An equity research deep-dive on Visa Inc. (NYSE:V), anchored on the April 24, 2026 close. The most boring-looking trillion-dollar-class business in the index has spent 2026 doing the most reliable thing in finance — collecting on every transaction.

Key Highlights

- Visa’s valuation reflects a high-quality compounding business driven by global payment volume growth and cross-border expansion.

- Strong operating margins and free cash flow support consistent capital return.

- Structural shift toward digital payments continues to underpin long-term growth outlook.

Visa (NYSE:V) is a global payments-technology company that operates the largest and most-connected card-payment network in the world. The business sits between issuers (banks and fintechs that provide cards), acquirers (banks and processors that serve merchants), and the merchants themselves, taking a small but recurring fee on each transaction. Beyond the core network, Visa has expanded into adjacent value-added services — risk and identity, issuing solutions, acceptance solutions — and into newer payment flows such as B2B, peer-to-peer, and cross-border money movement.

By 2026, Visa is best understood as the toll booth of the consumer internet and a meaningful portion of the global B2B economy. Its franchise is built on scale, brand, security, and trust; its growth is built on digital substitution of cash, expansion of payment volume across geographies, and monetization of new flow categories. The simplicity of the model belies one of the highest-margin, lowest-incremental-cost businesses in the public market.

Stock Performance in 2026 (YTD)

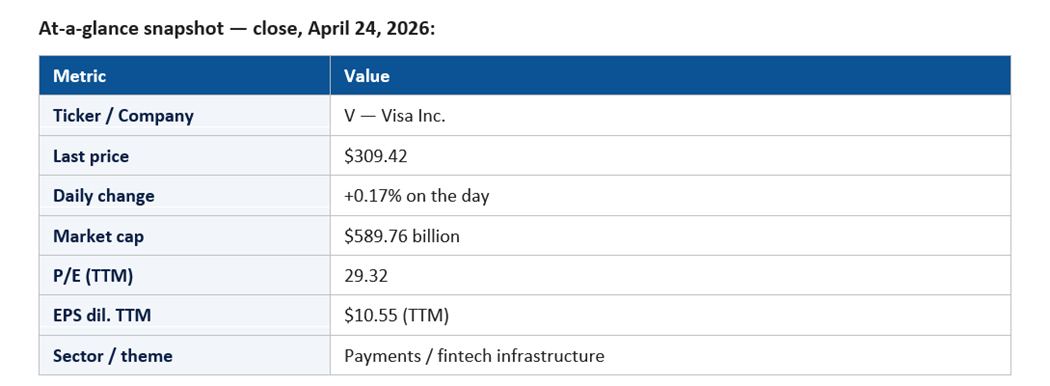

V closed April 24, 2026 at $309.42, up 0.17% on the day, with a market capitalization of $589.76 billion. The trailing P/E of 29.32 on $10.55 of TTM diluted EPS reflects a stable, high-quality compounder with a defensible multiple. The implied YTD posture is one of measured grinding higher — Visa has historically traded in line with consumer spending durability, and 2026 has been broadly constructive on that front.

On the April 24 session, Visa's near-flat close on a chip-led tape is consistent with a stock that does not lead AI-rally days but holds its ground. That defensiveness is a feature, not a bug: portfolio managers carry V because of its predictability, not its beta.

Key Price Movements and Milestones

Three milestones define the 2026 tape. First, the persistent defense of the $300-plus zone, with the breakthrough above $300 functioning as both a psychological event and a technical inflection. Second, the relationship between V and consumer-facing cyclicals has tightened — Visa has tracked credit-card spend volumes and travel data closely, with the implied earnings model very sensitive to international travel and cross-border activity.

Third, the disclosure cadence around incentives — the contra-revenue paid to issuers and acquirers — has been a recurring narrative variable, with each quarter's incentive ratio shaping the operating margin trajectory.

