An equity research deep-dive on Eli Lilly (NYSE:LLY), anchored on the April 24, 2026 close. The most dominant pharma franchise of the decade is now learning what it costs to be the most-watched ticker in healthcare.

Key Highlights

- Eli Lilly’s valuation reflects premium growth expectations driven by GLP-1 franchise dominance and pipeline depth.

- Manufacturing capacity constraints remain a key limiter of near-term revenue realization.

- Competitive pressure and pricing dynamics introduce medium-term risk to earnings sustainability.

Eli Lilly (NYSE:LLY) is one of the most strategically transformed large-cap pharmaceutical companies of the modern era. Over the past several years, it has gone from a diversified pharma with steady but unspectacular growth into the dominant Western operator in the GLP-1 metabolic franchise via Mounjaro and Zepbound (tirzepatide), with a deep and steadily advancing pipeline across obesity, diabetes, Alzheimer's, oncology, and immunology.

By 2026, the equity story is shaped by three forces. First, the GLP-1 franchise has become a structural blockbuster, redefining the addressable market for cardiometabolic disease. Second, the next-generation pipeline — including oral GLP-1 candidates, multi-incretin combinations, and next-wave Alzheimer's therapeutics — is one of the most-watched in the industry. Third, the supply, manufacturing, and access dynamics around GLP-1 have become a story unto themselves, defining quarterly revenue translation in ways that make the headline number more variable than the underlying demand picture.

Stock Performance in 2026 (YTD)

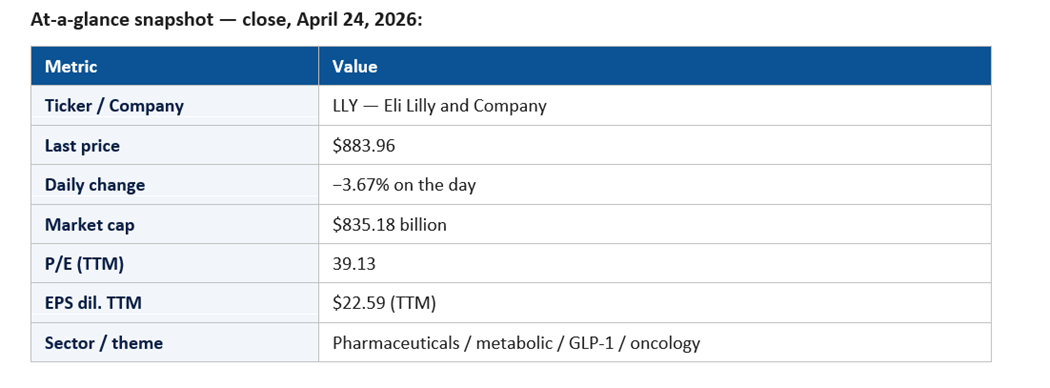

LLY closed April 24, 2026 at $883.96, down 3.67% on a session in which the broader market rose. The market capitalization of $835.18 billion ranks LLY as the largest pharma in the index by a wide margin. The trailing P/E of 39.13 on $22.59 of TTM diluted EPS is rich versus the broader pharma cohort and reflects continued investor willingness to pay for GLP-1 dominance and pipeline depth.

The implied YTD posture has been one of high-quality drug-name volatility. LLY is the kind of stock that responds sharply to specific data, label, manufacturing, or competitive announcements, and 2026 has had no shortage of any of them. The −3.67% session is exactly the kind of single-day reset that has punctuated an otherwise constructive longer-arc trajectory.

The most important structural fact about LLY in 2026 is the residual scarcity premium. Even after years of capacity build-out, the company's manufacturing throughput remains a binding constraint on revenue translation, and any data point on capacity changes the stock's near-term path.

Key Price Movements and Milestones

Three milestones define the 2026 tape. First, the consolidation around the $850–$900 zone, with previous highs in the $1,000-plus range establishing a wide trading band. Second, the persistent investor focus on competitive entrants in obesity, particularly the maturation of Novo Nordisk's next-generation candidates and emerging oral and small-molecule programs.

