An equity research deep-dive on JPMorgan Chase (NYSE:JPM), anchored on the April 24, 2026 close. The largest U.S. bank has spent 2026 doing what it does best — turning macro uncertainty into a balance-sheet advantage.

Key Highlights

- JPMorgan’s valuation remains grounded at ~15x earnings, reflecting strong profitability and disciplined capital allocation.

- Net interest income and capital markets recovery are key drivers of earnings stability.

- Strong balance sheet and capital position provide resilience across macro cycles.

JPMorgan Chase (NYSE:JPM) is the largest and most diversified bank in the United States, with leadership positions across consumer and community banking, corporate and investment banking, asset and wealth management, and a massive global markets franchise. The bank serves more than 80 million U.S. consumers, multinational corporates across every region, sovereign and institutional asset owners, and a deep ecosystem of mid-market businesses through its commercial banking arm.

By 2026, the strategic frame is clear. JPM is the structurally advantaged operator of U.S. financial services, with a balance sheet that benefits from scale, a technology platform that sets industry pace on AI deployment, and a culture of conservative capital management that lets it act in moments of dislocation. The combination of size, capital strength, and disciplined risk management has compounded into a cost-of-capital advantage versus most peers, which shows up almost mechanically in return on equity.

Stock Performance in 2026 (YTD)

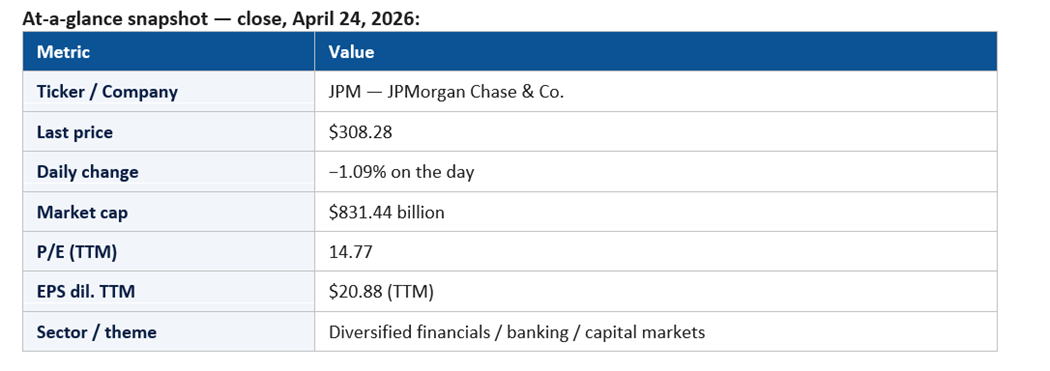

JPM closed April 24, 2026 at $308.28, down 1.09% on the day, with a market capitalization of $831.44 billion. The trailing P/E of 14.77 on $20.88 of TTM diluted EPS is among the most reasonable multiples in the megacap universe — a signature of high-quality cyclical earnings rather than narrative-driven multiple expansion.

The implied YTD posture is one of measured outperformance within a cyclical regime. JPM has benefited from constructive net-interest dynamics, a stronger investment banking environment than the prior two years, and stable consumer credit metrics. The −1.09% session is the kind of routine pullback that has framed the year — modest moves around a steadily compounding franchise.

Key Price Movements and Milestones

Three milestones define the 2026 tape. First, the persistent defense of the $300-plus zone. The break above $300 was a structurally important psychological event, and the subsequent consolidation has effectively turned the level into support.

Second, the relationship between JPM and the broader bank cohort has tightened. JPM has tended to lead financials on positive sessions and underperform less on weak ones — exactly the asymmetry investors expect from the franchise leader.

Third, the disclosure cadence around capital return — buybacks and dividends — has been a constructive narrative, with the bank continuing to operate well above regulatory capital requirements while methodically returning capital to shareholders.

