6,366, with resistance expected near 6,555.

Please wait processing your request...

Please wait processing your request...