Major Catalysts: Why the Stock Moved

The dominant 2026 catalyst is global payment volume. Each quarterly disclosure of payment volume, processed transactions, and cross-border volume is a discrete catalyst. Cross-border, in particular, has continued to be a high-margin growth engine as international travel and global e-commerce expand.

The second catalyst is value-added services. Risk products, identity, issuing technology, and acceptance services have grown into a meaningful and high-margin layer of the consolidated story. Each quarter that demonstrates VAS revenue accelerating supports the multiple.

The third catalyst is new flows. Visa Direct, B2B, and other money-movement initiatives have continued to add revenue and strategic optionality, with each disclosure of partner integration or volume milestone shifting the long-run TAM perception.

The fourth catalyst is regulation. Interchange and network-fee scrutiny in multiple jurisdictions is a steady undercurrent rather than a single dramatic event, but each major regulatory development shifts the risk premium investors apply.

Macro and Fed-rate sensitivity is moderate; geopolitics matter primarily through cross-border travel patterns and through emerging-market FX dynamics.

Sector Trends Influencing the Stock

Three sector trends underwrite the 2026 thesis. First, cash-to-digital substitution has continued in essentially every geography, providing a structural growth driver that is independent of the macro cycle. Second, the cross-border digital economy — e-commerce, freelance platforms, B2B trade — continues to expand the addressable market for high-margin cross-border transactions.

Third, the broader fintech and payments landscape has consolidated, with the network operators (Visa, Mastercard) sitting at the center of a stable, profitable two-sided market. New payment rails — real-time payments, account-to-account, and emerging stablecoin-style infrastructure — are evolving variables, but the network model has proven remarkably resilient.

Competitive Positioning

Visa's competitive position in 2026 is best described as duopoly leadership with continued ecosystem expansion. Mastercard remains the principal direct competitor, with both firms benefiting from network scale, brand, and security. American Express occupies a closed-loop premium niche; Discover, JCB, UnionPay, and emerging real-time payment systems each operate in specific geographies or product slices without dislodging the global network model.

The most-watched competitive vector is alternative payment rails. Account-to-account systems, real-time payments, and stablecoin or tokenized-money systems have continued to evolve. Visa's strategy has been a combination of defending core economics, partnering with rail operators, and investing in adjacent capabilities. The competitive picture is more nuanced than the simple 'disruption' narrative — Visa has consistently demonstrated the ability to integrate with new rails rather than be displaced by them.

Financial Highlights

TTM diluted EPS of $10.55 on a $309.42 share price gives Visa a P/E of 29.32. Operating margin remains among the highest in the megacap universe, reflecting the network's structural cost advantage. Free cash flow conversion is strong, supporting an aggressive capital return program through buybacks and a steadily growing dividend.

Revenue is split across service revenue, data processing, international transaction revenue, and other revenue, with each category contributing meaningfully. International transaction revenue (cross-border) is the most volatile and the most-watched, given its sensitivity to travel and e-commerce dynamics.

Incentives — the contra-revenue paid to issuers and acquirers to drive volume — have continued to scale with the business, with the implied incentive ratio one of the most-watched line items in each quarterly disclosure.

Key Risks and Challenges

The first risk is regulatory. Network fees, interchange caps, antitrust scrutiny, and access mandates around alternative payment rails are all live regulatory issues in different jurisdictions. Any meaningful change in fee structure would compress segment economics.

The second risk is alternative rails. While Visa has demonstrated adaptability, a structural shift in consumer or merchant preferences toward non-network rails would compress long-term volume growth.

The third risk is consumer health. Visa's revenue is sensitive to discretionary and cross-border spending, and a sustained consumer slowdown — especially in international travel — would dampen revenue growth.

The fourth risk is FX. As a globally diversified network, Visa's revenue is exposed to currency translation, with non-USD strength a positive and weakness a negative.

