Key Highlights

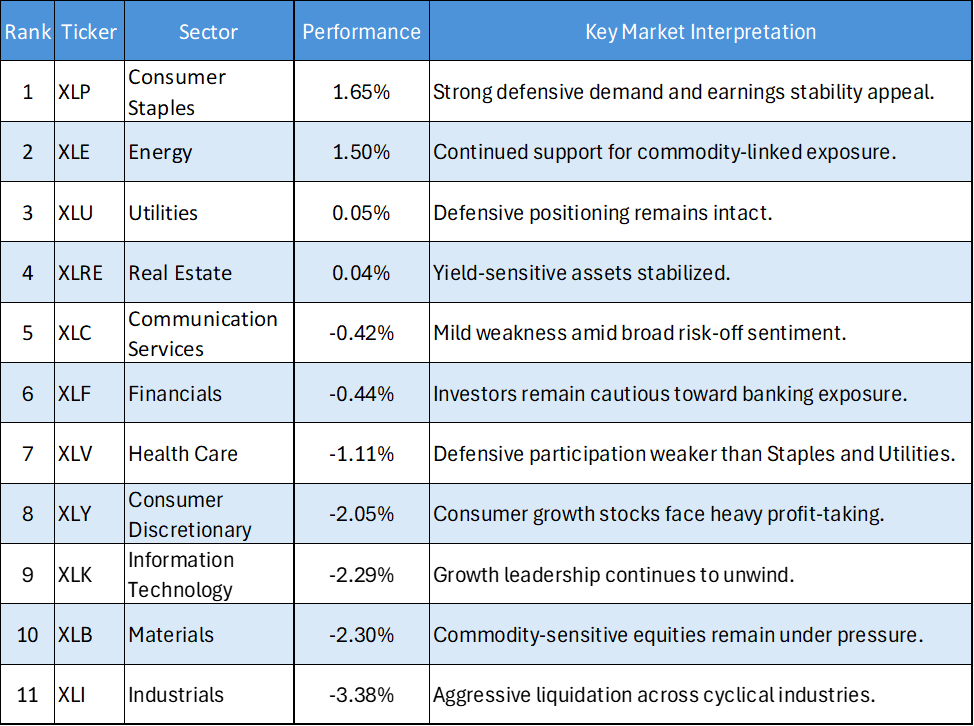

- Consumer Staples Leads Defensive Advance: Consumer Staples (XLP) gained 1.65%, emerging as the strongest-performing sector as investors sought stability amid broad market weakness. The strong inflow into staple-related equities suggests institutional capital is increasingly favoring defensive earnings visibility.

- Energy Remains a Relative Bright Spot: Energy (XLE) advanced 1.50%, outperforming all cyclical sectors except Consumer Staples. The sector’s resilience indicates continued investor interest in commodity-linked assets despite deteriorating risk sentiment across the broader market.

- Industrials Experience Significant Liquidation: Industrials (XLI) fell 3.38%, making it the weakest-performing sector of the session. The sharp decline highlights aggressive de-risking activity within economically sensitive industries as investors reduced exposure to growth-dependent segments.

- Technology and Consumer Discretionary Under Pressure: Information Technology (XLK) declined 2.29%, while Consumer Discretionary (XLY) lost 2.05%. The synchronized weakness across major growth sectors reflects a broad retreat from higher-beta assets and declining investor appetite for risk.

The US equity market session on June 10, 2026, was characterized by a pronounced defensive rotation as investors shifted capital away from growth-oriented and cyclical sectors. Unlike previous sessions that saw selective buying in Technology and Consumer Discretionary stocks, market participants increasingly favored defensive industries offering stable cash flows and lower earnings volatility.

The session displayed a clear divergence between defensive and economically sensitive sectors. Consumer Staples and Energy attracted positive inflows, while Industrials, Materials, Technology, and Consumer Discretionary sectors experienced substantial selling pressure. This pattern suggests institutional investors are adopting a more cautious stance amid growing uncertainty surrounding the near-term economic outlook.

Daily US Sector Performance Summary

Key Market Themes

Defensive Sectors Reclaim Leadership

- The defining characteristic of the session was the strong outperformance of defensive sectors. Consumer Staples (XLP) posted the largest gain among all sectors, while Utilities (XLU) and Real Estate (XLRE) managed to remain positive despite broad market weakness.

- The rotation into traditionally defensive assets suggests institutional investors are prioritizing capital preservation and earnings consistency. Such behavior is often observed during periods of elevated uncertainty when market participants seek to reduce portfolio volatility.

Technology Continues to Lose Momentum

- Information Technology (XLK) declined 2.29%, extending recent weakness and marking one of the largest sector declines of the session. The pullback indicates that investors remain reluctant to increase exposure to higher-duration growth assets.

- The weakness in Technology occurred alongside declines in Communication Services (XLC) and Consumer Discretionary (XLY), highlighting a broader reduction in growth-oriented positioning rather than sector-specific concerns.

Industrials and Materials Lead Cyclical Weakness

- Industrials (XLI) suffered the sharpest decline of the session, falling 3.38%, while Materials (XLB) lost 2.30%. The magnitude of these declines suggests institutional investors are becoming increasingly cautious toward sectors that are heavily dependent on economic expansion.

- The broad-based weakness across cyclical industries may indicate concerns regarding future demand growth, particularly as investors reassess expectations for economic activity and corporate earnings.

Energy Demonstrates Relative Strength

- Energy (XLE) stood out as one of the few sectors posting meaningful gains, rising 1.50%. The sector’s resilience suggests that investors continue to find value in commodity-linked assets despite the broader risk-off environment.

- Unlike Materials, which remained under pressure, Energy attracted selective inflows, indicating investors currently prefer targeted exposure to energy markets rather than broad commodity-related investments.

Financials Remain Directionless

- Financials (XLF) declined 0.44%, outperforming many cyclical sectors but still remaining in negative territory. The relatively modest decline suggests investors are maintaining a neutral stance toward the sector.

- While selling pressure was less severe than in Industrials and Technology, the inability of Financials to participate in defensive leadership indicates institutional conviction remains limited.

Bottom Line

The June 10 session highlighted a significant defensive rotation across US equity markets. Consumer Staples (XLP) and Energy (XLE) emerged as the primary beneficiaries of investor capital flows, while Technology (XLK), Materials (XLB), Consumer Discretionary (XLY), and Industrials (XLI) experienced substantial selling pressure.

The market's leadership structure now appears increasingly defensive, reflecting a more cautious institutional outlook. While Energy continues to attract selective buying interest, the broad weakness across growth and cyclical sectors suggests investors remain focused on risk management rather than aggressive risk-taking.

Going forward, defensive sectors such as Consumer Staples (XLP), Utilities (XLU), and Real Estate (XLRE) may continue to benefit if market uncertainty persists, while Technology (XLK) and Industrials (XLI) will likely require renewed institutional sponsorship before regaining leadership status.

Please wait processing your request...

Please wait processing your request...