Major Catalysts: Why the Stock Moved

The dominant 2026 catalyst is net interest income. The shape of the yield curve, the composition of deposits, and asset repricing dynamics collectively determine the run-rate of NII, and JPM's ability to manage all three has been a recurring strength. Each macro print that suggests rates remain higher for longer reinforces the NII story.

The second catalyst is investment banking and markets. After several softer years, the IB pipeline has reactivated, with M&A advisory, debt capital markets, and equity issuance all contributing. Markets revenue has continued to be a steady contributor, with rates and FX desks in particular benefiting from a more active macro tape.

The third catalyst is consumer credit. Card loss rates, mortgage origination, and consumer deposit dynamics have collectively held up better than the bear case, and JPM's underwriting quality has continued to show its edge in periods of stress.

The fourth catalyst is technology and AI. JPM's commitment to AI deployment in operations, customer service, and revenue-generating activities has been one of the more credible AI stories among the global banks. While not yet visible in segment-level revenue, it is increasingly visible in expense efficiency.

Macro and Fed-rate sensitivity is structural and asymmetric — JPM benefits from a steeper curve and from a higher-for-longer rate environment, but it is also resilient in scenarios where rates fall, due to the offset of stronger investment-banking activity.

Sector Trends Influencing the Stock

Three sector trends underwrite JPM's 2026 thesis. First, the U.S. banking landscape continues to consolidate around scale. Regulatory and capital requirements favor large operators, and JPM is the largest of them. Second, capital markets activity has reaccelerated, with strategic M&A, IPO issuance, and credit markets all running closer to long-term averages than prior years. Third, AI deployment in financial services is becoming a real cost-and-revenue lever, and JPM is one of a small number of operators with the budget and the talent to push it to scale.

Competitive Positioning

JPMorgan's competitive position in 2026 is one of structural primacy. In consumer banking, it is the dominant U.S. retail bank by deposits and branches. In investment banking, it competes at the top of the league tables in nearly every product. In asset and wealth management, it is one of the largest global operators, with a fast-growing alternatives platform.

The combination of scale, balance sheet, and brand creates a cost-of-capital and cost-of-funding advantage that is hard to dislodge. Competitors — Bank of America, Citigroup, Wells Fargo, Goldman Sachs, Morgan Stanley — each match JPM in specific product or geographic dimensions, but no single peer matches across all of them.

Financial Highlights

TTM diluted EPS of $20.88 on a $308.28 share price gives JPM a P/E of 14.77. Return on tangible common equity has continued to run at industry-leading levels, comfortably above the bank's stated through-the-cycle target.

Capital ratios remain meaningfully above regulatory minimums, providing both the cushion to weather adverse stress scenarios and the optionality to deploy capital opportunistically. The buyback continues to be a measurable source of EPS growth, with the dividend providing a steady income component.

Operating leverage — the gap between revenue and expense growth — has been broadly positive across the cycle, with technology investment running at a level that supports both near-term efficiency and longer-term competitive positioning.

Key Risks and Challenges

The first risk is the credit cycle. While consumer credit metrics have been resilient in 2026, a meaningful deterioration in unemployment or in commercial real estate could change the loss outlook quickly.

The second risk is regulatory. Capital requirements, particularly under any final implementation of more stringent Basel-style frameworks, could constrain capital return and require structural balance-sheet adjustment.

The third risk is geopolitical. JPM's global markets and corporate banking businesses are exposed to a wide range of cross-border dynamics, and any meaningful escalation — trade, sanctions, conflict — would create both revenue volatility and risk-management complexity.

The fourth risk is the rate path. If the curve steepens dramatically or flattens unexpectedly, NII trajectory could shift in ways that the consensus model has not fully captured.

Finally, key-person risk around the CEO, while less acute than at smaller firms, remains a recurring topic; the institution's culture is deeply tied to its leadership.