Third, the manufacturing capacity story has moved through several discrete updates. Each disclosure of new facility activation, expansion timing, or third-party fill-finish capacity has shifted the perceived revenue trajectory. The −3.67% session is consistent with a market that responds aggressively to news that complicates the supply-and-share narrative.

Major Catalysts: Why the Stock Moved

The dominant 2026 catalyst is the GLP-1 franchise itself: revenue trajectory, label expansion (cardiovascular benefit, sleep apnea, kidney, MASH-adjacent indications), and access dynamics with payers and PBMs. Each disclosure that broadens the labeled use cases supports the multiple; each disclosure that complicates pricing or access pressures it.

The second catalyst is competition. The pace at which Novo Nordisk's next-gen products advance, plus the readouts from emerging programs at other large pharmas and biotechs, function as discrete sentiment events. The market in 2026 has matured past the simple 'Lilly versus Novo' dichotomy into a more nuanced view of a multi-product, multi-mechanism category.

The third catalyst is the next-generation oral GLP-1 program (orforglipron) and broader pipeline progression. Each readout — whether efficacy, tolerability, or cardiovascular benefit data — is a meaningful narrative event.

The fourth catalyst is Alzheimer's: the donanemab (Kisunla) commercial trajectory, label dynamics, infusion-center access, and competitive positioning versus Eisai/Biogen's lecanemab. The Alzheimer's story is smaller in immediate revenue impact than the metabolic franchise but is strategically meaningful.

Macro and Fed-rate sensitivity is moderate — pharma is duration-sensitive, but Lilly's growth profile and earnings resilience have made it relatively resistant to rate-driven multiple compression. Geopolitics matter primarily through international pricing and access frameworks.

Sector Trends Influencing the Stock

Three sector trends underwrite the 2026 thesis. First, the GLP-1 category is still in early innings of its global penetration into eligible patient populations, with cardiovascular outcomes data and broader insurance coverage continuing to expand the practical addressable market.

Second, the global obesity and metabolic-disease epidemiology has become an explicit health-system priority in many countries, which is shifting policy and reimbursement dynamics in ways that broadly favor the category leaders.

Third, pharma manufacturing — particularly biologic and peptide manufacturing — has become a strategic capability in its own right. Investors increasingly view manufacturing capacity as a competitive moat rather than a back-office function.

Competitive Positioning

Lilly's competitive position in obesity and diabetes is best described as co-leadership with Novo Nordisk, with Lilly currently holding the more attractive in-market product on tolerability and weight-loss efficacy in many head-to-head comparisons. The competitive dynamic in 2026 has shifted from a pure first-mover advantage to a contest of innovation cadence: who has the best oral, who has the best multi-incretin combination, who has the best cardiovascular and kidney outcomes evidence.

Beyond the metabolic franchise, Lilly's pipeline depth — across oncology (Verzenio, KRAS programs), immunology, and Alzheimer's — provides a layer of optionality that few peers can match. Some of those programs are far enough out that they do not anchor the 2026 multiple, but they reduce the long-tail risk of franchise decay.

Outside the headline names, smaller competitors with novel mechanisms (oral small molecules, amylin analogs, dual or triple agonists) are slowly moving up the field. The competitive landscape in 2027–2028 will look different from 2026, and the market is starting to price that.

Financial Highlights

TTM diluted EPS of $22.59 against a $883.96 share price gives Lilly a P/E of 39.13. Operating margin has continued to expand as the GLP-1 franchise scales, and gross margin remains strong despite the manufacturing investment cycle.

Capital deployment has been weighted toward manufacturing capacity and R&D, with capital return secondary. Free cash flow has compounded as the GLP-1 franchise has matured, providing the funding base for further capacity investment without straining the balance sheet.

The disclosure cadence around segment economics — particularly Mounjaro/Zepbound revenue, gross margin, and supply-driven volatility — has become the most-watched part of each quarterly print.

