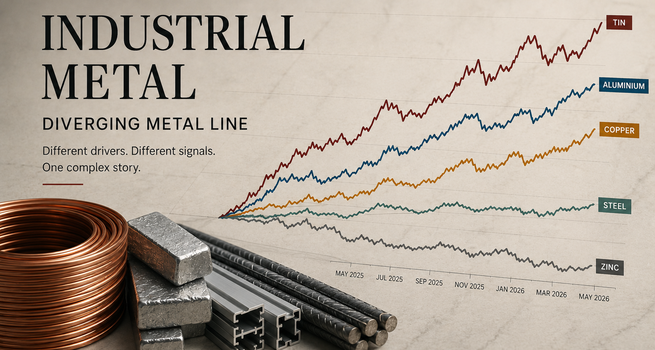

Industrial metals are telling sharply different stories in 2026. Tin has surged 64% over the past twelve months while steel barely moved. Copper holds near cycle highs, aluminum absorbs a geopolitical Supply shock, and zinc tracks the Credit cycle in real time. Here is what the divergence means

Key Highlights

- Tin has gained 64.47% over the past twelve months, the strongest performer in the industrial metals complex, driven by semiconductor supply tightness.

- Copper is up 35.78% over the same period but faces aggressive two-way Volatility from diverging U.S. and Chinese monetary conditions.

- Aluminum has risen 47.88%, with Gulf supply disruption entrenching a structural price premium that will not quickly unwind.

- Zinc is down on the week despite a 30.17% annual gain, offering a real-time read on construction sector and credit cycle stress.

- Steel's 2.06% annual gain is the single most direct measure of China's property and industrial Demand problem.

A Complex No Longer Moving Together

Industrial metals have historically functioned as a unified proxy for global growth. In 2026, that relationship has broken down. The spread between tin's 64.47% gain over the past twelve months and steel's 2.06% is not noise. It is the physical economy communicating in disaggregated form, with each metal responding to a distinct combination of supply constraints, demand conditions, and Monetary Policy transmission. Treating the complex as a single indicator now produces more confusion than clarity.

Copper: Structurally Supported, Cyclically Trapped

At $6.31 per pound, copper has gained 35.78% over the past twelve months and sits near historically elevated levels, though well below the cycle peak it briefly approached. The long-term demand case remains intact across grid infrastructure, electric vehicle deployment, and AI Data Center construction. Mine supply is structurally constrained following disruptions across major operations in Indonesia, the Democratic Republic of Congo, and Chile, none of which will normalize in the near term.

The cyclical problem is monetary divergence. U.S. Treasury yields climbing toward multi-decade highs are strengthening the dollar and prompting periodic Liquidation of long positions. Chinese government bond yields hovering near historic lows simultaneously signal that domestic Manufacturing and property sector activity cannot provide the physical demand intensity required to sustain a breakout. Physical inventories remain heavily concentrated in U.S. warehouses following Tariff-driven stockpiling, limiting availability to the broader global market. Copper is rangebound by design rather than by accident, and a sustained move higher requires both conditions to shift.

Aluminum: Geopolitical Floor, Demand Ceiling

Aluminum's 47.88% gain over the past twelve months is the most geopolitically driven return in the complex. Roughly 9% of global supply originates from Gulf producers that have been unable to export beyond the region, and the structural reality of smelter restarts means this supply shock will unwind gradually rather than abruptly. Even if conditions normalize, the recovery will be phased, not immediate.

The demand side offers no compensating momentum. European and North American consumption across construction, packaging, and transportation remains subdued. Aluminum is expensive for structural reasons, but those reasons do not automatically translate into further appreciation without a demand recovery that is not currently visible in the data.

The Construction Signal: Zinc and Steel Expose the Credit Cycle

Zinc's short-term weakness is the most analytically direct signal in the current data. Despite a 30.17% gain over the past year, the metal is down 1.13% on the day and 1.76% on the week. More than half of global zinc consumption flows into galvanized steel for construction applications, making it the sector most directly exposed to elevated interest rates and tightening credit conditions.

Zinc does not require interpretation. Its price weakness is the credit cycle expressing itself through the physical economy. Investors tracking the transmission of monetary tightening into real economic activity will find more signal in zinc's weekly price action than in most macroeconomic data releases.

Steel's 2.06% annual gain tells the same story from a different angle. Where zinc reflects the cost of credit tightening on construction demand broadly, steel's near-flat performance over twelve months points directly at China's property sector, where Investment is projected to decline by 12.8% in 2026 and real estate activity shows no credible recovery timeline. Together, the two metals offer the clearest available read on where the global construction and industrial cycle actually stands.

Tin: The Strongest Signal Nobody Is Discussing

Tin's 64.47% gain over the past twelve months is the most underreported performance in the complex. At $54,034 per ton, the metal also posted a 4.69% single-session gain, a move difficult to attribute to macro fund flows given tin's limited speculative participation relative to copper or aluminum.

The driver is physical. Tin is an essential soldering material in semiconductor manufacturing and printed circuit board production. Supply has remained structurally tight while demand from electronics manufacturing and industrial automation has recovered with more durability than the broader industrial sentiment narrative suggests. Tin's outperformance is a corrective to prevailing pessimism about global industrial demand. Genuine physical tightness exists in pockets, and tin is currently the clearest evidence.

What the Divergence Signals

The 62-percentage-point spread between tin and steel's performance over the past year is the industrial metals complex communicating something precise. Copper reflects macro uncertainty held in suspension. Aluminum reflects geopolitical supply risk with a slow recovery profile. Zinc reflects credit cycle stress in the real economy. Tin reflects genuine physical demand strength in high-value manufacturing.

Together, they describe a global economy that is neither in broad expansion nor broad contraction, but fracturing along sectoral and geographic lines that aggregate growth indicators are too blunt to capture.

_06_25_2026_01_47_16_943609.jpg)

_06_25_2026_01_48_12_180710.jpg)

_06_25_2026_01_49_10_600130.jpg)

Please wait processing your request...

Please wait processing your request...