Why JPM Has Been the Bank Stock That Refuses to Get Boring

The cliché about megabanks is that scale produces stability and stability produces dull stocks. JPM in 2026 has been the rebuttal. The franchise's earnings power has compounded faster than the broader bank cohort, the multi-line revenue mix has buffered against any single-cycle pressure, and the technology and AI commentary has given growth-oriented investors a reason to engage with a name they would otherwise treat as a value-cyclical.

What makes JPM specifically interesting in this regime is the way the company manages its capital position. Excess capital is meaningful, but it is never deployed without explicit reasoning, and the bar for buybacks, dividend increases, and M&A continues to be visibly disciplined. That posture turns the balance sheet itself into a kind of strategic asset: ready to act in a dislocation, content to wait when prices are unattractive.

The result is an equity that performs the most underrated trick in capital markets: it consistently delivers above-cohort earnings power without committing investors to a specific macro thesis. Investors who own JPM do not need to be right about rates, the curve, the credit cycle, or the AI cycle to justify the position. They only need to be right that the franchise will keep doing what it has been doing for the past several decades — adapting, compounding, and managing through whatever environment shows up.

Institutional and Investor Sentiment

Institutional positioning in JPM in 2026 is broadly constructive. The bank is a near-mandatory holding in financials-overweight portfolios and a frequent inclusion in core mandates. Sell-side coverage is positive on average, with the bull case framed around continued ROE leadership and the bear case largely focused on credit-cycle and regulatory tail risks.

The options market reflects relatively calm pricing of upside and downside, consistent with a high-quality cyclical that does not require speculation to justify position size.

Signals to Watch in the Coming Quarters

Six concrete signals will define how the JPM narrative evolves through the rest of 2026. The first is the trajectory of net interest income relative to the consensus path. Each disclosure that the bank maintains or expands its NII run-rate — particularly through a period in which rate-cut expectations move around — supports the multiple. Any visible NII air pocket would be a meaningful narrative event.

The second signal is investment-banking pipeline conversion. Announced M&A backlog, debt and equity capital-markets calendars, and indicated deal-flow commentary all set the bar for the next two-to-three quarters of fee revenue. The pipeline has been more constructive than recent years; the market wants visible conversion.

The third signal is consumer credit. Credit-card net charge-offs, auto and mortgage delinquency trends, and reserve-build commentary collectively define the implied loss content of the loan book. JPM's underwriting has been a structural advantage; any meaningful uptick in stress would still be a market-wide read on the consumer.

The fourth signal is commercial real estate. The bank has navigated the CRE cycle with discipline, but each disclosure of office-property reserves, refinancing dynamics, or work-out activity is read closely as a proxy for the broader sector.

The fifth signal is capital ratios and capital return. The pace of buyback activity, dividend increases, and any commentary on the implementation of any final more-stringent capital framework determines how much excess capital is available to return.

The sixth signal is technology and AI deployment. Any visible commentary on AI-driven expense efficiency, customer-experience improvement, or revenue-generating use cases continues to differentiate JPM from peers and reinforces the operational-leadership narrative.

Outlook for the Rest of 2026

The base case is continuation: NII holds at a high level; investment-banking activity remains constructive; consumer credit normalizes without dislocating; expense discipline supports operating leverage; capital return continues at a measured pace. In that scenario, JPM compounds earnings at a rate that supports a slow, durable re-rating of the multiple.

The bull case is a clean acceleration in capital-markets activity plus a steeper curve, both of which would lift revenue and EPS above the consensus path. The bear case is a credit-cycle deterioration, particularly in commercial real estate or consumer card, that compresses ROE and forces a multiple reset.

JPMorgan in 2026 is the rare bank stock that does not require a macro thesis to outperform. It just requires the macro to behave normally — and the franchise does the rest.

For now, the −1.09% session is the kind of measured pullback that has shaped the year. JPM is not designed to win the daily tape, but it is designed to compound through it. That is exactly what 2026 has shown.

Please wait processing your request...

Please wait processing your request...