Why Visa's Quiet Compounding Has Been the Trade Hiding in Plain Sight

The most unfashionable trade in 2026 has also been one of the most reliable: own the toll booth. While the AI complex has produced double-digit single-day moves and the chip cohort has dominated headlines, Visa has continued to do what it has always done — collect a small, recurring fee on a steadily growing share of global commerce. The lack of drama is the entire point. The stock's compounding profile is built on the slow, structural digitization of payments, not on any single quarter's catalyst.

What makes V specifically interesting in this regime is the disconnect between perceived risk and actual fragility. The bear narrative for Visa has been the same for a decade — alternative rails will disrupt the network, regulators will compress interchange, real-time payments will eat into core volume. None of those risks has materialized at scale. Instead, Visa has steadily integrated with new rails, expanded into value-added services, and grown cross-border at high incremental margin. The franchise is a study in adaptive incumbency.

The result is an equity that pays for portfolio composure. Investors who own Visa are not betting on any specific macro outcome; they are betting that global commerce continues, that the digital share of that commerce continues to grow, and that the network continues to take its small recurring slice. That is not a thesis that requires any particular news cycle to work — and that is precisely why it has worked through every news cycle of 2026.

Institutional and Investor Sentiment

Institutional positioning in Visa is broadly constructive. The combination of high-quality earnings, defensive growth, and attractive return on capital has made V a near-mandatory position in many large-cap-growth and core mandates. Sell-side coverage is positive on average, with bear cases focused on regulatory tail risk and on alternative rails.

The options market reflects a calm posture, with implied volatility behaving normally for a low-beta megacap. Visa is not the kind of stock that produces speculative intraday narratives.

Signals to Watch in the Coming Quarters

Six concrete signals will define how the Visa narrative evolves through the rest of 2026. The first is U.S. payment volume. As a proxy for U.S. consumer spend, the line is one of the most-watched real-time indicators of consumer health, and any meaningful deceleration would reshape the macro debate around discretionary spending.

The second signal is cross-border volume excluding intra-Europe. International travel, cross-border e-commerce, and global B2B transactions collectively drive this high-margin category. The pace of growth has been a defining variable; sustained double-digit growth supports the multiple, while any meaningful slowdown compresses it.

The third signal is the incentive ratio. The contra-revenue paid to issuers and acquirers determines how much volume growth converts to net revenue growth. A stable or improving incentive ratio is a constructive structural signal; an expanding ratio is a margin pressure that the market reads negatively.

The fourth signal is value-added services revenue. Each quarter the market wants visible double-digit growth in VAS, with commentary on cybersecurity, identity, issuing, and acceptance products. VAS is the principal mechanism by which Visa expands wallet share with existing partners beyond pure transaction processing.

The fifth signal is new flows and Visa Direct. Each disclosed integration, partnership, or volume milestone in B2B, P2P, or cross-border money movement adds a layer of long-run TAM expansion to the equity story.

The sixth signal is regulatory and competitive commentary on alternative rails. Any meaningful update on real-time payments, account-to-account systems, or stablecoin-style infrastructure will be parsed for implications on long-run network economics. The market expects steady evolution, not abrupt disruption.

Outlook for the Rest of 2026

The base case is continuation: payment volume compounds in the high single digits to low double digits; cross-border continues to recover and grow; value-added services accelerate; new flows add a modest but visible layer of growth; the buyback continues to absorb a meaningful share of float. In that scenario, Visa compounds earnings at a rate that supports the multiple and produces total returns in line with its long-run pattern.

The bull case is a structural acceleration in cross-border combined with stronger-than-expected VAS adoption. The bear case is a regulatory development that meaningfully changes interchange or network economics, paired with a consumer slowdown.

Visa in 2026 is the rare megacap whose competitive moat is the simple fact that, every minute of every day, more transactions move through its network than any plausible competitor could ever stand up.

For now, the +0.17% session is exactly the kind of low-volatility behavior that defines Visa. The trade is not about catalysts — it is about the steady, compounding right to a tiny slice of the global economy. That is what makes it a core position in 2026.

Please wait processing your request...

Please wait processing your request...