Key Risks and Challenges

The first risk is competition. Novo Nordisk and a long list of emerging programs collectively represent meaningful share-loss risk over the coming several years. While the category itself is still growing, market-share dynamics could compress Lilly's long-run revenue.

The second risk is pricing and access. Public-payer and PBM dynamics around GLP-1 pricing have been a structural negotiating frontier, and any meaningful step-change in access or rebating would compress the franchise economics.

The third risk is manufacturing. Capacity execution has been Lilly's largest operational challenge in this cycle; any setback at a major facility, fill-finish partner, or raw-material supplier would create immediate revenue impact.

The fourth risk is regulatory and label-related. Adverse label changes, label-restriction outcomes, or unexpected post-marketing safety signals would be material narrative events.

Finally, valuation gravity is real. At a multiple in the high 30s, the stock is priced for continued execution; any meaningful disappointment compresses the multiple before fundamentals catch up.

Institutional and Investor Sentiment

Institutional positioning in Lilly remains overweight in healthcare and growth mandates. The combination of the GLP-1 franchise, the pipeline, and the demonstrated execution track record has made LLY a near-must-own pharma name. Sell-side coverage is constructive on average, with the disagreement primarily focused on long-run franchise share.

The options market reflects a nervous-but-engaged posture: implied volatility into earnings has been elevated, skew on downside puts is meaningful, and the −3.67% session is a reminder of how aggressively the tape can react to news that disrupts the bull setup.

Signals to Watch in the Coming Quarters

Five concrete signals will define how the Lilly narrative evolves through the rest of 2026. The first is Mounjaro and Zepbound revenue trajectory. The market wants visible evidence that supply continues to expand faster than competitive share losses, with disclosed unit volumes, price/mix dynamics, and any commentary on net-realized pricing versus list pricing.

The second signal is manufacturing capacity activation. Each new facility coming online, each meaningful expansion in fill-finish capacity, and each successful technology transfer to a new line is a discrete revenue-translation event. The most-watched line in each quarterly disclosure is supply-versus-demand commentary.

The third signal is oral GLP-1 (orforglipron) clinical and commercial readouts. Efficacy, tolerability, and especially cardiovascular and kidney outcomes data will collectively determine the long-run franchise positioning. A clean efficacy and safety profile would be a major narrative event; a complicated profile would invite competitive reframing.

The fourth signal is donanemab (Kisunla) commercial trajectory in Alzheimer's. Infusion-center capacity, payer access, real-world tolerability data, and competitive positioning versus lecanemab will collectively determine whether the franchise scales into the substantial commercial opportunity many investors believe is achievable.

The fifth signal is pipeline events outside the metabolic franchise. Oncology readouts (KRAS programs, Verzenio expansion), immunology progress, and any next-generation Alzheimer's data collectively manage the long-term franchise concentration risk that surrounds the GLP-1 dependence. Each non-GLP-1 win reduces the multi-year risk premium investors apply to the multiple.

Outlook for the Rest of 2026

The base case is continuation: GLP-1 revenue compounds, manufacturing capacity expands, label development continues, and the next-generation oral and combination programs deliver supportive readouts. In that scenario, the multiple defends itself and the stock can grind higher over time, with the kind of single-day pullbacks captured in the April 24 print serving as buying opportunities for long-horizon holders.

The bull case is a step-change in oral GLP-1 efficacy/safety data plus continued cardiovascular and kidney outcomes data. The bear case is a meaningful share gain by Novo or by an emerging entrant, combined with payer-access pressure and a manufacturing setback. That combination is the symmetric risk to the equity story.

Lilly in 2026 is the most dominant pharma franchise of the decade — and a reminder that even dominant franchises trade with the gravity of their own expectations.

For now, the −3.67% session is the price of leadership. Big franchises do not get to have small reactions to small news. The question is whether the underlying demand and pipeline keep proving the bulls right between the volatile sessions.

Please wait processing your request...

Please wait processing your request...